Circuit Breaker Market Summary

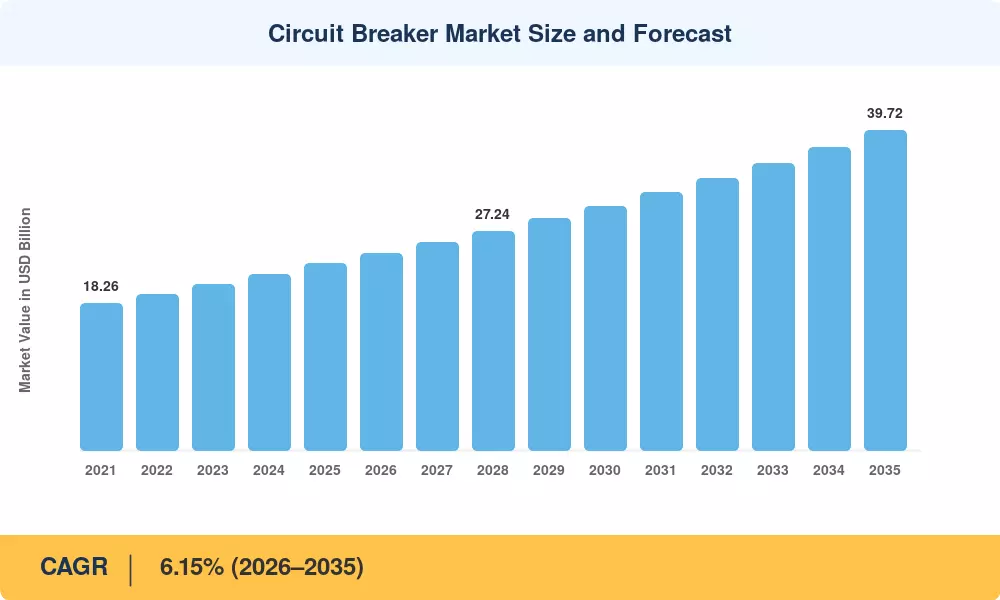

The global Circuit Breaker Market reached an estimated USD 23.18 billion in 2025 and is projected to grow from USD 24.61 billion in 2026 to USD 39.72 billion by 2035, registering a CAGR of 6.15% over the forecast period. Grid-modernization programs—particularly the USD 65 billion earmarked under the U.S. Bipartisan Infrastructure Law for power-grid upgrades—are driving a replacement cycle for aging switchgear across transmission and distribution networks [2]. Parallel investment in renewable-energy interconnection and industrial electrification is broadening the addressable base for advanced interruption devices.

Technology transformation is in the air as traditional oil-filled and SF₆ gas circuit breakers are replaced by vacuum circuit breaker MV distribution units and SF6-free circuit breaker green alternatives. As a response, the European Commission proposes a phase-down legislation for F-gases, aiming to reduce the use of SF 6 by 80% by 2030, driving manufacturers towards solid-dielectric and eco-gas interruption media [3]. Solid-state breakers, which were previously relegated to specialized HVDC high voltage DC circuit breaker applications, are now finding their way into data-center campuses and EV charging areas where sub-millisecond fault clearing is required.

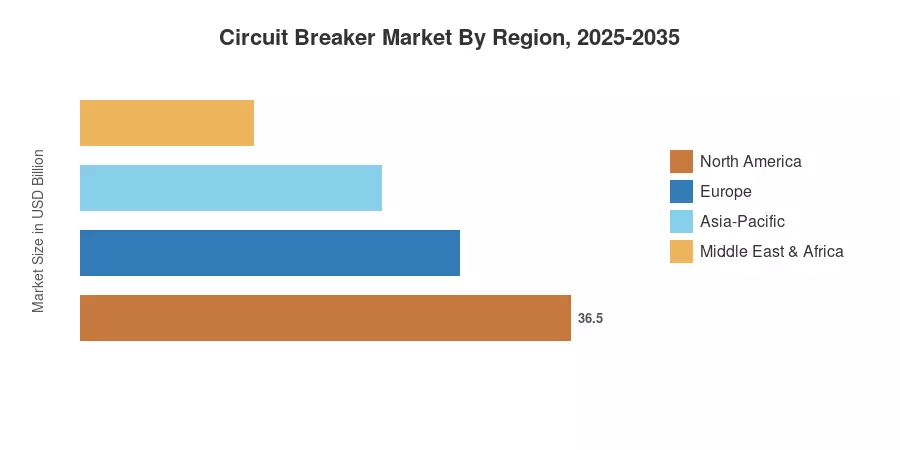

The Asia-Pacific region holds around 42.3% of the global Circuit Breaker Market revenue, led by the growth of China’s State Grid Corporation and India’s Revamped Distribution Sector Scheme (RDSS). Europe maintains the second-biggest proportion, some 23.5%, led by offshore-wind grid connections and smart-grid retrofits. The market for MCB miniature circuit breaker panels in Asia-Pacific is expected to rise at the quickest CAGR of 7.2% through 2035, owing to an expansion in household electrification projects

Key Report Takeaways

• By Type

- Vacuum circuit breaker MV distribution technology captured 36.6% of the Circuit Breaker Market in 2024, reflecting strong adoption in medium-voltage switchgear replacements

- Solid-state interruption devices are forecast to expand at a 9.4% CAGR through 2035, propelled by data-center and HVDC high voltage DC circuit breaker deployments

• By Voltage

- Medium-voltage equipment held 39.1% of the Circuit Breaker Market in 2024, underpinned by distributed solar and wind integration

• By Mounting

- Live-tank mounting variants led with a 38.2% share, while dead-tank configurations are advancing at a 8.6% CAGR to 2035

• By End User

- Utilities accounted for 41.0% of Circuit Breaker Market revenue in 2024 and remain the dominant procurement channel

• By Region

- Asia-Pacific's 7.2% CAGR makes it the fastest-growing region, with China and India contributing over 60% of regional demand

Market Size and Forecast (2021–2035)

The figures below are derived from MRFR’s unique bottoms-up methodology, which compiles switchgear procurement data from utilities’ tenders, industrial CAPEX filings and OEM shipment disclosures in 42 countries. Historical values (2021-2024) are harmonized with customs-trade databases. Forecast figures use a calibrated CAGR of 6.15%.

.webp?v=1785402810)