Infrared Sensor Market Summary

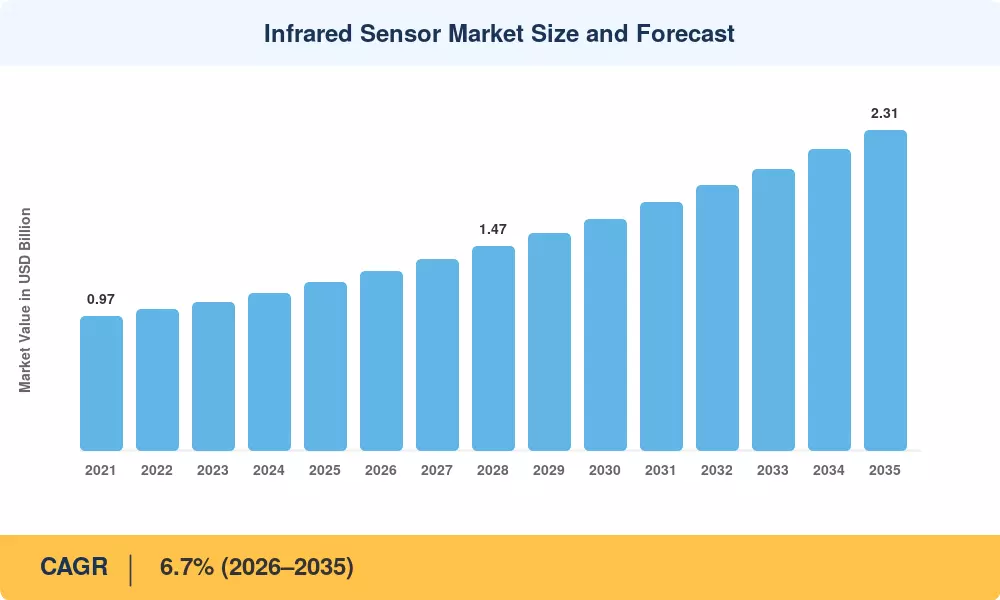

The Infrared Sensor Market was valued at USD 1.21 Billion in 2025, is projected to reach USD 1.29 Billion in 2026, and is expected to grow to USD 2.31 Billion by 2035, registering a CAGR of 6.7% during the 2026–2035 forecast period. Two catalysts anchor this trajectory: mandatory automotive occupant-monitoring regulations under Euro NCAP's 2026 roadmap and growing sovereign data-processing mandates across the European Union and China that favor on-device inference over cloud-reliant architectures. These policy forces are pulling infrared sensing out of its traditional niche and into mainstream consumer and industrial applications. The Infrared Sensor Market is responding with significant capital reallocation across the value chain.

A fundamental technology shift is reshaping the Infrared Sensor Market. Legacy lead-salt and pyroelectric detectors are yielding to chip-scale quantum cascade arrays, colloidal quantum-dot imagers, and wafer-level-packaged uncooled microbolometers. Wafer-level packaging alone has compressed sensor module costs by roughly 30% since 2021, according to Yole Intelligence estimates [1]. Government programs such as the U.S. Department of Defense's Third Offset Strategy continue to direct over USD 2 billion annually toward next-generation electro-optical systems, sustaining demand for higher-performance focal-plane arrays [2].

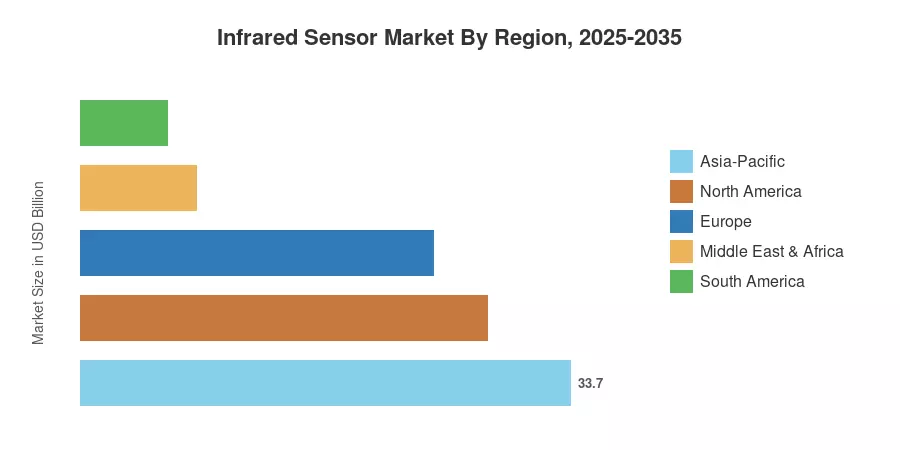

Asia-Pacific commands the largest share of the Infrared Sensor Market at approximately 33.7% of global revenue, driven by China's sprawling smart-city surveillance rollouts and Japan's precision-manufacturing inspection lines. Africa is the fastest-growing region, posting an estimated 8.8% CAGR through 2035, fueled by agricultural modernization and perimeter-security deployments. North America holds the second-largest position with roughly 28.0% share, underpinned by defense procurement cycles and the rapid buildout of smart-building HVAC optimization systems. As edge AI chipsets become more affordable, the Infrared Sensor Market is poised to penetrate wearable health monitors and autonomous vehicle cabins at scale over the coming decade.

Key Report Takeaways

• By Technology

- Uncooled detectors held an estimated 60.6% share of the Infrared Sensor Market in 2025, reflecting their cost advantage in high-volume commercial applications.

• By Wavelength

- The short-wave infrared (SWIR) wavelength band is forecast to expand at an 8.3% CAGR through 2035, driven by semiconductor wafer inspection and moisture-detection use cases.

- Long-wave infrared (LWIR) accounted for approximately 43.4% of revenue in 2025, anchored by building automation and perimeter security demand.

• By Application

- Security and surveillance represented roughly 36.1% of the Infrared Sensor Market revenue in 2025, the largest single application vertical.

- Precision agriculture and livestock monitoring is the fastest-rising application, with an 8.0% CAGR to 2035.

• By End-User

- Healthcare end users are growing at an estimated 8.9% CAGR, propelled by wearable diagnostics and infection-screening deployments.

• By Region

- Asia-Pacific led the Infrared Sensor Market with 33.7% of global revenue in 2025.

- Africa is projected to grow at an 8.8% CAGR through 2035, the highest of any region.

- North America accounted for approximately 28.0% share, sustained by defense and smart-building investment.

Infrared Sensor Market Size and Forecast (2021–2035)

Market sizing combines bottom-up revenue aggregation across sensor OEMs, system integrators, and aftermarket channels with top-down cross-validation against semiconductor shipment data from WSTS and regional trade statistics. Historical figures reflect actual reported revenues, while the forecast period applies the calibrated 6.7% CAGR alongside segment-level growth differentials identified through primary interviews with procurement executives and technology officers across 14 countries.