Digital Process Automation Market Summary

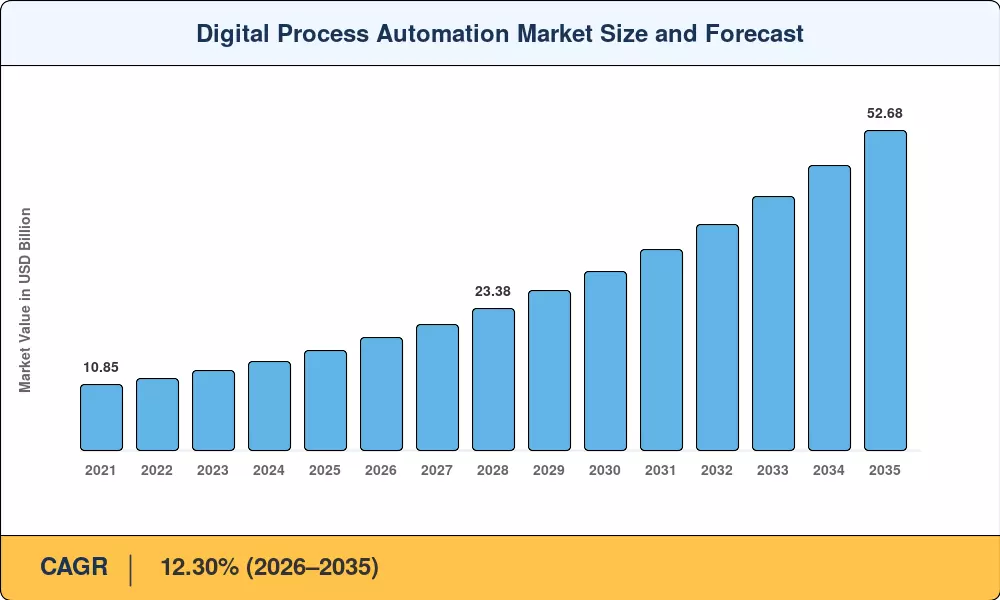

The Digital Process Automation Market reached a valuation of USD 16.52 Billion in 2025 and is projected to grow from USD 18.54 Billion in 2026 to USD 52.68 Billion by 2035, registering a CAGR of 12.30% during the forecast period (2026–2035). This trajectory reflects a structural shift across industries toward end-to-end workflow orchestration, driven in part by regulatory mandates such as the EU's Digital Operational Resilience Act (DORA) and the U.S. Federal Zero Trust Architecture strategy, both of which compel organizations to digitize, audit, and automate core business processes [1][2].

The technology landscape is moving beyond simple task-level scripting. Legacy business process management suites — often rigid, developer-dependent, and siloed — are giving way to unified low-code platforms that embed process mining, event-driven orchestration, and generative AI capabilities into a single design surface. Enterprise spending on intelligent automation platforms exceeded USD 8.2 Billion globally in 2024, according to estimates, and cloud hyperscalers are embedding native AI into their workflow tools, intensifying competitive pressure on traditional vendors [3][4].

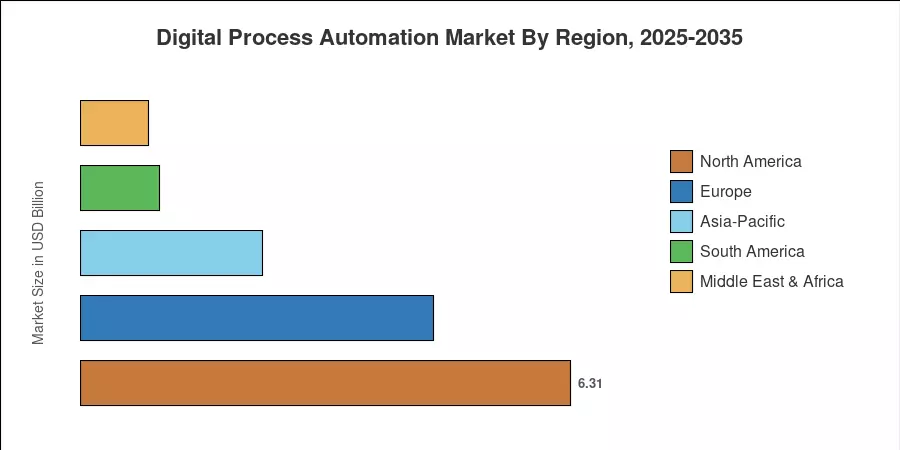

North America commands the largest share of the Digital Process Automation Market at 38.2% of 2025 revenue, supported by mature cloud infrastructure and early adoption of hyper-automation frameworks. Asia-Pacific is the fastest-growing region with a projected CAGR of 14.20%, fueled by aggressive digitization policies in India, China, and Southeast Asian economies. Europe holds the second-largest position at 27.5% share, with demand anchored in compliance-driven automation across financial services and manufacturing. As sustainability reporting mandates expand globally, the Digital Process Automation Market is positioned for sustained double-digit growth through the next decade.

Key Report Takeaways

• By Component

- The solution segment accounted for 58.5% of the Digital Process Automation Market in 2025, driven by enterprise demand for integrated low-code orchestration platforms.

- Services are projected to register a CAGR of 13.90% through 2035 as implementation consulting and managed automation services scale alongside platform adoption.

• By End User

- BFSI held a 29.5% share of the Digital Process Automation Market in 2025, reflecting regulatory pressure to automate compliance and customer onboarding workflows.

- Healthcare is anticipated to grow at a 14.40% CAGR, making it the fastest-expanding vertical through 2035.

• By Region

- North America led the Digital Process Automation Market with 38.2% of global revenue in 2025.

- Asia-Pacific is forecast to advance at a 14.20% CAGR through 2035, led by India's Digital India initiative and China's state-backed enterprise digitization programs.

Digital Process Automation Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines top-down industry supply analysis with bottom-up vendor revenue aggregation, cross-validated against enterprise IT spending surveys and regulator-mandated disclosure databases. Historical figures (2021–2024) are actuals; 2025 is the calibrated base year; 2026–2035 values are forecast using proprietary demand modeling.