Malaria Diagnostics Market Summary

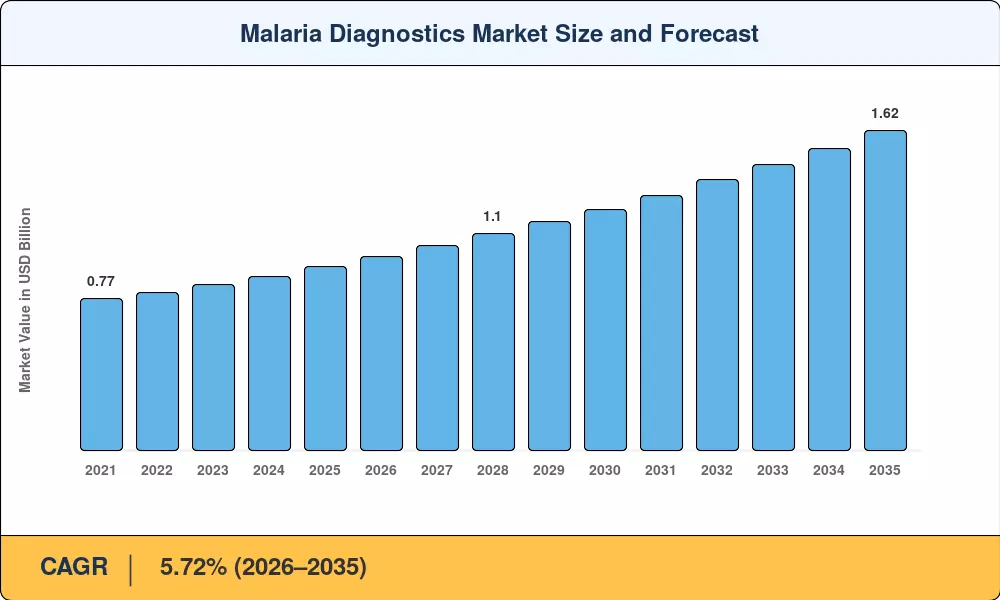

The Global Malaria Diagnostics Market size was valued at USD 0.93 Billion in 2025, and the market is projected to grow from USD 0.98 Billion in 2026 to USD 1.62 Billion by 2035, registering a CAGR of 5.72% during the forecast period 2026–2035. This trajectory reflects sustained funding commitments from the Global Fund and bilateral donors, which have collectively channeled over USD 4.1 billion into malaria control since 2020 [2]. WHO's updated policy guidance on dual-antigen detection and molecular confirmation has compelled national malaria programs to overhaul procurement strategies, directly lifting the Malaria Diagnostics Market beyond its pre-pandemic growth trend.

A technology shift is redefining how health systems detect and respond to infections. Traditional light microscopy, long considered the gold standard, is steadily giving way to high-sensitivity molecular platforms and AI-assisted image recognition systems. India's National Center for Vector Borne Diseases Disease Control allocated USD 38 million in 2024 to deploy isothermal amplification kits across 14 high-burden states, signaling a broader move toward point-of-care molecular testing [3]. This transition accelerates the Malaria Diagnostics Market as procurement agencies prioritize accuracy over per-unit cost.

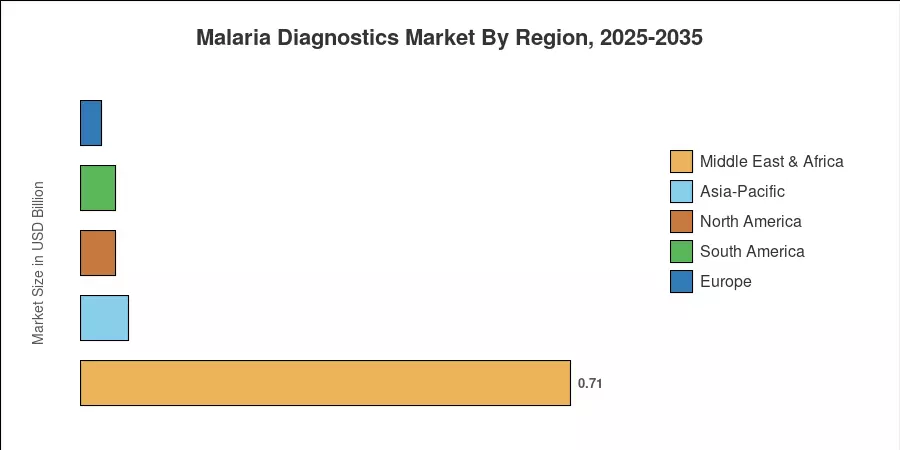

The Middle East & Africa region dominates the Malaria Diagnostics Market with an estimated 76.2% share of global revenue, driven by sub-Saharan Africa's endemic burden and sustained multilateral procurement volumes. Asia-Pacific represents the fastest-growing region at a projected CAGR of 7.54%, fueled by elimination campaigns in India, Indonesia, and Myanmar [4]. South America holds a meaningful share as Amazonian basin countries scale up community-based screening programs. The Malaria Diagnostics Market is positioned to accelerate through the forecast period as elimination-phase diagnostics demand increasingly sophisticated testing platforms.

Key Report Takeaways

• By Technology

- Rapid diagnostic tests captured approximately 56.5% of the global Malaria Diagnostics Market revenue in 2025, anchored by mass procurement through the Global Fund and PMI channels.

- Molecular diagnostics are projected to register the strongest segment CAGR of 6.28% through 2035, reflecting health system investment in sub-patent parasite detection.

- Next-generation platforms, including CRISPR-based assays and AI-powered microscopy readers, are gaining regulatory traction and represent the highest-value emerging technology category.

• By End User

- Clinics accounted for the largest end-user share at an estimated 55.8% of the Malaria Diagnostics Market revenue in 2025, driven by decentralized testing mandates.

- Diagnostic centres are forecast to grow at a leading 6.65% CAGR through 2035 as referral networks expand.

• By Region

- The Middle East & Africa region commanded over three-quarters of global revenue in 2025.

- Asia-Pacific is projected to post a 7.54% CAGR through 2035 as India and Southeast Asia intensify elimination-phase surveillance.

Market Size and Forecast (2021–2035)

Market Research Future's estimates integrate WHO World Malaria Report case data, Global Fund procurement records, national health expenditure surveys, and proprietary demand modeling. Historical figures (2021–2024) are derived from audited manufacturer shipments and donor disbursement data. Forecast projections (2026–2035) apply a calibrated CAGR anchored to the base year 2025, with adjustments for programmatic funding cycles and technology adoption curves[2].