Laboratory Equipment Market Summary

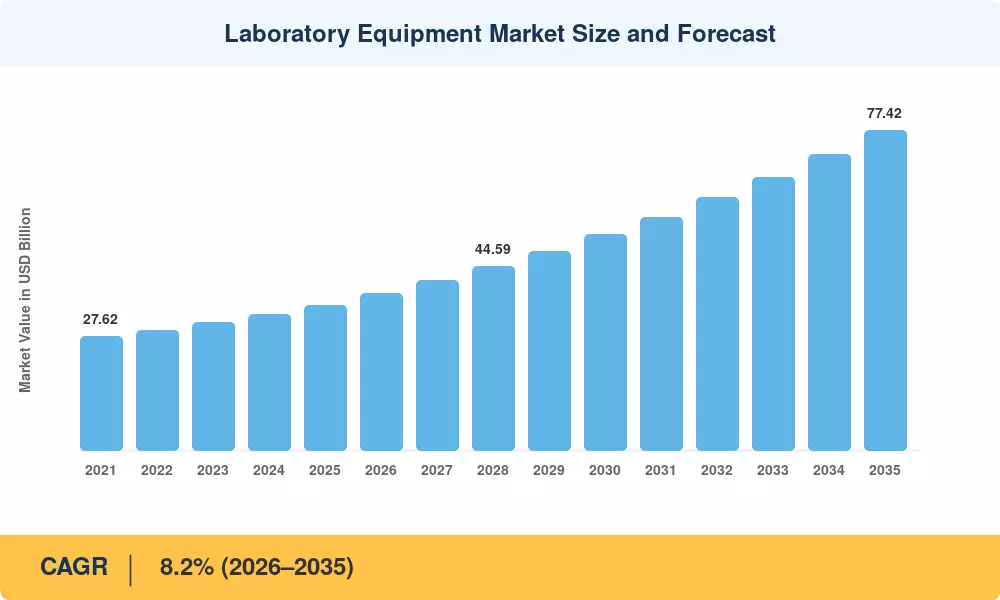

The Laboratory Equipment Market size was valued at USD 35.20 Billion in 2025, and the market is projected to grow from USD 38.09 Billion in 2026 to USD 77.42 Billion by 2035, registering a CAGR of 8.2% during the forecast period 2026–2035. Two catalysts are anchoring this trajectory: biopharmaceutical R&D spending, which crossed USD 205 Billion globally in 2024 [1], and the rising incidence of non-communicable diseases, responsible for roughly 41 million deaths each year according to the WHO [2]. Together, these forces are compelling hospitals, reference laboratories, and contract research organizations to expand testing infrastructure at an unprecedented pace.

Underneath these demand drivers sits a technology shift that is rewriting procurement cycles. Legacy manual benchtop workflows are giving way to fully integrated platforms that combine sample preparation, analysis, and data management in closed-loop systems. Single-use technologies and modular consumable kits are shortening equipment replacement intervals, while public-sector net-zero mandates are pushing suppliers toward low-carbon manufacturing and take-back programs. The Laboratory Equipment Market is therefore evolving from a capital-heavy, replacement-driven cycle into a consumables-intensive, service-oriented ecosystem.

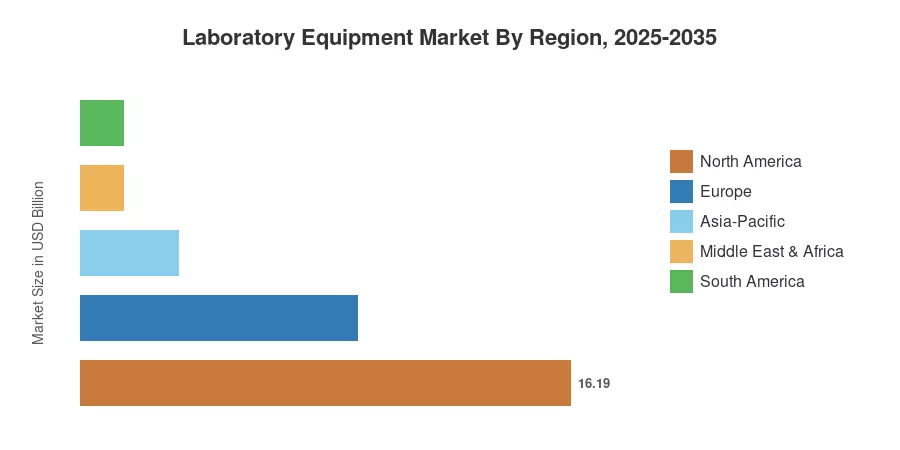

North America commanded a 46% share of the Laboratory Equipment Market in 2025, buoyed by NIH funding levels and a dense network of pharmaceutical headquarters. Asia-Pacific is the fastest-growing region, projected to expand at a 9.2% CAGR through 2035 as China, India, and South Korea ramp up clinical laboratory capacity [4]. Europe holds approximately 26% of spending, anchored by Horizon Europe research grants and IVD Regulation compliance upgrades. The decade ahead will reward vendors that balance instrument innovation with sustainability credentials and service-model flexibility.

Key Report Takeaways

• By Product Type

- Laboratory equipment captured roughly 51% of the Laboratory Equipment Market revenue in 2025, reflecting sustained capital spending on automated analyzers and imaging platforms.

- Laboratory disposables are forecast to expand at a 10.3% CAGR through 2035, driven by single-use bioreactor linings and pre-sterilized consumable kits.

• By Application

- Clinical diagnostics led the Laboratory Equipment Market with approximately 38% of spending in 2025, underpinned by hospital-based chemistry and hematology volumes.

- Genomics and proteomics applications are set to advance at a 10.5% CAGR, fueled by precision-medicine adoption and next-generation sequencing cost reductions.

• By End User

- Hospitals and clinics accounted for 43% of the Laboratory Equipment Market in 2025.

- Contract research organizations are projected to grow at an 11.2% CAGR through 2035, as pharma companies increasingly outsource early-stage assay development.

• By Region

- North America held a 46% share of the Laboratory Equipment Market in 2025, driven by NIH-funded academic research and large-scale reference laboratory networks.

- Asia-Pacific is the fastest-growing region with a 9.2% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from company filings, import–export databases, and regulatory device registrations. Forecast projections combine bottom-up end-user demand modeling with top-down macroeconomic adjustment to produce a consistent 2026–2035 outlook for the Laboratory Equipment Market.