Cattle Feed Market Summary

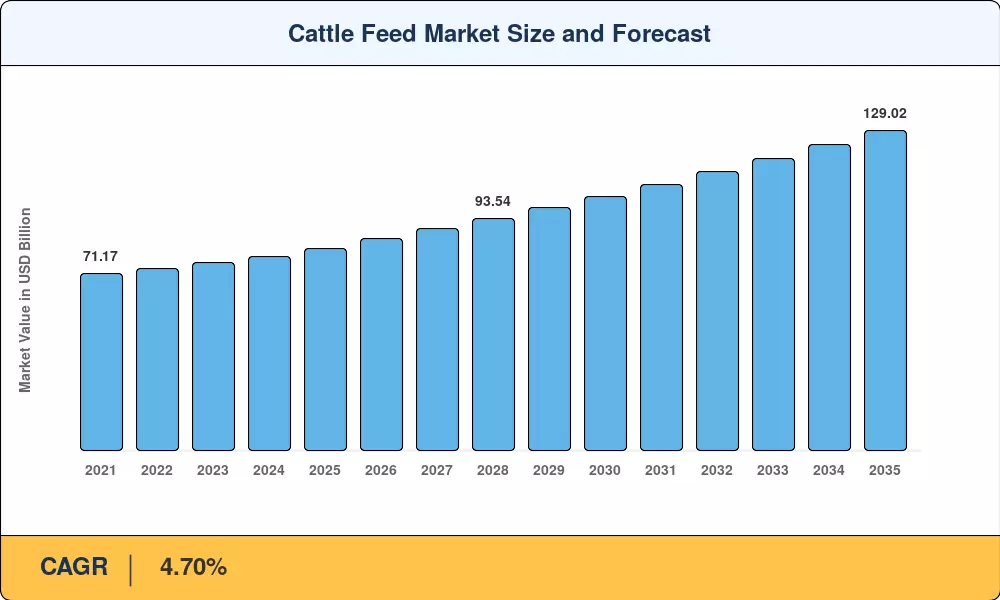

The global Cattle Feed Market reached an estimated USD 81.50 billion in 2025 and is projected to climb from USD 85.33 billion in 2026 to USD 129.02 billion by 2035, registering a compound annual growth rate of 4.70% across the forecast window. Sovereign protein-security mandates in over forty countries now channel surplus grain harvests toward domestic milling operations, while rapid feedlot expansion across South America has shifted economics decisively in favor of high-energy manufactured rations over pasture conversion [1]. These structural forces anchor a demand base that has proven resilient even during volatile crop cycles.

Feed production technology is undergoing a generational shift. Legacy dry-batch mixing lines are giving way to liquid feeding platforms capable of real-time nutrient dosing, a transition accelerated by the European Union's 2022 ban on prophylactic antimicrobials that redirected over USD 1.2 billion in annual additive spending toward phytogenic and probiotic alternatives [2]. Automated dairies in Northern Europe now report 8–12% reductions in dust-related ingredient loss after adopting liquid delivery, and similar installations are scaling across India's cooperative dairy belt [3].

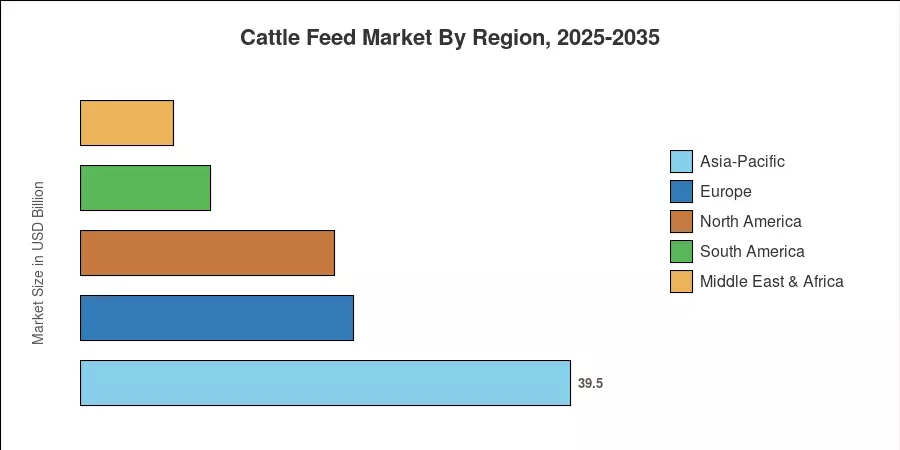

Asia-Pacific commands the largest share of the Cattle Feed Market at roughly 39.5% of 2025 revenue, anchored by China's industrial herd programs and India's expanding dairy cooperatives. Africa is positioned as the fastest-growing region with an anticipated CAGR of 5.9%, driven by credit-backed cooperative models that bundle fortified rations with veterinary services [4]. Europe holds the second-largest position at approximately 22.0%, sustained by stringent feed-safety regulation and high per-animal spending. The Cattle Feed Market outlook through 2035 hinges on how quickly emerging-market herds transition from subsistence grazing to formulated feeding regimes.

Key Report Takeaways

• By Animal Type

- Dairy cattle accounted for 57.0% of the Cattle Feed Market in 2025, reflecting the dominance of fluid-milk demand across Asia and Europe.

- Beef cattle segments are forecast to grow at a 5.7% CAGR through 2035, propelled by feedlot intensification in Brazil and Argentina.

• By Ingredient

- Cereals represented 45.4% of the Cattle Feed Market by ingredient value in 2025.

- Feed additives are projected to register a 5.8% CAGR from 2026 to 2035, the fastest-expanding ingredient category as phytogenic compounds displace older antimicrobials.

• By Form

- Pellets commanded a 56.5% share of the Cattle Feed Market in 2025, favored for storage efficiency and controlled nutrient delivery.

- Liquid feed is expected to grow at a 5.1% CAGR through 2035, gaining traction inside automated dairy operations.

• By Region

- Asia-Pacific held a 39.5% share of the Cattle Feed Market in 2025.

- Africa is projected to post a 5.9% CAGR from 2026 to 2035.

Cattle Feed Market Size and Forecast (2021–2035)

Market size estimates draw on primary interviews with feed millers, cooperative procurement officers, and grain-trading desks across 35 countries, cross-referenced with customs data and national livestock census records [5]. Historical values reflect actual trade, while forecast projections apply a supply-demand equilibrium model calibrated to herd growth trajectories, ingredient price indices, and regulatory timelines.