Cold Brew Coffee Market Summary

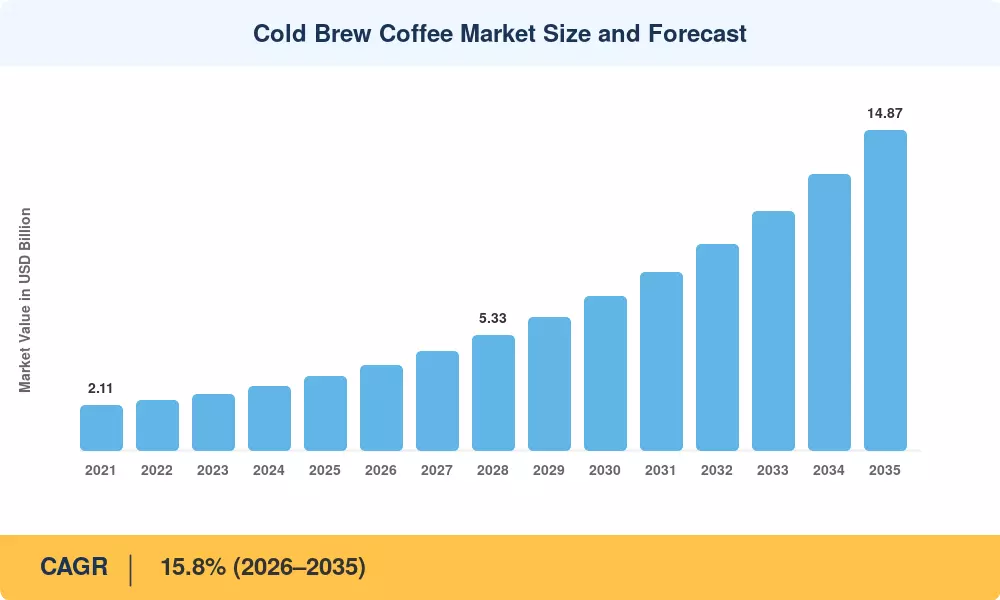

The Cold Brew Coffee Market was valued at USD 3.43 Billion in 2025 and is projected to grow from USD 3.97 Billion in 2026 to USD 14.87 Billion by 2035, registering a CAGR of 15.8% during the forecast period (2026–2035). Younger demographics across developed economies are accelerating the shift away from instant coffee toward premium, lower-acidity brewing methods. The National Coffee Association's 2024 consumer survey reported that cold brew consumption among 18–34-year-olds grew 22% year-over-year, a catalyst that continues to reshape retail shelf allocation and foodservice menus [1].

This transformation is fundamentally altering how coffee is produced, distributed, and consumed. Legacy hot-brew concentrate operations are giving way to nitrogen-infused extraction lines and aseptic flash-chill processing that extend shelf life to 90+ days. Nestlé alone committed over USD 250 million between 2023 and 2025 to retrofit plants for ambient-stable cold coffee formats, reflecting the capital flowing into this segment [2]. Simultaneously, single-serve pod manufacturers are integrating cold-brew capsule technology into existing machine ecosystems, lowering the barrier to home preparation.

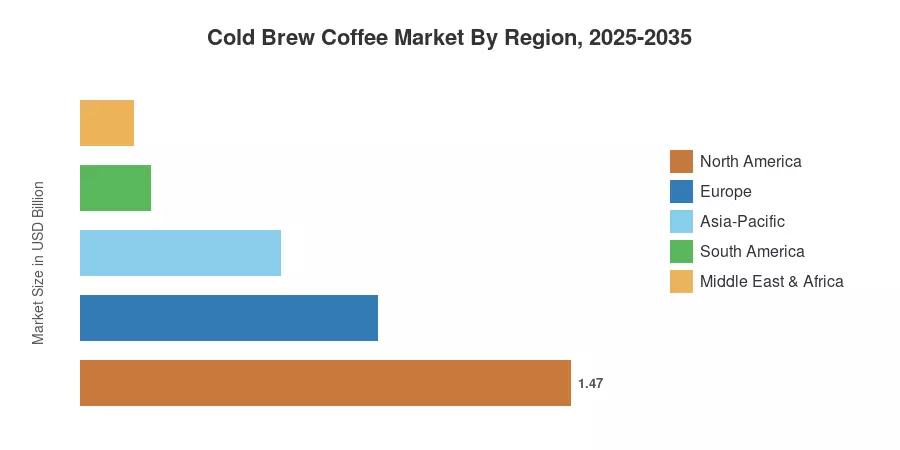

North America held approximately 43% of the Cold Brew Coffee Market in 2025, anchored by strong RTD retail penetration in the United States and Canada. Asia-Pacific stands as the fastest-growing region with an estimated CAGR of 17.5%, fueled by specialty café expansion in China, India, and Southeast Asia. Europe accounted for the second-largest share at roughly 26%, driven by private-label growth in Germany and the United Kingdom. As sustainability certifications and functional ingredient innovation intensify, the Cold Brew Coffee Market is positioned for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Form

- RTD cold brew products captured approximately 70% of the Cold Brew Coffee Market share in 2025, underscoring the dominance of grab-and-go consumption occasions.

- Cold brew pods are forecast to register a 16.8% CAGR through 2035, reflecting rapid adoption in home-brewing systems.

• By Flavor

- Unflavored variants accounted for roughly 52% of revenue in 2025, as purist consumers gravitated toward single-origin profiles.

• By Packaging Format

- Cans are projected to grow at a 17.2% CAGR, driven by portability and recyclability appeal among eco-conscious buyers.

• By Nature

- Conventional cold brew held about 67% of volume in 2025, though organic offerings are accelerating fastest at a 17.6% CAGR.

• By Distribution Channel

- Off-trade channels represented roughly 63% of the Cold Brew Coffee Market share, led by grocery and convenience store penetration.

• By RegionRegion

- North America dominated with a 43% share in 2025, supported by established RTD distribution networks.

- Asia-Pacific is expected to surge at a 17.5% CAGR, led by urbanization and rising disposable incomes across China and India.

Cold Brew Coffee Market Size and Forecast (2021–2035)

Market sizing combines bottom-up revenue analysis of manufacturer shipments, retail audit data from Nielsen and Euromonitor, trade association statistics, and validated primary interviews with supply-chain participants. Historical figures (2021–2024) reflect actual sales; 2025 represents the calibrated base year; and 2026–2035 values are forecast using a compound annual growth framework adjusted for macro-consumer spending projections [3].