GDPR Services Market Summary

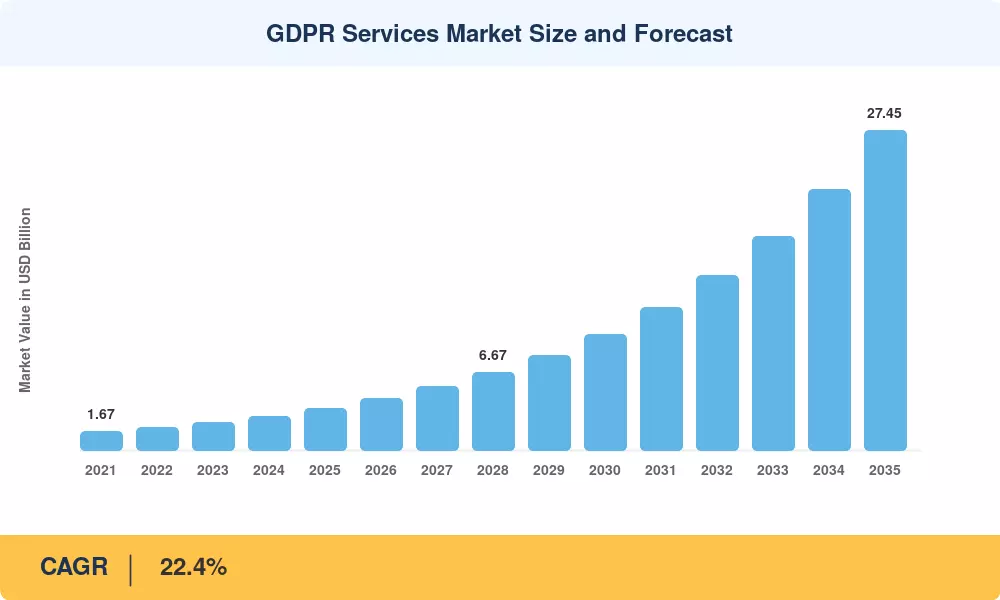

The GDPR Services Market reached USD 3.58 Billion in 2025 and is projected to grow from USD 4.45 Billion in 2026 to USD 27.45 Billion by 2035, registering a CAGR of 22.4% across the forecast window. European data-protection authorities issued more than EUR 1.3 billion in aggregate fines during 2024, shifting enterprise spending from reactive penalty mitigation toward sustained compliance architecture [1]. The EU-U.S. Data Privacy Framework, ratified in mid-2023, simultaneously opened new compliance obligations for transatlantic businesses, creating a durable revenue stream for specialized service providers.

A technology inflection point is reshaping how organizations address privacy obligations. Legacy spreadsheet-based registers and manual consent logs are giving way to AI-driven data-mapping engines, automated discovery platforms, and continuous monitoring dashboards capable of scanning petabytes in hours. estimated that enterprise spending on privacy management technology surpassed USD 2.5 billion globally in 2024, reflecting a 28% year-on-year jump [2]. Regulatory bodies across the EU have signaled stricter enforcement of data-protection-by-design mandates under the AI Act, reinforcing this technology shift.

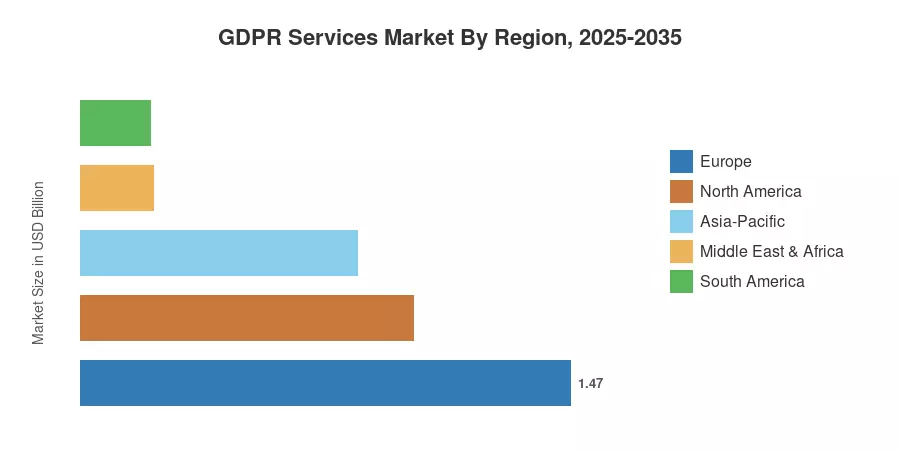

Europe commands approximately 41% of the GDPR Services Market, anchored by Germany, France, and the UK. Asia-Pacific stands as the fastest-growing region at a 23.2% CAGR through 2035, propelled by India's Digital Personal Data Protection Act and Japan's amended APPI. North America holds the second-largest share at roughly 28%, driven by state-level legislation in California, Virginia, and Colorado that borrows heavily from GDPR principles. The convergence of global privacy frameworks should sustain demand well beyond the current decade.

Key Report Takeaways — GDPR Services Market

By Deployment Type

- On-premises deployments accounted for 72.0% of GDPR Services Market revenue in 2025, reflecting regulated industries' preference for data residency control.

- Cloud-based GDPR Services Market solutions are forecast to expand at a 24.1% CAGR through 2035, driven by SaaS delivery models and lower total cost of ownership.

By Offering

- Solutions captured 62.0% of GDPR Services Market spending in 2025, led by consent management and data-discovery platforms.

- Managed and professional services within the GDPR Services Market are projected to grow at a 23.8% CAGR as organizations outsource complex compliance workflows.

By Organization Size

- Large enterprises controlled 73.0% of the GDPR Services Market in 2025.

- SMEs are expected to expand at a 24.0% CAGR to 2035, aided by affordable subscription-based privacy platforms.

By End User

- BFSI held a 37.0% share of the GDPR Services Market in 2025.

- Retail and consumer goods represent the fastest-growing vertical at a 23.0% CAGR.

By Region

- Europe led the GDPR Services Market with a 41.0% revenue share in 2025, supported by the most mature enforcement landscape globally.

- Asia-Pacific is projected to record a 23.2% CAGR to 2035, making it the fastest-growing region in the GDPR Services Market.

GDPR Services Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on bottom-up revenue modeling across deployment types, offerings, verticals, and geographies, triangulated with public financial disclosures of leading vendors, regulatory enforcement data, and primary interviews with 85+ privacy officers conducted in Q1 2025.