Carbon Capture and Storage Market Summary

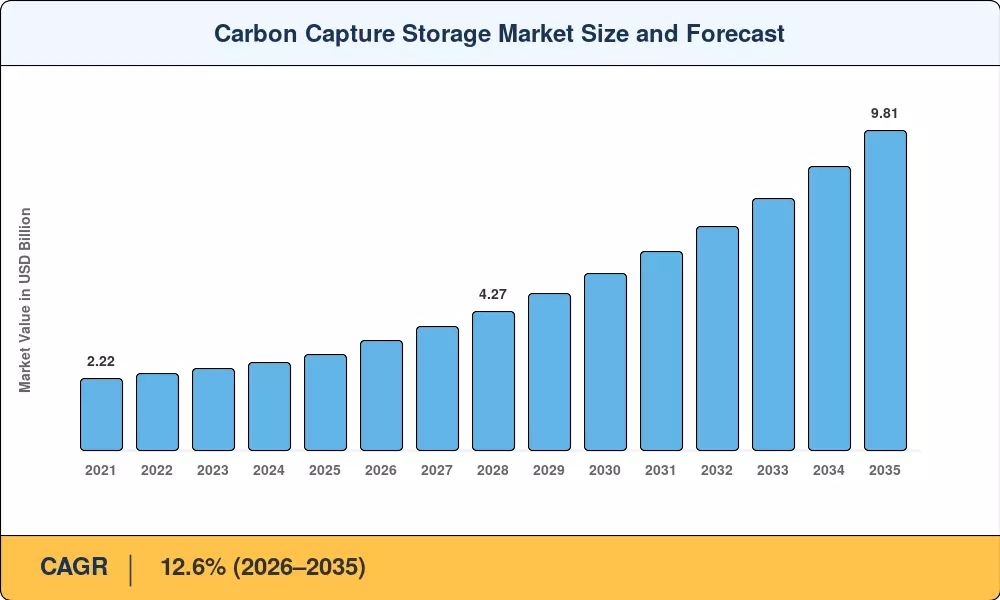

The Carbon Capture and Storage Market stood at USD 2.95 Billion in 2025 and is projected to reach USD 3.37 Billion in 2026 before climbing to USD 9.81 Billion by 2035, registering a CAGR of 12.6% during 2026–2035. This expansion traces directly to the U.S. Inflation Reduction Act's enhanced 45Q tax credit — now worth up to USD 85 per tonne for dedicated geological storage — and the European Union's Carbon Border Adjustment Mechanism, which prices embedded emissions in imported steel, cement, and aluminium [1][2]. Together, these instruments have shifted the Carbon Capture and Storage Market from niche demonstration projects to bankable commercial infrastructure.

The technology landscape is moving fast. First-generation amine scrubbers that dominated early post-combustion CO2 capture installations are giving way to advanced solvent blends, membrane contactors, and solid-sorbent systems that promise 30–40% lower energy penalties [3]. The U.S. Department of Energy committed USD 3.5 billion through its Carbon Capture Demonstration Projects Program to accelerate next-generation capture at coal, gas, and industrial facilities, while the EU Innovation Fund allocated EUR 1.8 billion across fifteen large-scale CCS projects in 2024 alone [4][5].

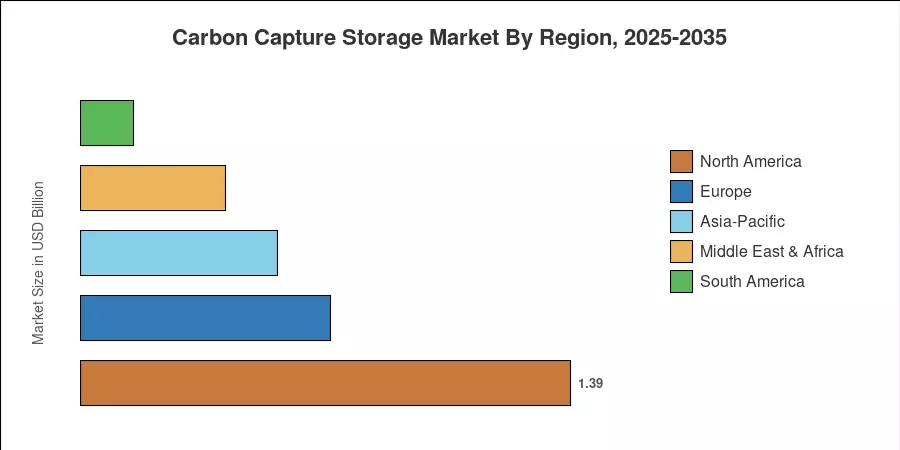

North America commands roughly 47% of the Carbon Capture and Storage Market, anchored by the Gulf Coast's mature pipeline network and sequestration geology. Europe, propelled by aggressive decarbonization targets and cross-border CO2 transport agreements, is the fastest-growing region at a projected CAGR of approximately 24%. Asia-Pacific holds the second-largest share at around 19%, driven by China's coal-dependent power fleet and Japan's strategic investments in offshore storage. The decade ahead will test whether policy momentum translates into sustained deployment at the gigaton scale.

Key Report Takeaways

• By Technology

- Pre-combustion capture accounted for approximately 76% of the Carbon Capture and Storage Market in 2025, reflecting its established role in hydrogen production and syngas processing.

- Oxy-fuel combustion capture is positioned as the fastest-growing technology segment at a projected CAGR of roughly 19.6% through 2035.

• By End-User Industry

- The oil and gas segment represented about 64% of the Carbon Capture and Storage Market size in 2025.

- The chemical sector is expected to expand at a CAGR of approximately 27% between 2026 and 2035, driven by ammonia and ethylene decarbonization mandates.

• By Region

- North America led the Carbon Capture and Storage Market with close to 47% revenue share in 2025.

- Europe is projected to deliver the fastest regional growth, supported by the EU ETS Phase IV framework and North Sea storage developments.

- Asia-Pacific contributed roughly USD 0.56 billion in 2025, anchored by industrial capture projects in China and Japan.

Carbon Capture and Storage Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from operational facility databases maintained by the Global CCS Institute, supplemented by disclosed capital expenditure filings and emissions-intensity benchmarks from the IEA Greenhouse Gas R&D Programme. Forecast projections apply a bottom-up capacity model cross-validated against policy pipeline analysis and announced project FID schedules [6][7].