Maize Market Summary

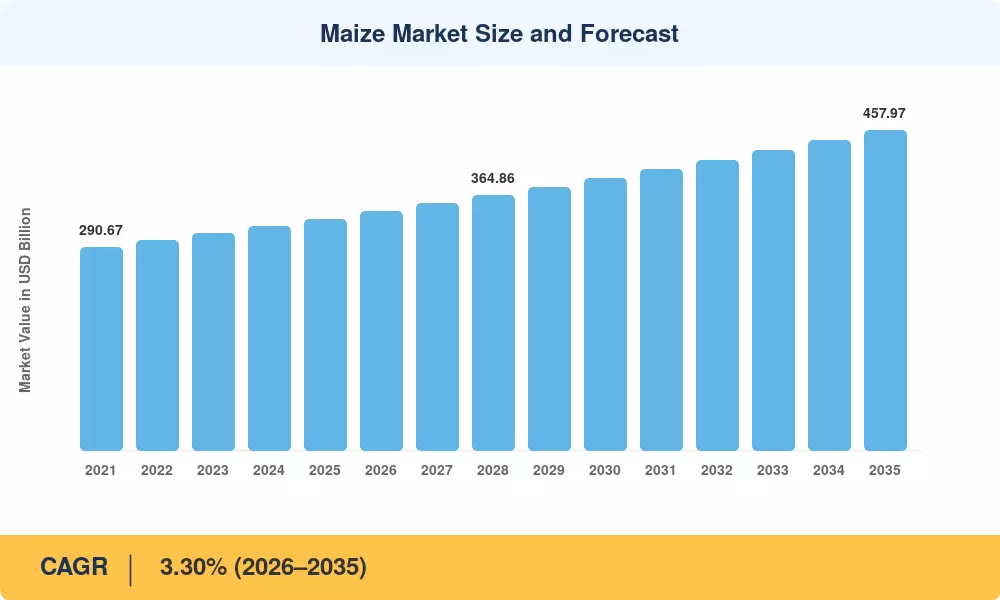

The global maize market reached an estimated USD 331.00 billion in 2025 and is projected to grow from USD 341.92 billion in 2026 to USD 457.97 billion by 2035, registering a CAGR of 3.30% during the forecast period. Biofuel blending mandates in the United States and Brazil, coupled with expanding livestock populations across the Asia-Pacific, remain the two most powerful demand catalysts for corn grain production and trade. The February 2025 reversal of Mexico's biotech-maize import ban removed a critical trade friction point and reopened a corridor worth roughly USD 4.7 billion in annual commodity flow [2].

A structural transformation is reshaping corn cultivation and harvesting practices worldwide. Legacy open-pollinated varieties are steadily giving way to high-yield hybrid and genetically modified seeds that tolerate drought stress and support denser planting configurations. Corteva Agriscience and Bayer CropScience have committed over USD 2.8 billion in combined R&D spending on short-stature maize hybrids designed for mechanized harvesting, signaling the pace of innovation in the maize market [3]. Meanwhile, on-farm grain storage infrastructure is expanding at roughly 6% annually, giving producers greater pricing flexibility and reducing post-harvest losses that historically eroded 12–15% of output in sub-Saharan Africa [4].

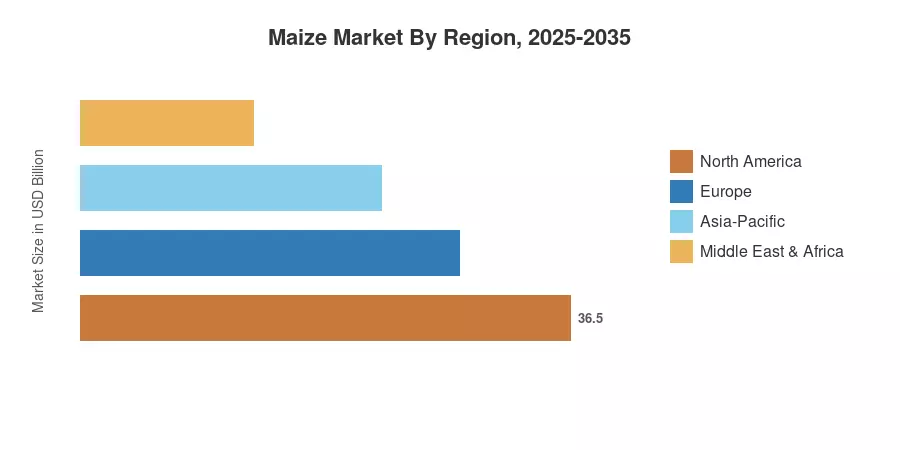

North America commands approximately 37.5% of the global maize market, anchored by the U.S. Corn Belt's unmatched yield density and ethanol refining capacity. Asia-Pacific stands as the fastest-growing region with a projected CAGR of 5.35%, driven by rising demand for maize as food feed and fuel across China, India, and Southeast Asia. Europe holds the second-largest share at roughly 22%, propelled by livestock feed requirements and expanding maize starch and ethanol uses in bio-based packaging. The next decade will test how effectively trade frameworks and climate-resilient agronomy can keep pace with surging global consumption.

Key Report Takeaways

• By Type

- Yellow maize accounted for roughly 68% of the global maize market value in 2025, reflecting dominant use in animal feed and ethanol refining.

- White maize is forecast to grow at a 3.85% CAGR through 2035, propelled by food-grade consumption in Africa and Central America.

• By Application

- Animal feed represented the largest end-use of the maize market, valued at approximately USD 138.80 billion in 2025.

- Industrial uses — including maize starch and ethanol uses — are expanding at a 4.10% CAGR, the fastest among application segments.

- Food and beverages held a 19% share of the maize market globally, supported by rising demand for corn-based snack and cereal products.

• By Region

- North America led the maize market with 37.5% revenue share in 2025, driven by U.S. ethanol mandates and export infrastructure.

- Asia-Pacific is projected to register the highest CAGR of 5.35%, fueled by expansion of corn grain production and trade in China and India.

Maize Market Size and Forecast (2021–2035)

MRFR's market sizing integrates FAO production statistics, USDA Foreign Agricultural Service trade data, national grain board pricing indices, and proprietary demand models triangulated against industry interviews with grain traders, seed companies, and ethanol producers[5].