Cyber Warfare Market Summary

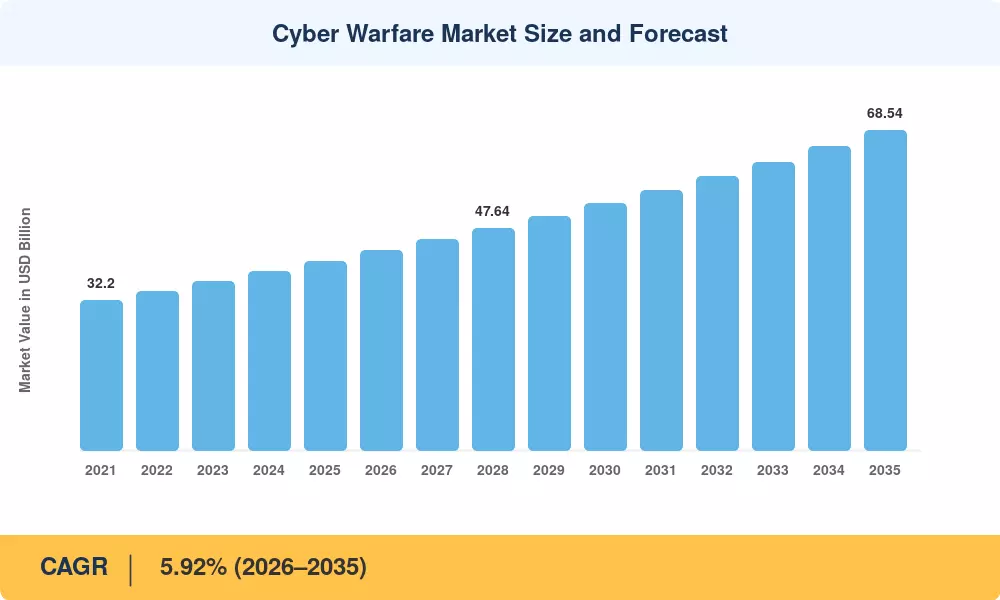

The Cyber Warfare Market reached an estimated USD 40.78 billion in 2025 and is projected to grow from USD 42.94 billion in 2026 to USD 68.54 billion by 2035, registering a CAGR of 5.92% during 2026–2035. This expansion is anchored in accelerating defense budgets earmarked for offensive cyber operations, military programs, and the formal recognition of cyberspace as a fifth warfighting domain by NATO and allied coalitions. The U.S. Department of Defense alone allocated over USD 13.5 billion to cyber-related activities in FY2025, reflecting a 15% year-over-year increase that signals sustained government commitment to the Cyber Warfare Market [2].

A fundamental technology transformation is reshaping spending patterns across the Cyber Warfare Market. Legacy perimeter-defense architectures—firewalls, signature-based intrusion detection, and air-gapped enclaves—are giving way to zero-trust frameworks, autonomous threat-hunting engines, and cognitive-warfare platforms powered by machine learning. Cyber threat intelligence defense capabilities now integrate real-time telemetry from satellite networks, cloud environments, and operational-technology sensors, creating a unified kill chain that compresses response times from hours to seconds [3]. Governments are mandating DevSecOps pipelines for continuous software updates, which shifts competitive advantage toward cloud-native vendors capable of rapid iteration.

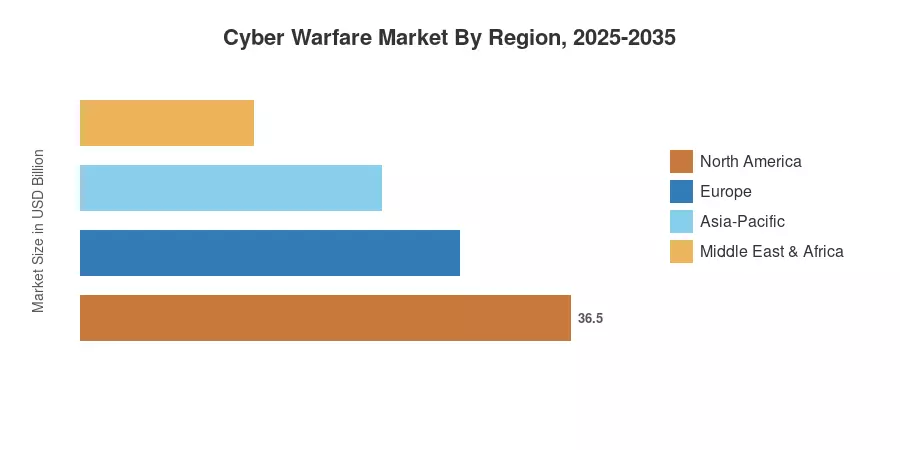

North America retained a dominant 42.18% share of the Cyber Warfare Market in 2025, driven by concentrated procurement from U.S. Cyber Command and the NSA. Asia-Pacific is the fastest-growing region at a projected CAGR of 7.58%, fueled by nation-state cyber attack concerns across the Indo-Pacific theater and rising budgets in Japan, South Korea, and India Europe holds the second-largest position, with critical infrastructure cyber protection mandates under the EU NIS2 Directive accelerating spending. The Cyber Warfare Market is poised to remain a strategic priority as digital conflict intensifies through 2035.

Key Report Takeaways

• By Component

- Solution offerings commanded approximately 71.89% of the Cyber Warfare Market share in 2025, reflecting demand for integrated cyber threat intelligence defense platforms

- The services segment is expanding at a 6.84% CAGR through 2035, propelled by managed detection-and-response contracts that address the cleared-personnel shortage

• By Deployment Mode

- On-premises installations held USD 15.62 billion in 2025, favored by defense agencies requiring air-gapped environments for offensive cyber operations, military use

- Cloud-based deployment is advancing at a 7.28% CAGR to 2035 within the Cyber Warfare Market, driven by elastic compute requirements for autonomous threat hunting

• By End-User Industry

- Defense and aerospace accounted for 34.22% of the Cyber Warfare Market share in 2025, anchoring procurement across all regions

- Healthcare is emerging at a 7.71% CAGR, as ransomware campaigns against hospital systems force investments in critical infrastructure cyber protection

• By Region

- North America retained a 42.18% share of the Cyber Warfare Market in 2025

- Asia-Pacific is projected to expand at a 7.58% CAGR to 2035, led by Japan and India

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue tracking from defense procurement databases, vendor financial disclosures, and government budget documents, cross-validated against top-down macroeconomic indicators and cyberspace domain military doctrine spending benchmarks.