Hardware Security Modules Market Summary

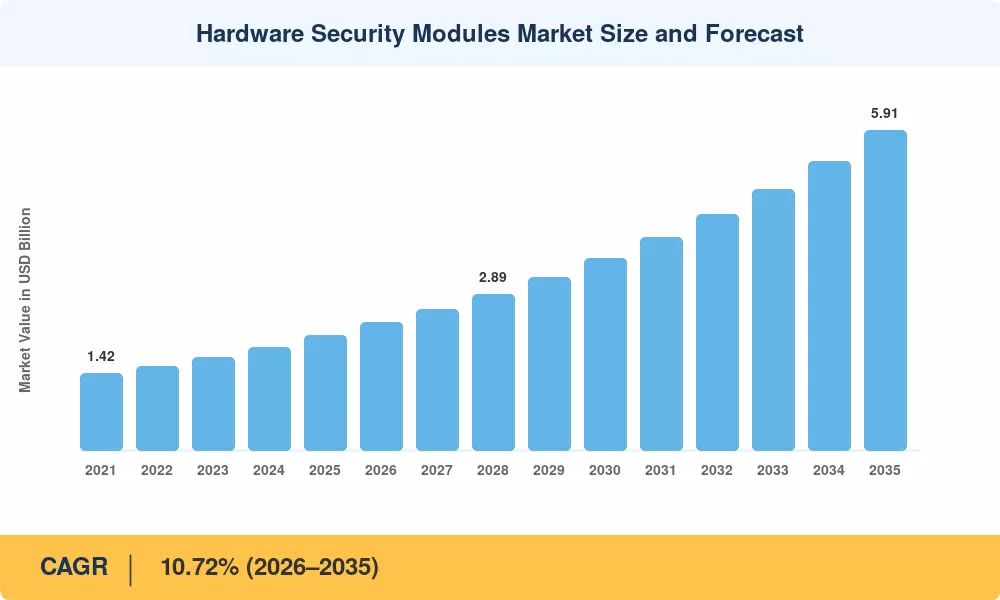

The Hardware Security Modules Market stood at USD 2.13 Billion in 2025, is projected to reach USD 2.36 Billion in 2026, and will climb to USD 5.91 Billion by 2035, registering a CAGR of 10.72% during the 2026–2035 forecast period. Two catalysts are reshaping purchasing behavior across enterprises: mandatory encryption-at-rest requirements embedded in updated PCI DSS 4.0 guidelines and the accelerating migration of sovereign key management workloads into certified tamper-resistant appliances [1]. These regulatory forces have shifted HSM procurement from discretionary IT spending to compliance-mandated capital allocation.

A generational technology transition is underway. Legacy software-based key stores and first-generation PKCS#11 appliances are being replaced by FIPS 140-3 Level 3 validated modules capable of handling post-quantum cryptographic algorithms. Cloud service providers invested an estimated USD 680 million in HSM infrastructure buildouts during 2024 alone [2], reflecting the urgency to offer customers hardware-rooted trust anchors within multi-tenant environments. Subscription-based cloud HSM services now complement traditional on-premise appliance sales, opening the Hardware Security Modules Market to mid-market enterprises that previously lacked the budget for dedicated hardware.

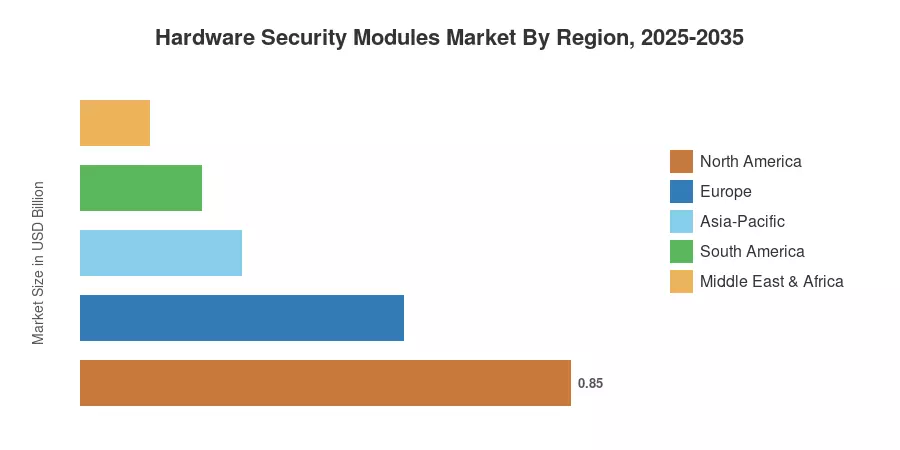

North America commands roughly 39.7% of the Hardware Security Modules Market, driven by early federal mandates such as NIST SP 800-131A and CMMC certification requirements. Asia-Pacific delivers the fastest regional growth at a 13.08% CAGR through 2035 as hyperscalers localize data-sovereignty platforms across India, Japan, and Southeast Asia. Europe holds the second-largest share at approximately 26.3%, buoyed by MiCA-driven crypto-custody regulations and eIDAS 2.0 digital identity infrastructure investments. The convergence of quantum computing timelines with existing cryptographic debt positions the Hardware Security Modules Market for sustained double-digit expansion through the next decade.

Key Report Takeaways

• By Deployment & Type

- On-premise appliances captured approximately 76.9% of Hardware Security Modules Market revenue in 2025, reflecting enterprise preference for physically controlled key boundaries in regulated sectors.

- Cloud-hosted HSM deployments represent the fastest-growing type segment, advancing at an 11.55% CAGR as managed service models reduce the total cost of ownership for distributed workloads.

- General-purpose HSM units accounted for 63.6% of type-level revenue share in 2025, serving authentication, code-signing, and database encryption use cases.

• By Application & End-User

- Payment processing applications held 40.8% of the Hardware Security Modules Market in 2025, anchored by EMV terminal deployments and real-time payment rails.

- The BFSI vertical represented 36.3% of end-user demand in 2025, while cloud service providers are projected to record the highest vertical CAGR at 11.78% through 2035.

• By Region

- North America led the Hardware Security Modules Market with 39.7% share in 2025, followed by Europe at 26.3%.

- Asia-Pacific is forecast to post a 13.08% CAGR through 2035, fueled by sovereign data localization mandates across India and ASEAN economies.

Market Size and Forecast (2021–2035)

Market Research Future's sizing framework integrates bottom-up revenue modeling from vendor disclosures, import-export databases, and end-user procurement surveys. Historical figures (2021–2024) reflect audited shipment data, while 2025 is the calibrated base year. Forecast values (2026–2035) apply segment-weighted growth assumptions validated against regulatory pipeline analysis and capital expenditure schedules from hyperscale cloud operators.