IoT Integration Market Summary

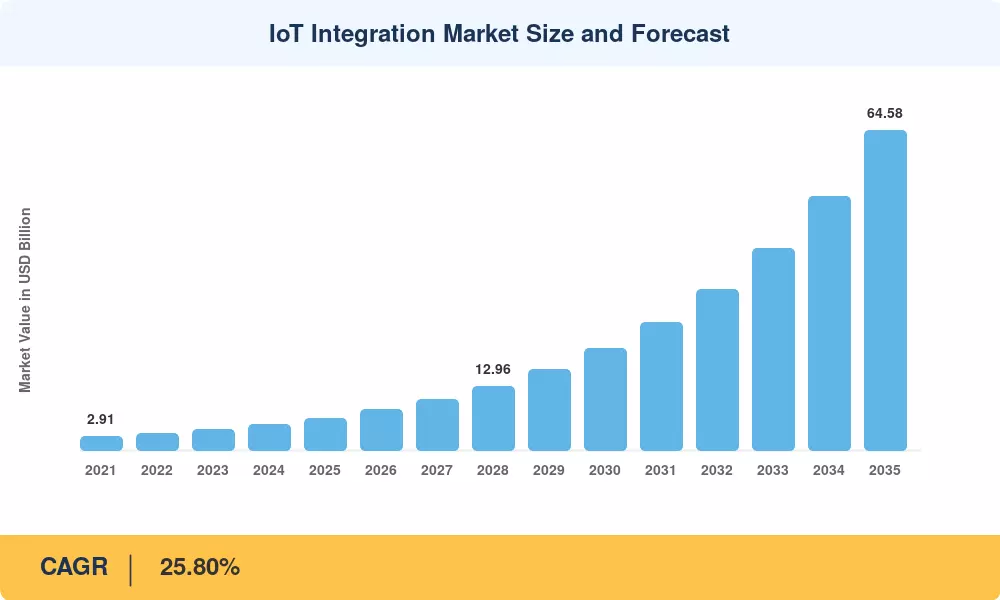

The IoT Integration Market reached USD 6.50 billion in 2025 and is forecast to grow from USD 8.18 billion in 2026 to USD 64.58 billion by 2035, registering a 25.80% CAGR across the forecast window. Accelerating 5G rollouts and enterprise digital-transformation mandates — the U.S. CHIPS and Science Act alone earmarked over USD 52 billion for semiconductor and connected-infrastructure programs [1] — are channeling investment toward integration specialists capable of bridging multi-vendor IoT ecosystems. Governments in the EU, India, and South Korea have concurrently launched smart-city and Industry 4.0 frameworks that explicitly require certified IoT Integration Market participants to manage cross-platform deployments [2].

Legacy point-to-point interfaces are making way to cloud-native orchestration layers and edge-computing fabrics that bring together sensors, gateways and analytics pipelines into a single control plane. The World Economic Forum predicts that by 2027, the number of IoT devices globally will exceed 30 billion, which will put pressure on the ad-hoc integration methods and will move the organizations towards the managed integration services [3]. These professional and managed services are becoming a larger slice of overall IoT spend as businesses opt for speed to value rather than building capabilities in-house.

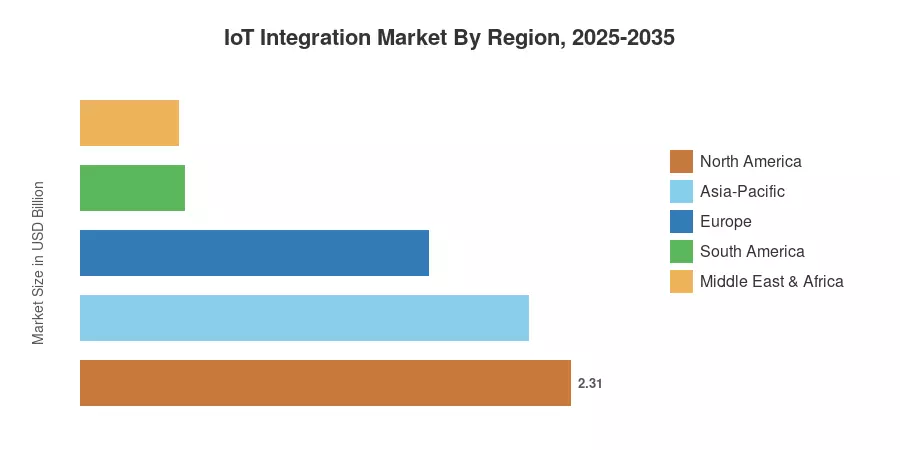

North America accounted for around 35.50% of the IoT Integration Market in 2025, led by hyperscaler cloud ecosystems and federal smart-infrastructure schemes. The Asia-Pacific region is witnessing the fastest growth, with a CAGR of 32.50%, owing to the “Digital China 2035” strategy of China and the Production-Linked Incentive program of India for electronics manufacturing [4]. Europe is the second largest region with 25.20%, anchored by the EU Data Act and Horizon Europe IoT research centers [5]. Integrators that can combine deep vertical domain understanding with scalable, security-first systems will be rewarded over the next decade.

Key Report Takeaways

• By Service

- Device and Platform Management commanded a 31.00% share of the IoT Integration Market in 2025, reflecting demand for unified fleet orchestration across heterogeneous sensor estates.

- Network Management services are projected to grow at a 27.90% CAGR through 2035, propelled by private 5G deployments and network-slicing requirements.

• By Application

- Smart Buildings and Home Automation represented 35.60% of IoT Integration Market revenue in 2025, as property owners pursue energy-optimization and occupant-experience upgrades.

- Smart Healthcare is set to expand at a 29.20% CAGR, driven by remote-patient-monitoring mandates and FDA digital-health pre-certification pathways.

• By Geography

- North America accounted for the largest regional share of the IoT Integration Market, underpinned by hyperscaler partnerships and defense-sector IoT modernization.

- Asia-Pacific leads all regions with a 32.50% CAGR, backed by massive government-led smart-city initiatives across China, India, and ASEAN economies.

IoT Integration Market Size and Forecast (2021–2035)

MRFR projections are based on a combination of bottom-up vendor-revenue analysis and top-down demand modeling, which are then validated through regulatory filings, enterprise IT surveys and macroeconomic factors. Historical statistics (2021–2024) are based on audited financial filings. Forecast predictions (2026–2035) are based on a compound annual growth model calibrated to technology-adoption S-curves and anticipated infrastructure investments.