Functional Safety Market Summary

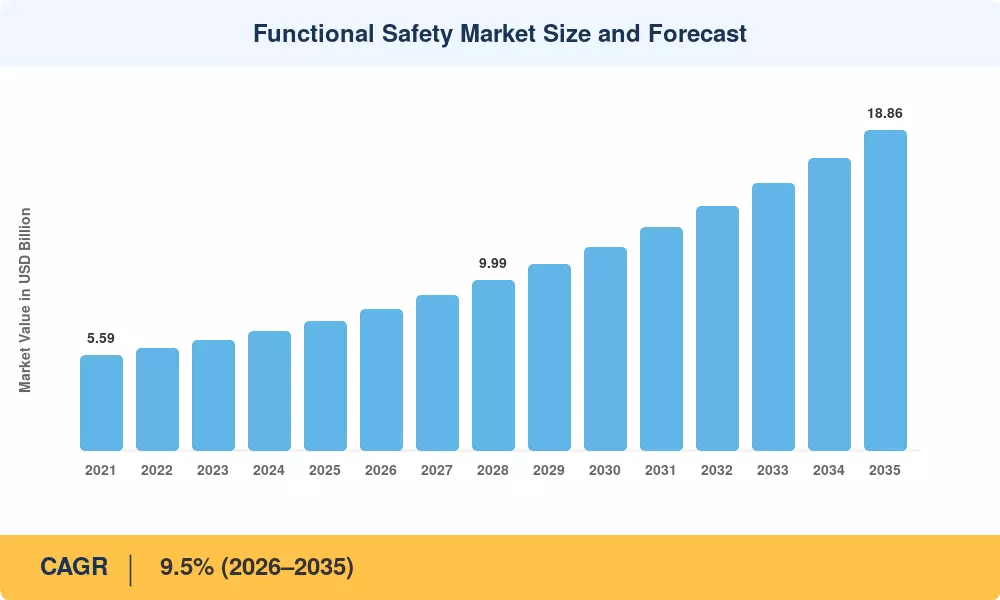

The Functional Safety Market was valued at USD 7.61 Billion in 2025 and is projected to grow from USD 8.33 Billion in 2026 to USD 18.86 Billion by 2035, registering a CAGR of 9.5% during the forecast period. Mandatory compliance with international standards such as IEC 61508 and the Seveso III Directive across chemical and petrochemical facilities has created non-discretionary demand for safety-instrumented systems, while ISO 26262 obligations tied to ADAS and electric vehicle architectures are pulling automotive OEMs into multi-year certification cycles [1][2].

A technology shift is underway as hardware-centric safety controllers give way to software-defined platforms capable of over-the-air parameter updates and cloud-hosted proof-test documentation. Industry 4.0 deployments are embedding SIL-rated logic solvers directly into distributed control architectures, collapsing what used to be standalone safety layers into integrated automation stacks. Global spending on smart manufacturing infrastructure exceeded USD 410 Billion in 2024, and a meaningful share of that capital is flowing into functional safety upgrades [3][4].

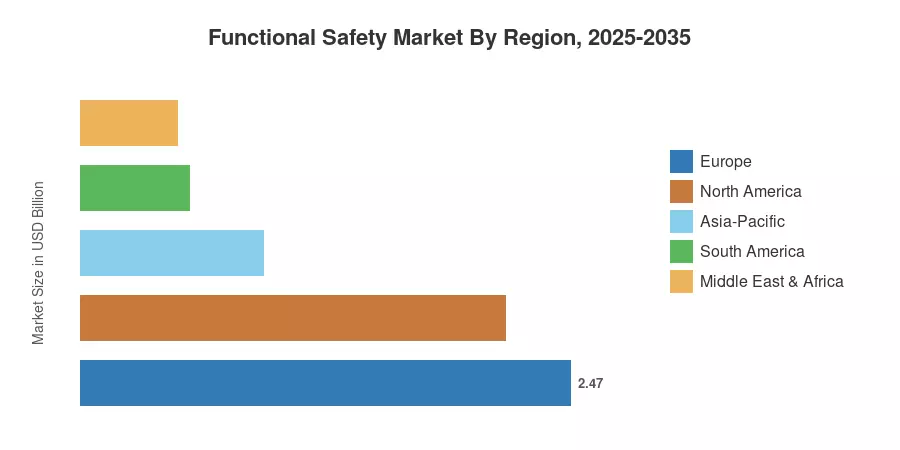

Europe retained the largest share of the Functional Safety Market at approximately 32.4% in 2025, anchored by stringent EU machinery and process safety directives. Asia-Pacific stands as the fastest-growing region with a projected 12.1% CAGR, driven by refinery and automotive plant expansions across China, India, and Southeast Asia. North America accounted for roughly 28.1% of global revenue, supported by OSHA process safety mandates and shale-sector modernization programs. As autonomous systems and AI-driven shutdown logic mature, the Functional Safety Market is poised for sustained double-digit expansion through the next decade [5][6].

Key Report Takeaways

• By Device Type

- Safety sensors commanded approximately 31.4% of the Functional Safety Market in 2025, reflecting broad deployment across process and discrete manufacturing environments.

- Programmable safety systems are forecast to expand at a 10.8% CAGR through 2035, fueled by software-defined controller adoption.

• By Safety System

- Emergency shutdown systems represented roughly 30.4% of total revenue in 2025, driven by oil and gas regulatory requirements.

- High-integrity pressure protection systems are projected to grow at a 10.9% CAGR, the fastest among safety system categories.

• By End-User Industry

- Oil and gas contributed an estimated 31.7% of the Functional Safety Market in 2025, making it the single largest vertical.

- Pharmaceuticals are expected to post a 10.8% CAGR through 2035 as batch-process validation standards tighten.

• By Region

- Europe held the dominant position in the Functional Safety Market with 32.4% share in 2025.

- Asia-Pacific is anticipated to register a 12.1% CAGR, outpacing all other regions.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining bottom-up revenue estimation from device and service line-items, top-down validation against industrial automation spending benchmarks, and qualitative inputs from safety engineering consultancies and certification bodies. Historical figures are calibrated against audited financial disclosures from leading suppliers, while forecast projections apply a regression-adjusted CAGR informed by capital expenditure cycles across end-user industries.