Coffee Market Summary

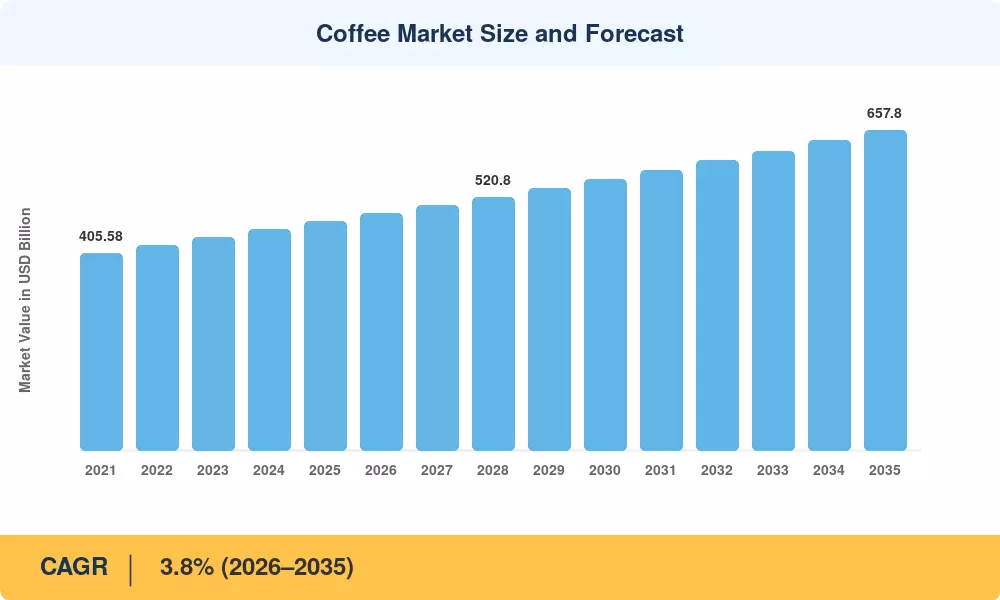

The global Coffee Market reached an estimated USD 471.2 billion in 2025 and is projected to grow from USD 489.1 billion in 2026 to USD 657.8 billion by 2035, registering a CAGR of 3.8% during the forecast period (2026–2035). This expansion is anchored in rising per-capita consumption across emerging economies and a structural shift toward specialty single-origin coffee that commands higher price points. The European Union's Deforestation Regulation (EUDR), which mandates full supply-chain traceability for coffee imports by late 2025, is reshaping sourcing economics and accelerating investment in sustainable certified coffee programs across Latin America and Southeast Asia [2].

A quiet transformation is underway in how coffee reaches consumers. Legacy commodity-grade supply chains — built around bulk Robusta trading and instant-powder processing — are giving way to vertically integrated models that emphasize espresso coffee bean roast profiling, direct-trade sourcing, and cold brew ready-to-drink coffee innovation. Global venture and corporate investment in coffee-tech startups exceeded USD 2.8 billion between 2022 and 2024, spanning precision fermentation, AI-driven roast optimization, and blockchain traceability platforms [3]. The coffee subscription delivery trend has matured from a niche direct-to-consumer play into a mainstream retail channel, with major roasters reporting subscription revenues growing at two to three times the rate of traditional retail.

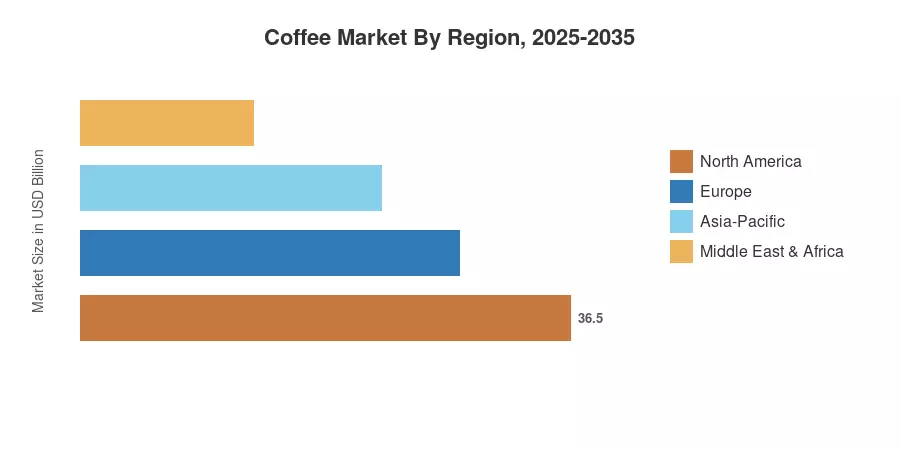

Europe commands the largest share of the Coffee Market at roughly 34% of global revenue, driven by the continent's deeply rooted café culture and stringent quality import standards. Asia-Pacific is the fastest-growing region at a projected 5.4% CAGR, fueled by urbanization in China, India, and Southeast Asia, where tea-drinking populations are rapidly adopting specialty coffee habits North America remains the second-largest region, accounting for approximately 28% of the Coffee Market, with cold brew and ready-to-drink formats driving incremental volume growth through convenience retail channels.

Key Report Takeaways

• By Product Type

- Roast & ground coffee holds the dominant share of the Coffee Market at approximately 42% of global revenue, supported by widespread retail penetration and home-brewing adoption

- Cold brew ready-to-drink coffee is the fastest-growing product category at an estimated 7.2% CAGR, reflecting consumer preference for convenience and premium positioning

- Instant coffee generates roughly USD 130 billion in annual revenue, with strong demand persistence in the Asia-Pacific and African markets

• By Distribution Channel

- Supermarkets and hypermarkets account for ~38% of the coffee market distribution volume

- Online and coffee subscription delivery trend channels are expanding at a 6.8% CAGR, outpacing brick-and-mortar growth by a factor of 2.5×

• By Geography

- Europe dominates the Coffee Market with a 34% revenue share, led by Germany, France, and Italy

- Asia-Pacific is projected to add approximately USD 68 billion in incremental value by 2035

- Brazil anchors the South American Coffee Market as both the world's largest producer and a rapidly growing domestic consumption hub

Coffee Market Size and Forecast (2021–2035)

MRFR's market sizing combines top-down revenue analysis from trade bodies (International Coffee Organization, USDA Foreign Agricultural Service) with bottom-up validation using company financials, import/export data, and proprietary primary surveys of 420+ stakeholders across the coffee value chain. All figures are expressed in current USD and adjusted for inflation where applicable.

.webp?v=1782888030)