Graphite Market Summary

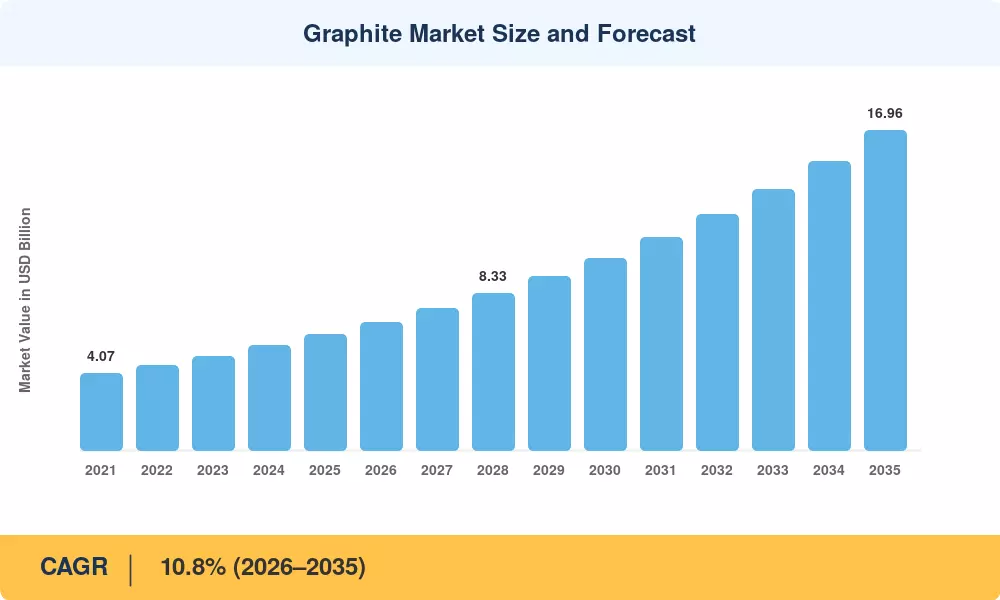

The global Graphite Market reached an estimated USD 6.14 Billion in 2025 and is positioned to grow from USD 6.74 Billion in 2026 to USD 16.96 Billion by 2035, registering a CAGR of 10.8% across the forecast period. This expansion is anchored in record capital commitments to lithium ion battery gigafactories — the U.S. Department of Energy alone channeled over USD 3.1 Billion into battery material supply chains through the Bipartisan Infrastructure Law, while Europe's Critical Raw Materials Act designated graphite as strategic, unlocking preferential permitting for new processing hubs[2].

A generational technology shift is reshaping the Graphite Market from the supply side. Legacy blast-furnace steelmaking is yielding ground to electric-arc-furnace (EAF) routes that consume graphite electrodes at roughly three times the intensity per ton of steel. Simultaneously, battery anode materials producers are integrating mine-to-anode operations to reduce dependence on third-party synthetic graphite toll-processors, with over USD 1.9 Billion in capacity announcements across North America and Europe during 2024–2025 [3][4].

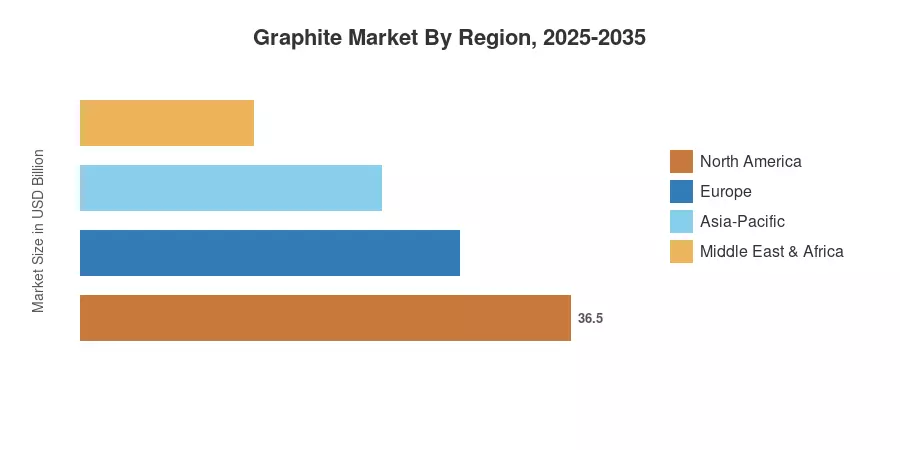

Asia-Pacific commands roughly 51.5% of global revenue, led by China's dominance in natural graphite mining and anode processing. The region also posts the fastest CAGR at 12.3% through 2035. North America ranks as the second-largest contributor with an 18% share, driven by reshoring incentives under the Inflation Reduction Act. Europe follows closely at 20%, propelled by EV battery localization mandates. The Graphite Market trajectory points to a decisive decade of geographic diversification and demand intensification [5].

Key Report Takeaways

• By Type

- Synthetic graphite captured 63.5% of the Graphite Market in 2025, reflecting strong demand from EAF steelmaking and high purity graphite applications in semiconductors

- Natural graphite is projected to expand at a 13.3% CAGR through 2035, fueled by cost-competitive battery anode materials sourcing

• By Application

- Batteries accounted for 44.2% of Graphite Market revenue in 2025, as lithium ion battery graphite consumption scaled alongside global gigafactory buildouts

- Graphite electrodes remain the second-largest application segment, underpinned by accelerating EAF steel capacity additions worldwide

• By End-User Industry

- Automotive held the largest share of the Graphite Market at 47.2% in 2025, reflecting the EV production ramp across major OEMs

- Electronics end users are advancing at a CAGR of 14.6%, tied to rising semiconductor wafer demand for high purity graphite components

• By Region

- Asia-Pacific controlled 51.5% of the Graphite Market in 2025

- North America is attracting USD 1.9 Billion in new graphite processing investments through 2027

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework combines primary industry interviews, trade data reconciliation, and bottom-up demand modeling validated against public company disclosures and government production statistics.