Electric Three Wheelers Market Summary

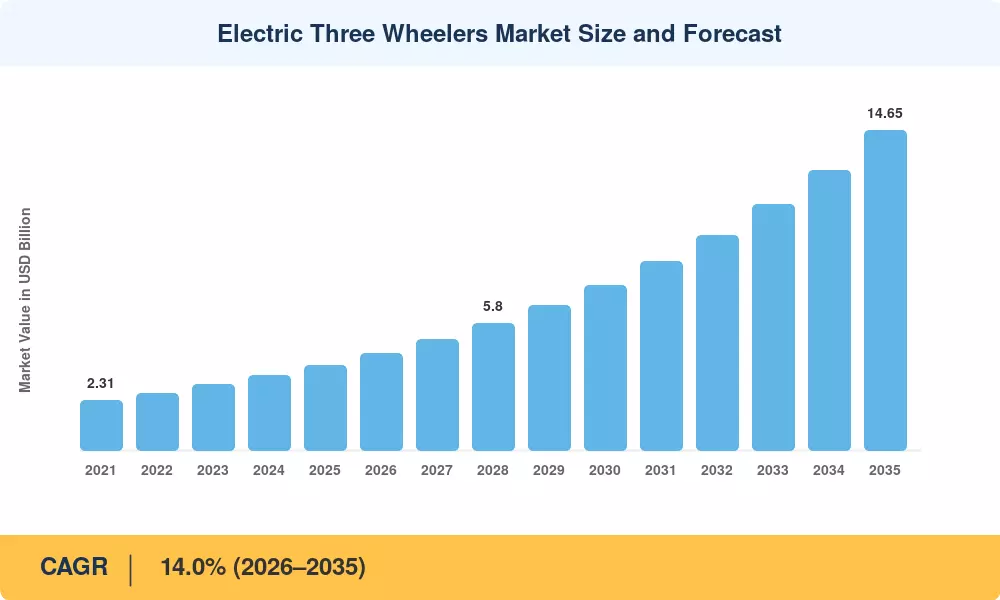

The Electric Three Wheeler Market was valued at USD 3.90 Billion in 2025, with the forecast period beginning at USD 4.50 Billion in 2026 and projected to reach USD 14.65 Billion by 2035, registering a CAGR of 14.0% from 2026 to 2035. India's PM E-DRIVE scheme and the proposed FAME-III programme, combined with the EU Fit-for-55 package and US Inflation Reduction Act commercial credits, have created a global policy environment that actively tilts fleet economics toward zero-emission three-wheelers [1]. These regulatory levers are accelerating adoption faster than organic demand alone would allow.

A structural technology shift is reshaping the Electric Three Wheeler Market from the inside out. Legacy lead-acid-powered vehicles — long the backbone of South Asian last-mile transport — are giving way to lithium-ion-powered platforms as pack-level prices dropped roughly 12% year-over-year through 2024 [2]. Battery swapping networks have also matured rapidly; one major Indian operator has completed over 50 million swaps across 1,400 stations, cutting commercial driver downtime from hours to minutes [3]. This infrastructure buildout is a critical enabler for fleet-scale electrification.

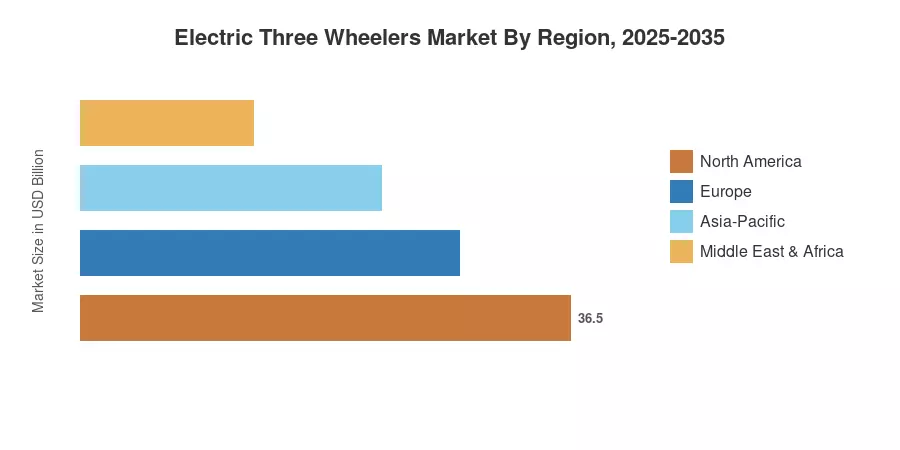

Asia-Pacific commands the Electric Three Wheeler Market with approximately 77% revenue share in 2025, anchored by India and China's massive installed fleets. The Middle East & Africa region is advancing at the fastest clip with a projected CAGR of 21.0%, driven by urbanization in sub-Saharan cities and new import incentives in the Gulf states [4]. Europe holds the second-largest share at around 8%, supported by L-category vehicle regulations and municipal zero-emission zones. As total-cost-of-ownership parity strengthens across regions, the coming decade will see electric three-wheelers transition from a niche product to a mainstream commercial vehicle platform.

Key Report Takeaways

• By End Use

- Passenger carriers held a dominant position in the Electric Three Wheeler Market with approximately 76% revenue share in 2025, driven by high-utilization urban commuter fleets across South and Southeast Asia.

- Goods carriers represent the fastest-expanding end-use segment, projected to grow at a CAGR of 20.0% through 2035 as last-mile logistics operators electrify delivery fleets.

• By Battery Type

- Lithium-ion battery systems are growing at a CAGR of 22.5%, steadily displacing lead-acid packs as cell-level costs decline and energy density improves.

• By Power Output

- The 2–4 kW power output segment accounted for approximately 47% of the Electric Three Wheeler Market in 2025, reflecting the predominance of low-speed urban passenger vehicles.

• By Charging Model

- Battery swapping as a charging model is projected to expand at a 25.8% CAGR, though fixed plug-in charging still holds roughly 82% share.

• By Region

- Asia-Pacific captured roughly 77% of the global Electric Three Wheeler Market revenue in 2025, with India and China as the two largest national markets.

- The Middle East & Africa region leads growth projections at a 21.0% CAGR, while Europe is expanding through regulatory incentives for L-category electric vehicles.

Market Size and Forecast (2021–2035)

Market Research Future's estimates for the Electric Three Wheeler Market draw on primary interviews with fleet operators, OEM shipment disclosures, battery import records, and government registration databases across 32 countries. Historical figures (2021–2024) use verified shipment and revenue data, while the forecast (2026–2035) applies a bottom-up model calibrated against policy timelines and lithium-ion cost curves.