Decorative Lighting Market Summary

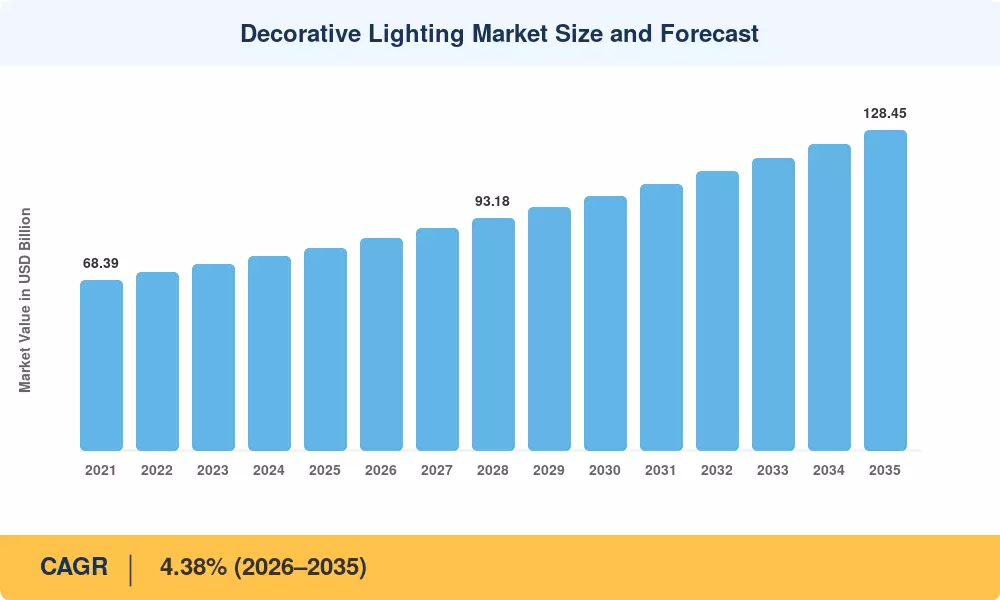

"The decorative lighting market reached an estimated USD 81.20 billion in 2025, with the forecast period beginning at USD 84.58 billion in 2026 and climbing to USD 128.45 billion by 2035 at a 4.38% CAGR." Growth in the decorative lighting market traces directly to tightening lamp efficacy standards—the U.S. Department of Energy's backstop rule now enforces a 45 lumen-per-watt minimum for general-service lamps, while the EU's Single Lighting Regulation (EU 2019/2020) phases out the last halogen categories by late 2025 [2]. These twin mandates are converting entire installed bases of incandescent and halogen pendant chandelier decorative lamp fixtures into LED decorative light fixtures that combine energy savings with design appeal.

The technology transition is in full swing. Legacy incandescent sources still represented a large replacement tail three years ago, but are being replaced by LED decorative light fixtures and developing OLED screens with tunable-white and circadian rhythm capabilities. According to the International Energy Agency, the global adoption of LED in residential settings has crossed 60% penetration in 2024, opening up USD 30 billion in annual energy cost savings globally [3]. Then there's smart home lighting systems. Built on Matter and Zigbee 3.0, these are now integrated into mid-range product lines, with linked controls an anticipated baseline rather than a premium upsell.

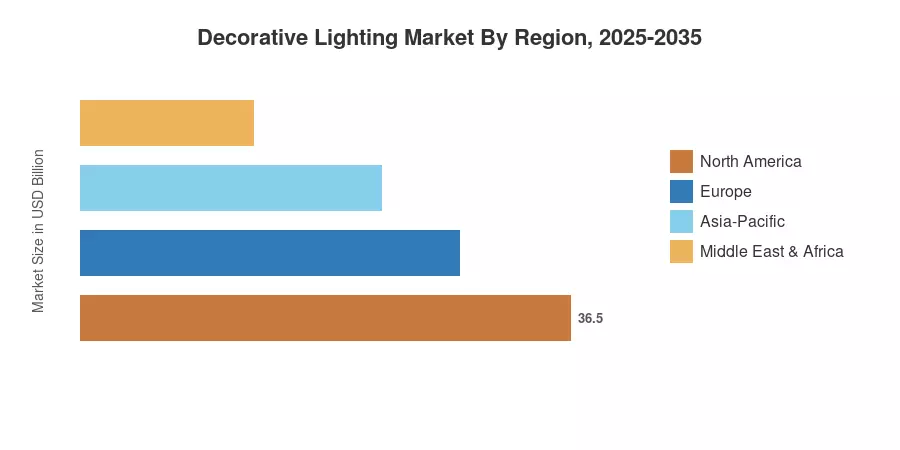

Asia-Pacific is the largest market for decorative lighting, accounting for around 38.4% of total sales worldwide, with China’s large luminaire export base and India’s fast urbanization among the key drivers. It is also the fastest-expanding region with a projected CAGR of 5.48% through 2035. The second largest market is Europe with a share of over 26%, driven by strong ecodesign rules and consumer desire for energy-efficient decorative lights. North America completes the top three, where remodeling expenditure and adoption of ambient lighting for smart house keeps demand robust across the predicted horizon.

Key Report Takeaways

• By Product Type

- Ceiling lights and chandeliers command the largest segment of the decorative lighting market, capturing over 37% of revenue in 2025, owing to strong replacement demand in both residential and hospitality settings

- Table and floor lamps are forecast to expand at a 4.78% CAGR through 2035 as portable, design-forward pendant chandelier decorative lamp products gain popularity in home offices and boutique retail

- Wall-mounted fixtures contribute a growing share as outdoor decorative string lights and architectural accent applications proliferate in commercial façade projects

• By Light Source

- LED technology held approximately 74.6% of the decorative lighting market in 2025, reinforcing its position as the default source for energy-efficient decorative bulbs

- OLED and solar-integrated solutions are set to register a 5.32% CAGR through 2035, appealing to designers seeking ultra-thin, flexible form factors

• By End-User

- Residential end-users generated roughly 63% of decorative lighting market revenue in 2025, underpinned by smart home ambient lighting adoption and home improvement spending cycles

- Commercial applications—including hospitality, retail, and office—are projected to grow at a 5.08% CAGR as brands invest in experiential lighting design

• By Geography

- Asia-Pacific leads the decorative lighting market with a projected 5.48% CAGR, powered by urbanization and manufacturing scale

- North America contributed approximately USD 19.50 billion in 2025, with renovation-led demand sustaining steady growth

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up revenue estimates from luminaire manufacturers with top-down cross-checks against trade data (UN Comtrade HS 9405), construction spend indices, and national energy agency installation records. Historical figures draw on audited company revenues and customs databases; forecast values apply the calibrated 4.38% CAGR with adjustments for policy-driven demand spikes and raw material cost inflation.