Chlor Alkali Market Summary

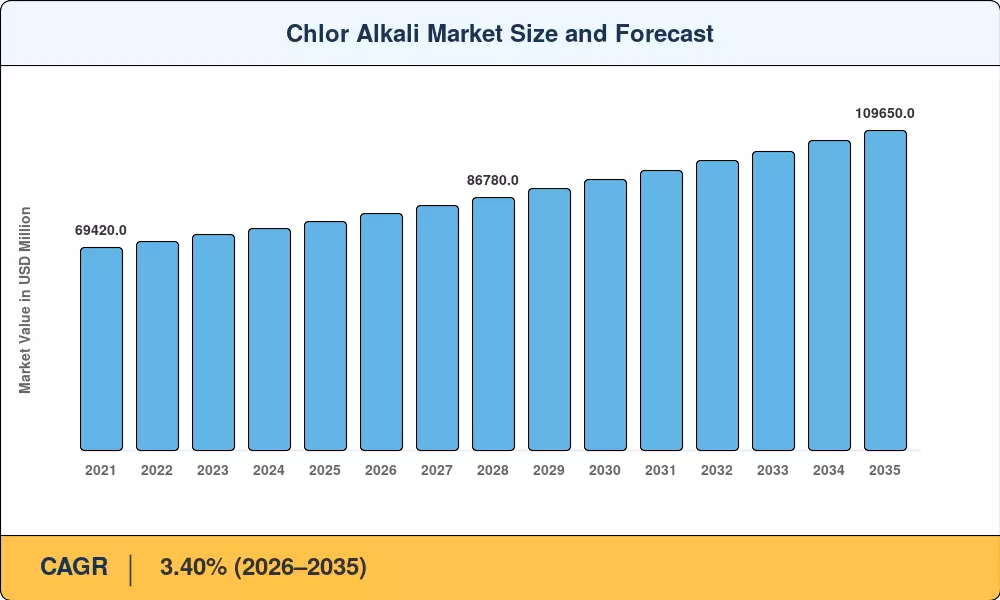

The Chlor-Alkali Market reached USD 78,500 million in 2025 and is projected to grow from USD 81,170 million in 2026 to USD 109,650 million by 2035, registering a CAGR of 3.40% during the forecast period. This expansion is anchored to rising demand from water treatment infrastructure programs worldwide and tightening environmental mandates that are forcing plant operators to modernize aging capacity. The European Union's Industrial Emissions Directive, which mandated the retirement of all mercury-based chlor-alkali cells by December 2023 [1], has triggered a capital cycle that continues to reshape global supply balances through 2035.

The trend of the chlor-alkali market is centered on technological transformation. Membrane cell technology is gradually replacing legacy diaphragm and mercury cell installations, which used to account for more than half of Western capacity. Currently, membrane cells use less than 2,100 kWh per ton of caustic soda produced, which is around 30% less than diaphragm substitutes [2]. Industrial decarbonization schemes that directly support membrane conversions and hydrogen by-product capture have received incentives totaling more than USD 1.8 billion from the governments of North America and Europe [3].

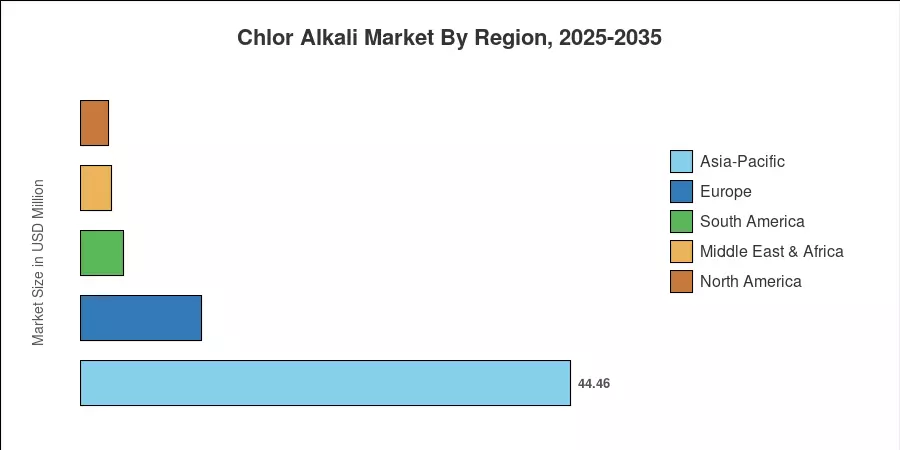

Asia-Pacific is by far the leading region, holding around 57.0% of the Chlor-Alkali Market. With capacity additions in China and India linked to downstream PVC, alumina, and textile demand, the area is also the fastest-growing, with a 3.50% CAGR through 2035. Thanks to integrated chemical complexes along the US Gulf Coast and shale-gas cost advantages, North America commands around 18.5% of the worldwide market. Europe makes up about 15% of the total, where carbon pricing mechanisms and zero-liquid-discharge laws are accelerating capacity migration toward more efficient units.

Key Report Takeaways

• By Product

- Chlorine held a 37.5% share of the Chlor-Alkali Market in 2025, driven by downstream vinyl chloride monomer and water disinfection demand.

- Caustic soda is expanding at the fastest pace among product segments, underpinned by alumina refining and pulp bleaching applications globally.

• By Production Process

- Membrane cell technology accounted for a 57.5% share of the Chlor-Alkali Market in 2025, reflecting ongoing conversions from legacy cell types.

- Diaphragm cell installations continue to contract as operators face rising energy costs and stricter emission standards.

• By Application

- Pulp and paper represented a 33.5% share of the Chlor-Alkali Market in 2025, anchored by bleaching chemical requirements in integrated paper mills.

- Organic chemicals and alumina refining are emerging as high-growth application verticals through 2035.

• By Region

- Asia-Pacific captured 57.0% of the Chlor-Alkali Market in 2025 and leads all regions in absolute capacity additions.

- North America is advancing at a 3.30% CAGR, supported by integrated petrochemical complexes and favorable energy pricing.

Chlor-Alkali Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated research methodology combining bottom-up capacity utilization analysis, trade flow modeling, and top-down demand estimation from downstream consumption sectors. Historical figures (2021–2024) reflect verified production and trade data, while the forecast period (2026–2035) is constructed using proprietary regression models calibrated to energy pricing, regulatory timelines, and downstream GDP elasticity.