Industrial Gases Market Summary

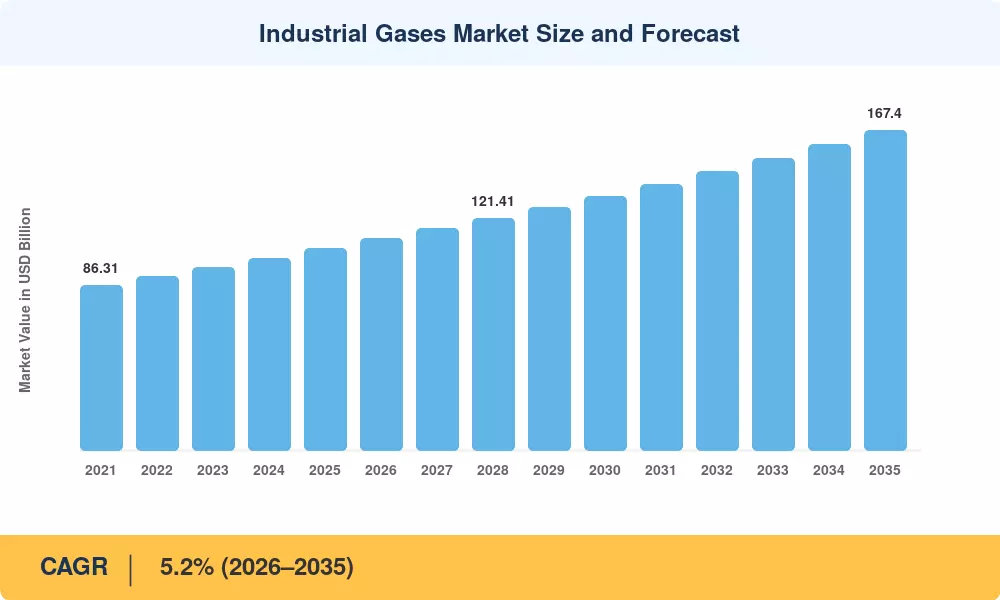

The Industrial Gases Market reached an estimated USD 105.8 billion in 2025 and is projected to grow from USD 111.3 billion in 2026 to USD 167.4 billion by 2035, registering a CAGR of 5.2% during the forecast period (2026–2035). Two forces are accelerating this trajectory: the global push toward green hydrogen production — backed by over USD 280 billion in announced electrolyzer and hydrogen hub investments worldwide [1] — and the rapid expansion of semiconductor fabrication, which demands ultra-high-purity nitrogen, argon, and specialty gas blends at unprecedented volumes. The Industrial Gases Market is no longer a commodity story; it is becoming a technology-intensive growth sector.

On-site industrial gas generator installations and pipeline supply networks are replacing legacy merchant distribution arrangements where liquid nitrogen oxygen industrial gas was trucked from centralized air separation units (ASUs) to end customers. This is reflected in Linde's announcement of a USD 2 billion investment cycle in on-site hydrogen industrial gas supply installations across the US Gulf Coast in 2024 [2]. Meanwhile, carbon capture, utilization, and storage (CCUS) operations under the U.S. 45Q tax credit are establishing completely new demand pools for the industrial food-grade and technical grade streams of carbon dioxide CO2.

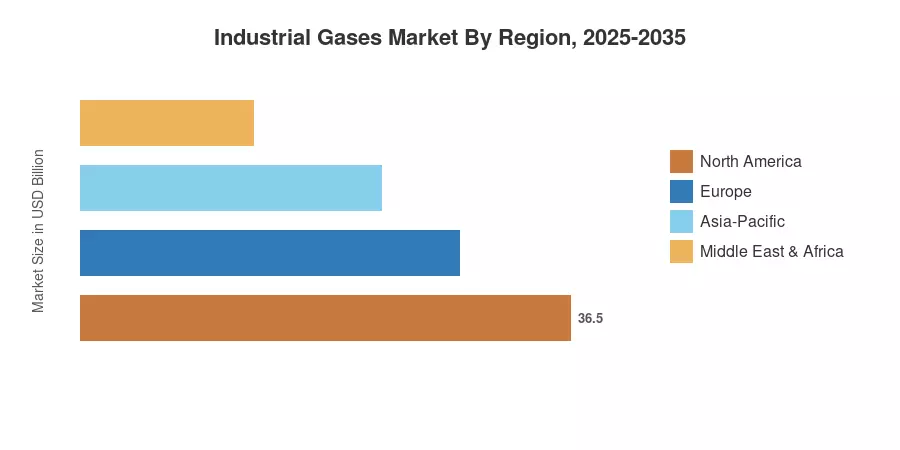

North America is the largest market for industrial gases, with a share of ~33% in worldwide revenues, driven by petrochemical refining hubs and the hydrogen economy buildout. With a CAGR of 6.4%, Asia-Pacific is the fastest-growing market, driven by China’s steel decarbonization standards and India’s burgeoning healthcare oxygen infrastructure. Europe accounts for the second greatest part of over 27%, with the EU Hydrogen Strategy allocating EUR 470 billion for clean hydrogen until 2050 [3]. Industrial Gases Market – Structural Demand Growth Expected in All Major Geographies Over the Next Decade

.

Key Report Takeaways

• By Gas Type

- Oxygen holds the largest revenue share at approximately 28% of the Industrial Gases Market, driven by steelmaking, healthcare, and wastewater treatment demand

- Nitrogen is growing at a CAGR of 5.5%, reflecting surging electronics fab and food-preservation applications where liquid nitrogen oxygen industrial gas is critical

- Hydrogen industrial gas supply is projected to reach USD 32.6 billion by 2035, as green electrolysis capacity scales globally

• By Distribution Mode

- Bulk industrial gas supply contract arrangements account for roughly 42% of total delivery revenue in the Industrial Gases Market

- On-site industrial gas generator deployments are expanding at a CAGR of 6.1%, especially in refinery and semiconductor clusters

• By Geography

- North America leads the Industrial Gases Market with a 33% revenue share anchored in petrochemicals and hydrogen hubs

- Asia-Pacific registers the highest CAGR at 6.4%, with China and India as primary demand engines

- Europe contributes approximately USD 28.6 billion in 2025, underpinned by decarbonization policy

Industrial Gases Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a market-sizing methodology that blends bottom-up revenue estimation from company filings and trade association shipment statistics (CGA, EIGA, JIGA) with top-down macro-economic indicators. Historical data (2021-2024) are based on reported revenues and production volumes of the top 10 suppliers, and prospective values (2026-2035) are based on segment-specific growth assumptions confirmed against IEA and World Bank industrial output predictions.