Electronic Warfare Market Summary

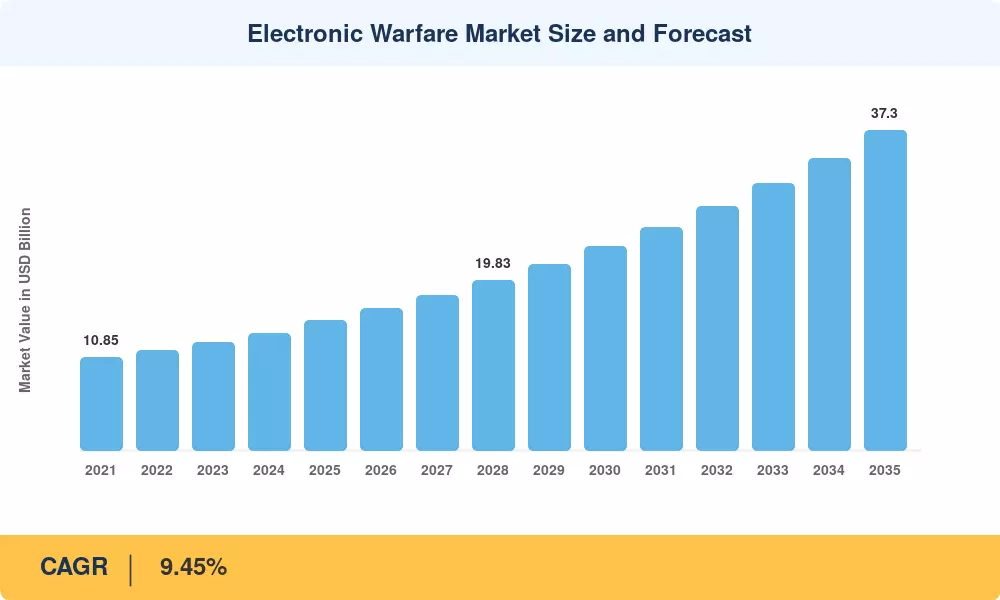

The Electronic Warfare Market reached USD 15.12 billion in 2025 and is projected to grow from USD 16.55 billion in 2026 to USD 37.30 billion by 2035, registering a 9.45% CAGR over the forecast period. Two catalysts anchor this trajectory: the U.S. Department of Defense allocated over USD 5.5 billion to electronic warfare programs in its FY 2025 budget request [1], and NATO's 2024 Vilnius Summit communiqué explicitly elevated electromagnetic spectrum operations to a tier-one warfighting priority [2]. These policy commitments create durable demand floors that insulate the Electronic Warfare Market from the cyclical defense-budget pressures facing more discretionary programs.

Procurement patterns are changing as a result of a technological turning point. Software-defined, cognitive architectures based on machine-learning signal classifiers and gallium-nitride (GaN) amplifier modules are replacing physically directed jammers and legacy analog receivers. A life-cycle cost estimate of USD 6.4 billion is associated with the U.S. Navy's Next Generation Jammer program alone [3], indicating the extent of platform-level change that is taking place. Operators with limited resources can obtain near-peer capabilities without completely replacing their platforms thanks to retrofit initiatives, which shorten integration timelines to 18–24 months.

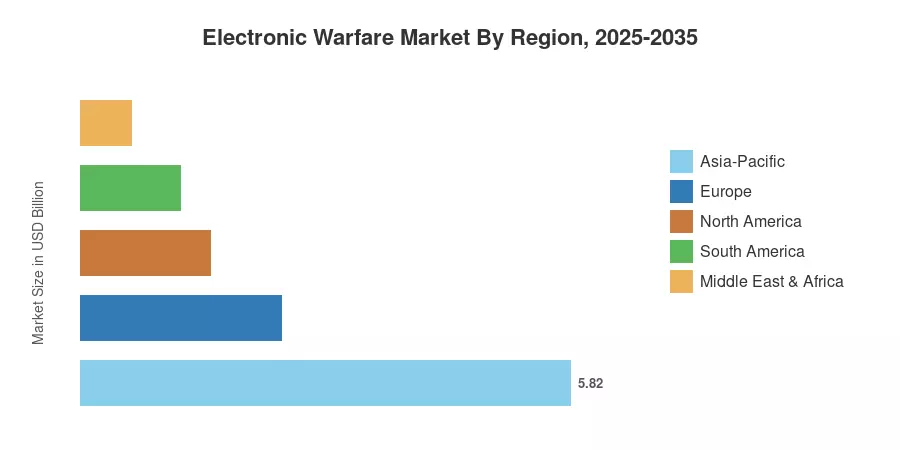

Due to India's domestic defense corridor initiatives and China's increasing investments in integrated electronic attack suites, Asia-Pacific accounts for around 38.5% of the electronic warfare market. Driven by Pentagon modernization objectives and classified special-access initiatives, North America comes in second with a 37.2% share and the fastest regional CAGR of 10.20%. Europe makes up 15.8% of the total, and spending is increasing around frameworks for pan-EU and Franco-German electronic defense cooperation. As drone proliferation and spectrum congestion increase the operational stakes for all services, the Electronic Warfare Market is expected to experience continuous double-digit regional growth pockets.

Key Report Takeaways

• By Capability

- Electronic Protection held a 37.8% share of the Electronic Warfare Market in 2025, reflecting sustained spending on self-protection suites across fighter and rotorcraft fleets.

- Electronic Attack is the fastest-expanding capability segment, advancing at a 9.92% CAGR through 2035 as offensive stand-in and stand-off missions gain operational priority.

• By Platform

- Air-based systems led the Electronic Warfare Market with approximately USD 5.30 billion in revenue during 2025, anchored by fighter-pod and escort-jammer procurement cycles.

- Space-based electronic warfare platforms are projected to record a 10.10% CAGR, the highest among all platform segments, as orbital sensing and denial capabilities attract dedicated budget lines.

• By Equipment

- Counter-UAS electronic warfare suites are growing at a 9.72% CAGR, outpacing legacy equipment categories amid the global drone-threat surge.

• By Region

- North America is on track to post a 10.20% CAGR in the Electronic Warfare Market through 2035.

- Asia-Pacific maintains the largest regional revenue pool, valued at roughly USD 5.82 billion in 2025.

Electronic Warfare Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down government budget allocations, bottom-up OEM contract values, and independent trade-source benchmarking to produce consensus-grade estimates. Historical data (2021–2024) draw on audited defense-industry revenue filings and congressional budget justification documents; forecast values (2026–2035) apply a composite CAGR validated against program-of-record timelines and procurement pipeline visibility.

.webp?v=1783951584)