Bottled Water Market Summary

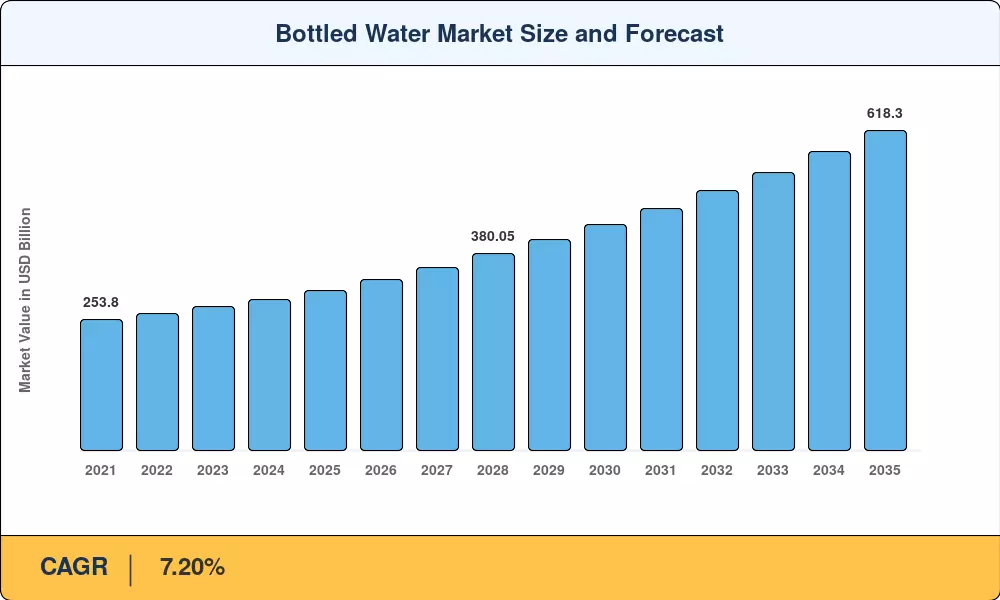

The global Bottled Water Market stood at USD 308.50 billion in 2025, poised to reach USD 330.71 billion in 2026 and an estimated USD 618.30 billion by 2035, registering a CAGR of 7.20% during 2026–2035. Tightening municipal water quality standards across both developed and emerging economies is accelerating packaged water adoption. In contrast, the World Health Organization's updated drinking water guidelines [1] have sharpened consumer scrutiny of tap water safety. These twin forces — regulatory push and consumer pull — are reshaping a category once viewed as a simple commodity into a value-driven wellness segment.

The bottled water market is changing dramatically in terms of production and packaging. Traditional single-use. The EU Single-Use Plastics Directive and similar state-level regulations in the U.S. are driving the transition from PET lines to closed-loop recycled-PET and aluminum systems [2]. In 2024, global investment in advanced purification technologies, including UV-C disinfection, nano-filtration, and electrolytic mineral enrichment, exceeded USD 4.2 billion [3], allowing manufacturers to support premium price designs and enhance quality benchmarks.

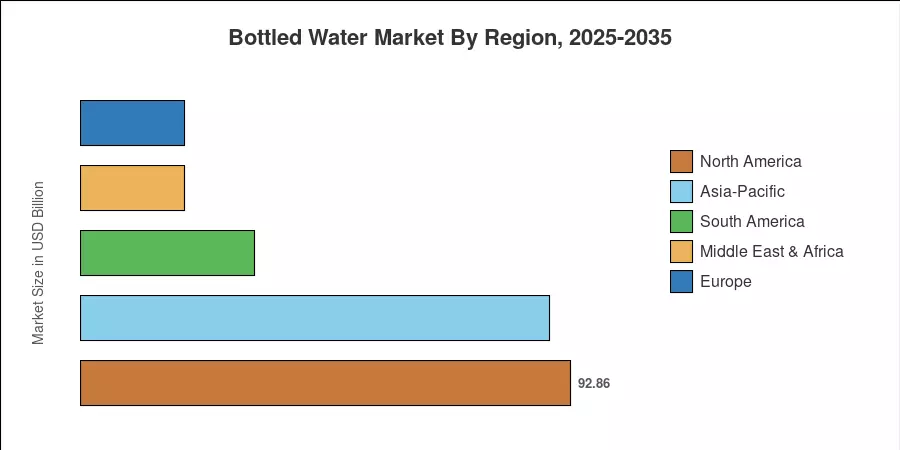

With a 30.1% regional share in 2025, North America dominated the bottled water market due to per-capita consumption of more than 50 gallons per year [4]. With a share of about 28.8%, Asia-Pacific follows closely, helped forward by the fast urbanization of China and India. With a CAGR of 10.7% through 2035, South America had the greatest regional growth rate due to unmet middle-class demand and improved cold-chain logistics in Argentina and Brazil. Producers who strike a balance between scale and sustainability credentials will be rewarded in the upcoming ten years.

Key Report Takeaways

• By Product Type

- Still water commanded approximately 77.6% of the bottled water market share in 2025, reinforced by its position as the default hydration choice across retail and foodservice channels.

- Functional and flavored water segments are expanding at an 8.8% CAGR through 2035, led by electrolyte-enhanced and vitamin-infused formulations.

• By Packaging Material

- PET bottles retained 65.3% of the Bottled Water Market in 2025, though recycled-PET mandates are raising input costs.

- Glass bottles are advancing at a 9.4% CAGR, supported by on-trade premiumization and sustainability-conscious consumers.

• By Geography

- North America led the Bottled Water Market with 30.1% share in 2025, with the U.S. per-capita spending at the forefront.

- South America posts the highest regional CAGR at 10.7%, underpinned by Brazilian urbanization and expanding organized retail.

Bottled Water Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing model integrates trade data from national customs agencies, production volumes from industry bodies such as the International Bottled Water Association (IBWA), and point-of-sale tracking from leading retail analytics firms. Historical values (2021–2024) reflect actuals; the 2025 base year blends confirmed H1 sales with modeled H2 estimates; and the forecast period (2026–2035) applies a calibrated compound annual growth trajectory.