In Vitro Diagnostics Market Summary

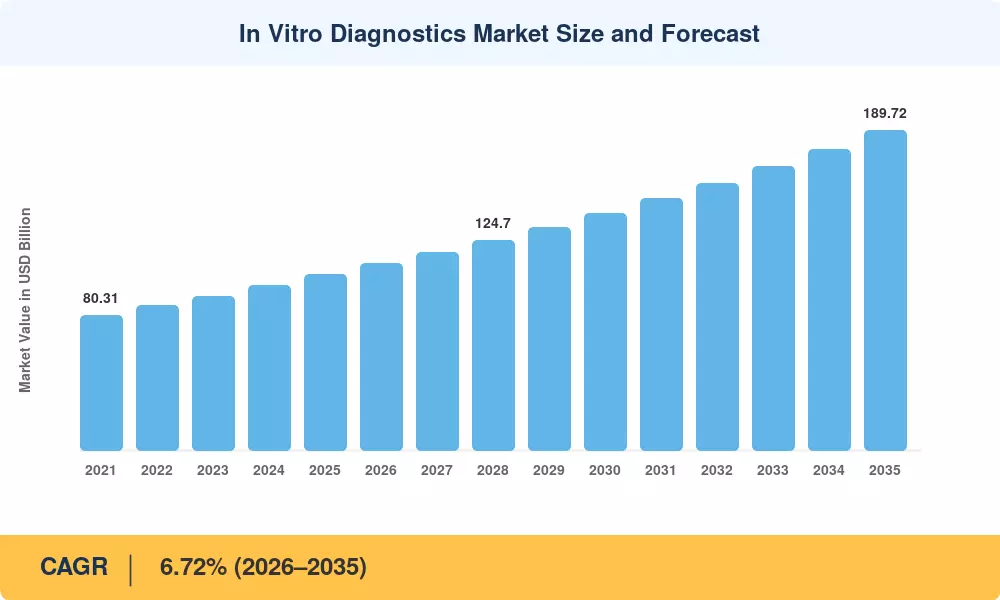

The In Vitro Diagnostics Market reached an estimated USD 104.18 billion in 2025 and is projected to grow from USD 110.94 billion in 2026 to USD 189.72 billion by 2035, registering a CAGR of 6.72% across the forecast period. Two forces anchor this trajectory: the global rise in chronic disease burden — diabetes, cardiovascular conditions, and cancer collectively account for over 70% of healthcare expenditure in OECD nations [2] — and government mandates accelerating laboratory diagnostic testing capacity in lower-income settings, including WHO's 2024 Essential Diagnostics List expansion [3].

A technology change is reshaping clinical laboratory procedures. Fully integrated automation lines with cloud-based middleware are replacing legacy manual analyzers and information systems in silos. In the US and EU, major health systems have invested more than USD 4.5 billion in laboratory consolidation initiatives that combine reagent rental contracts with decision-support software, shortening blood sample analysis turnaround times by up to 35% [4]. PCR-based diagnostic tests and next-generation sequencing panels are replacing earlier culture-based approaches for the detection of infectious diseases, shortening time-to-result from days to hours.

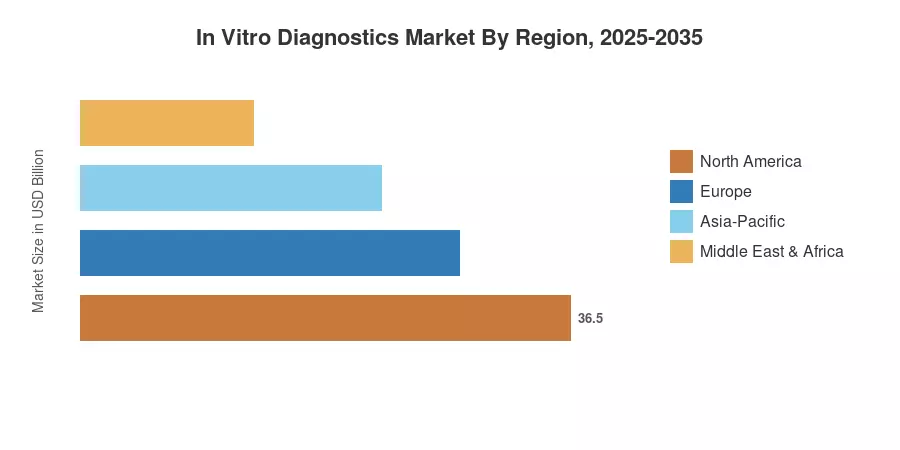

North America accounts for over 34.2% of the global revenue, due to the robust reimbursement policies and the established installed base of clinical immunoassay kits. Asia-Pacific is the fastest expanding market with an estimated CAGR of 7.82% due to hospital infrastructure build-outs in China and India. Europe is the second-largest market with a share of approximately 27.8% based on EU IVDR implementation timetables that are changing competitive dynamics until 2035

Key Report Takeaways

• By Product Type

- Reagents and kits captured approximately 50.4% of the In Vitro Diagnostics Market revenue in 2025, reflecting the recurring consumable demand model that underpins laboratory diagnostic testing economics

- Software and services represent the fastest-expanding product category, projected at a 9.48% CAGR through 2035 as laboratories invest in AI-driven analytics and middleware integration

• By Technology

- Immunoassay platforms led with a 24.7% revenue share in 2025, anchored by high-throughput clinical immunoassay kits deployed across hospital core laboratories

- Molecular diagnostics are forecast to grow at a 7.58% CAGR, driven by expanding adoption of PCR-based diagnostic tests and companion diagnostics in oncology

• By Application

- Infectious diseases represented the largest application segment in the In Vitro Diagnostics Market, generating approximately USD 43.8 billion in 2025

- Oncology testing is positioned as the fastest-growing application at a 9.14% CAGR, underpinned by liquid biopsy innovations and targeted therapy biomarker assays

• By Geography

- North America generated roughly USD 35.6 billion in 2025, with the US alone contributing over 82% of regional revenue

- Asia-Pacific is forecast to register a 7.82% CAGR, making it the primary growth engine for point-of-care diagnostic devices and decentralized testing networks

Market Size and Forecast (2021–2035)

MRFR's sizing framework triangulates bottom-up revenue estimates from reagent shipment data, installed instrument bases, and test-volume metrics reported by national laboratory associations. Top-down validation draws on healthcare expenditure ratios published by the WHO and OECD health accounts[2].

.webp?v=1785508907)