Canned Tuna Market Summary

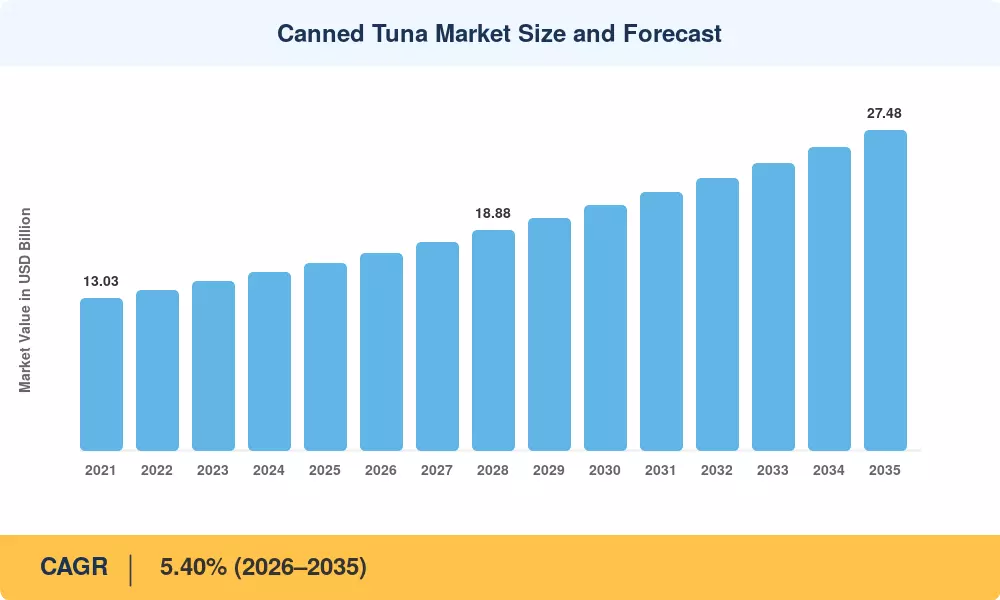

The global Canned Tuna Market was valued at USD 16.07 billion in 2025 and is projected to grow from USD 17.06 billion in 2026 to USD 27.48 billion by 2035, registering a CAGR of 5.40% during 2026–2035. Rising consumer preference for shelf-stable, high-protein convenience foods and expanding food-service procurement volumes are the twin engines behind this trajectory. Government-backed nutritional programs in Southeast Asia and Sub-Saharan Africa — several allocating over USD 200 million annually to fortified food distribution — are adding incremental demand for ready-to-eat canned fish products [2].

Processing technology is undergoing a quiet but consequential shift. Legacy steel-can lines, some dating back three decades, are giving way to flexible retort pouch systems that cut material costs by roughly 18% and reduce carbon intensity per unit. Thai Union Group alone committed USD 150 million between 2023 and 2025 to upgrade its Southeast Asian plants with automated pouch-filling and nitrogen-flush sealing lines, a move that other vertically integrated players are replicating across the Indian Ocean rim [3]. The transition also enables lighter shipping weights, which matters as ocean freight rates remain elevated.

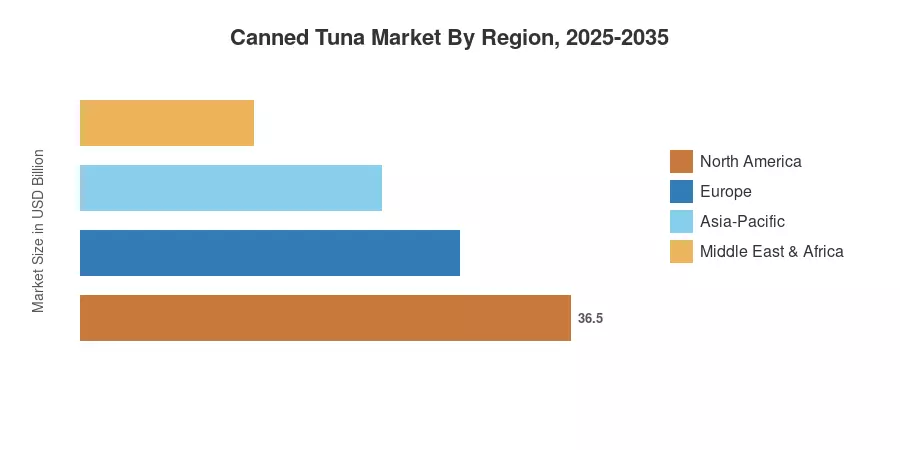

Europe commands the largest share of the Canned Tuna Market at an estimated 37.80% of 2025 revenues, driven by deeply entrenched consumption habits in Spain, Italy, and France. The Middle East & Africa region is the fastest-growing Region, with a projected CAGR of 6.10% through 2035, buoyed by new canning plants in Oman and rising per-capita protein intake across the Gulf Cooperation Council states Asia-Pacific holds the second-largest share at approximately 24.50%, anchored by Japan's premium sashimi-grade canned tuna segment and growing skipjack and albacore tuna consumption in the Philippines and Indonesia.

Key Report Takeaways

• By Product Type

- Light tuna accounted for 63.10% of the Canned Tuna Market in 2025, supported by skipjack's favorable mercury profile under FDA "Best Choice" guidance

- White tuna is forecast to expand at a 6.00% CAGR through 2035, as premiumization and MSC-certified sourcing lift retail price points

• By Packaging Type

- Metal cans generated USD 14.20 billion in Canned Tuna Market revenue during 2025, reflecting entrenched consumer trust in traditional packaging

- Pouches are projected to post a 6.20% CAGR from 2026 to 2035 as retailers prioritize lightweight, recyclable formats

• By Distribution Channel

- Off-trade channels captured roughly 64.30% of global sales in 2025, with supermarket private-label lines expanding aggressively

- On-trade distribution is anticipated to grow at a 6.70% CAGR through 2035, fueled by post-pandemic food-service volume recovery

• By Region

- Europe dominated with a 37.80% share of the Canned Tuna Market in 2025, led by per-capita consumption exceeding 3 kg annually in Spain

- The Middle East & Africa region leads growth projections at a 6.10% CAGR through 2035

Canned Tuna Market Size and Forecast (2021–2035)

The figures below are derived from MRFR's proprietary demand-supply triangulation model, cross-referenced with FAO catch data, trade flow databases, and processor financial disclosures. Historical values (2021–2024) reflect actual industry revenues; the base year (2025) blends preliminary shipment data with channel-level sell-through estimates. Forecast values (2026–2035) apply MRFR's calibrated CAGR of 5.40%.