Digital Twin Market Summary

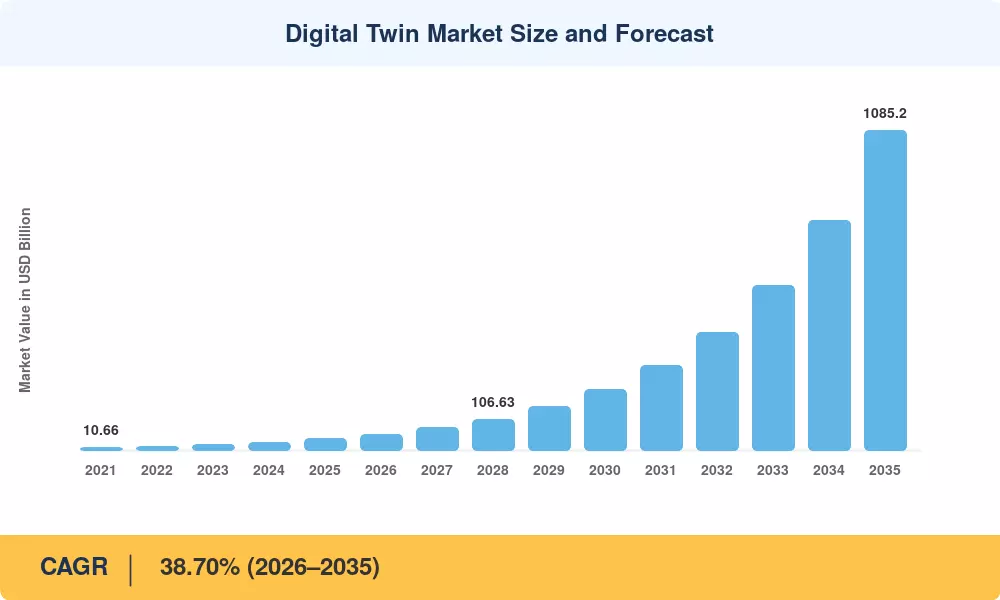

The Digital Twin Market was valued at USD 39.45 billion in 2025 and is projected to reach USD 53.60 billion in 2026 before climbing to USD 1,085.20 billion by 2035, registering a CAGR of 38.70% during the 2026–2035 forecast window. This acceleration is anchored in two converging forces: widespread industrial IoT platform maturation and a wave of government mandates requiring a real-time digital twin for energy grid management across safety-critical infrastructure in the US, EU, and China. The US Department of Energy's 2024 allocation of USD 1.2 billion toward grid modernization programs specifically earmarked digital-replica capabilities for transmission monitoring [2].

Physics-informed, cloud-native simulation environments combining sensor data, AI inference and 3D visualization replace legacy siloed SCADA and CAD-based design procedures. Global spending on enterprise IoT-based digital twin for smart manufacturing surpassed USD 8 billion in 2024, led by automotive OEMs and semiconductor fabs seeking 12–18% yield gains through virtual process optimization [3]. Industrial digital twin for predictive maintenance already underlies more than 40% of new condition monitoring contracts signed by Tier-1 equipment vendors [4].

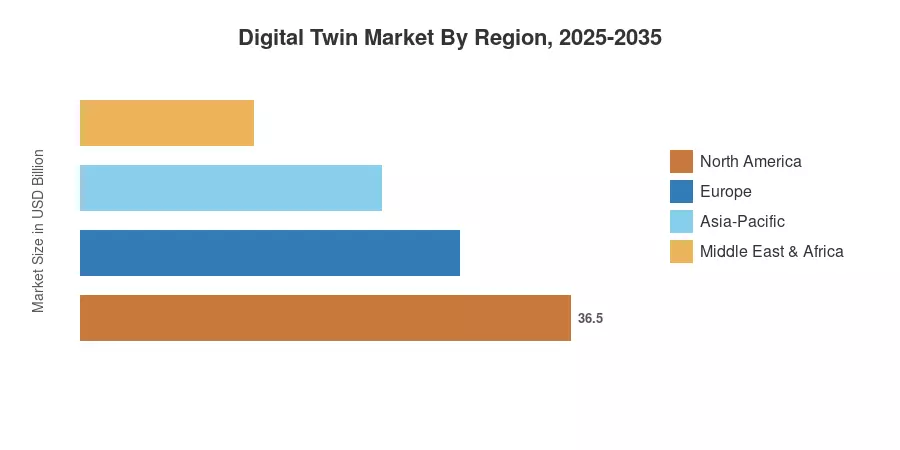

North America holds over 41.0% of the Digital Twin Market, driven by defense-sector digital-thread programs and hyperscaler cloud spending. Asia-Pacific is the fastest expanding area at an expected 28.10% CAGR, fueled by China’s “Digital China 2035” vision and India’s Smart Cities Mission. Europe has the second-highest share at around 26.5%, with Germany and France leading the way in adoption in the automotive and aerospace sectors. The Digital Twin Market will change the way enterprises develop, run and decommission physical assets of all sizes during the next decade.

Key Report Takeaways

• By Application

- Manufacturing accounted for 37.90% of the Digital Twin Market share in 2025, reflecting entrenched smart-factory deployments across automotive, electronics, and heavy industry

- Oil & Gas is forecast to expand at a 30.20% CAGR through 2035, as producers adopt asset-integrity digital twins to reduce unplanned downtime in offshore and refinery operations

• By Component

- Solutions and platforms captured 67.50% revenue share in the Digital Twin Market in 2025, led by simulation-software suites and IoT middleware

- Services are projected to grow at a 32.40% CAGR to 2035 as enterprises seek system integration and managed-twin expertise

• By Region

- North America led with 41.0% of the Digital Twin Market in 2025

- Asia-Pacific is set to rise at a 28.10% CAGR through 2035, driven by public digitalization programs in China, India, and Japan

MRFR’s proprietary sizing framework triangulates bottom-up vendor revenues, top-down macroeconomic variables and primary interviews with 120+ industry stakeholders to get both historical and projected estimations. All amounts are in current USD Billion and are calendar year-end values.