Chocolate Market Summary

The global Chocolate Market reached an estimated USD 121.32 billion in 2025, with the forecast period beginning at USD 127.18 billion in 2026 and climbing to USD 197.85 billion by 2035 at a CAGR of 5.38%. This expansion reflects a structural shift in consumer spending habits — households across both mature and developing economies are trading up from commodity confections to premium, origin-certified, and wellness-positioned products. The EU's Farm to Fork Strategy and tightening cocoa traceability regulations under the EU Deforestation Regulation (EUDR), effective since December 2024, are compelling supply-chain overhauls that simultaneously raise the value ceiling for compliant producers [2].

Product innovation is rewriting the competitive playbook in the Chocolate Market. Bean-to-bar artisan chocolate facilities, small-batch fermentation programs and functional chocolate health claim formulations enriched with probiotics, adaptogens and plant proteins are augmenting – and in some segments displacing – legacy mass production lines built around standardized milk chocolate tablets. Industry capex trackers point towards global expenditures on processing lines for the dark chocolate premium segment crossing USD 2.1 billion in 2024 as manufacturers raced to meet demand for higher-cacao-content SKUs [3].

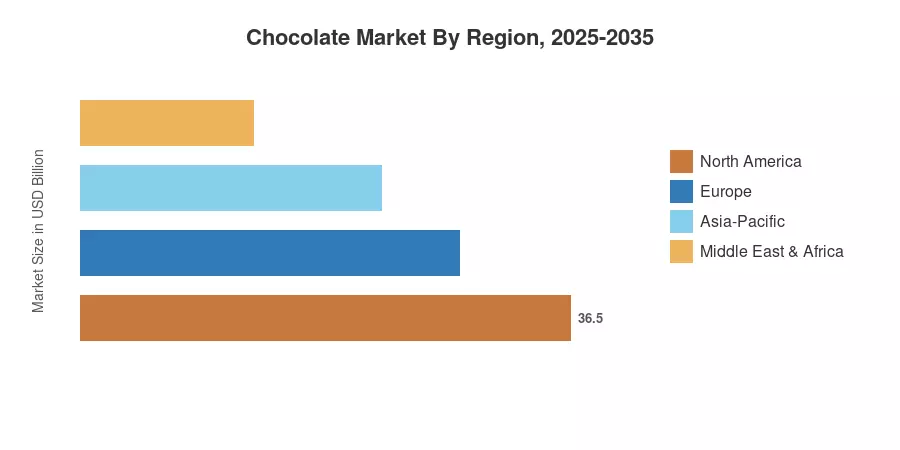

Europe dominates the Chocolate Market with a 46.5% share of 2025 revenues, backed by per capita consumption rates in Switzerland, Germany, and Belgium that are the highest in the world. The Middle East & Africa are expected to be the fastest expanding territory, registering a CAGR of 6.42% through 2035, primarily due to urbanization and increased disposable incomes in the Gulf nations and Nigeria. The Asia-Pacific region has the second largest income stream, with a giving culture in Japan and rapid sugar-free chocolate innovation launches in India and China In the next decade, companies that can combine sustainable chocolate sourcing agreements with scalable, margin-accretive product ranges will be rewarded.

Key Report Takeaways

• By Product Type

- Milk and white chocolate variants captured approximately 68.9% of the chocolate market revenue in 2025, reflecting entrenched consumer preference for sweeter profiles

- Dark chocolate is forecast to expand at a 5.75% CAGR through 2035, propelled by clinical research linking high-cacao intake to cardiovascular benefits and the broader dark chocolate premium segment trend

• By Form

- Tablets and bars led with a 51.4% revenue share in the Chocolate Market in 2025

- Pralines and truffles are advancing at a 5.35% CAGR to 2035, driven by gifting occasions and bean-to-bar artisan chocolate positioning

• By Price Range

- The mass tier accounted for USD 90.46 billion in 2025, underpinning volume dominance across emerging geographies

- The premium segment is projected to grow at a 6.82% CAGR through 2035, the fastest across all price tiers

• By Ingredient Type

- Dairy-based products represented an 86.4% share in 2025, though plant-based formulations are advancing at a 6.58% CAGR through 2035

• By Distribution Channel

- Supermarkets and hypermarkets captured roughly 46.7% share of the Chocolate Market in 2025

- Online retail is progressing at a 7.59% CAGR through 2035, the strongest channel-level growth rate

• By Regional

- Europe commanded a 46.5% share of the Chocolate Market in 2025, while the Middle East & Africa posted the fastest regional CAGR at 6.42%

Chocolate Market Size and Forecast (2021–2035)

Market Research Future’s market-sizing approach combines a top-down examination of revenue for publicly listed confectionery firms with bottom-up estimates of volumes from trade agencies such as ICCO, Euromonitor and national cocoa boards. Historical data (2021-2024) confirmed using customs data and manufacturer disclosures. Forecast data (2026-2035) uses a calibrated CAGR based on demand elasticity models and sustainable cocoa sourcing supply restrictions.

.webp?v=1783340210)