Managed Print Services Market Summary

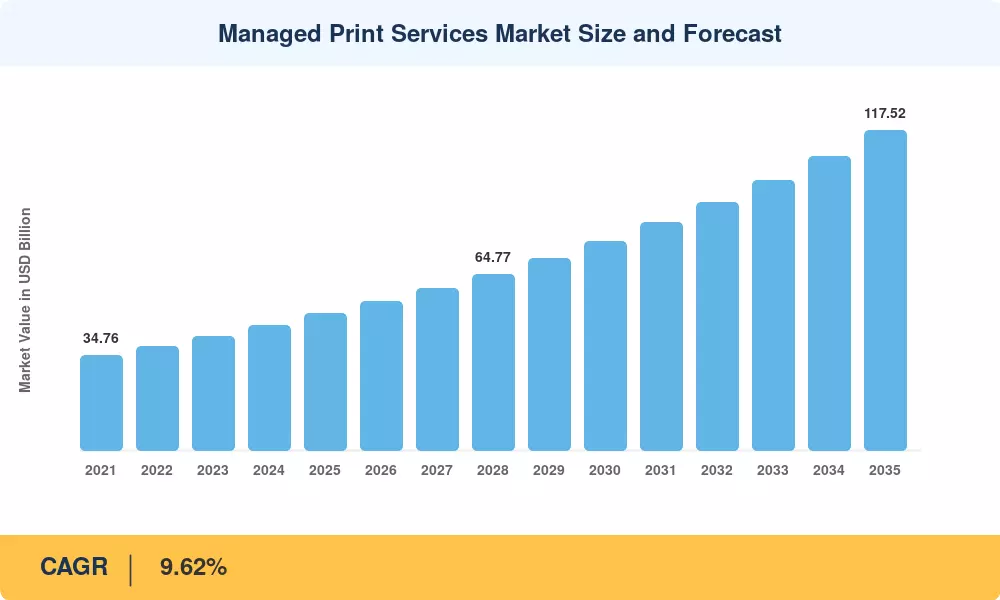

The Managed Print Services Market reached an estimated USD 50.18 billion in 2025 and is projected to grow from USD 54.95 billion in 2026 to USD 117.52 billion by 2035, registering a CAGR of 9.62% during the forecast period. Two catalysts are accelerating this trajectory: enterprise compliance mandates — particularly GDPR Article 30 recordkeeping requirements for printed documents — and the global shift toward hybrid work models that demand secure, cloud-orchestrated printing from any device, anywhere. Corporate IT budgets allocated to outsourced print management rose 14% year-over-year in 2024, reflecting a decisive pivot away from break-fix device ownership toward subscription-based print cost optimization [2].

Legacy on-premise print servers, once the backbone of enterprise printer fleet management, are being replaced by cloud-native MPS platforms that bundle predictive maintenance, zero-trust authentication, and automated supply replenishment.According to a recent report, 62% of new managed document services contracts signed in 2024 included embedded analytics modules, up from 41% two years prior. This transformation is turning print infrastructure from a cost center into a data asset — organizations now extract workflow intelligence from print telemetry to streamline document-intensive processes across legal, healthcare, and financial verticals.

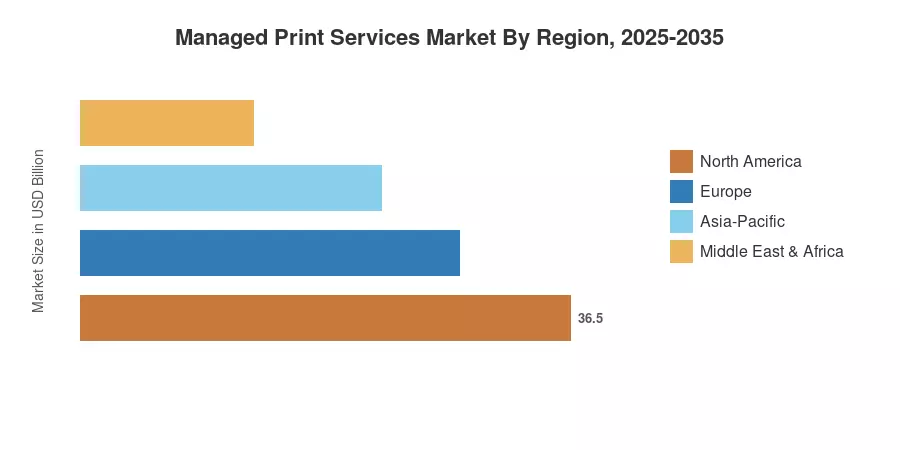

North America commands approximately 43.64% of the global Managed Print Services Market revenue, anchored by early adoption of cloud print architectures and stringent data-handling regulations such as HIPAA and SOX [4]. Asia-Pacific is the fastest-growing region, posting a projected 11.32% CAGR through 2035 as digitization programs in India, China, and Southeast Asia drive first-time MPS adoption among mid-market enterprises. Europe holds the second-largest share at roughly 27%, powered by EU sustainability mandates that reward page-level emissions tracking and carbon-neutral print operations [5]. The decade ahead will see the Managed Print Services Market evolve from fleet optimization into a broader platform play — integrating document workflow automation, AI-driven content routing, and usage-based provisioning at enterprise scale.

Key Report Takeaways

• By Channel Type

- Printer and copier manufacturers captured 52.46% of channel revenue in 2025, yet independent software vendors are disrupting traditional OEM-centric value chains with modular MPS document solutions

• By Service Type

- Cloud print services represent the fastest-growing service category at a 10.01% CAGR through 2035, outpacing managed print operations and print infrastructure assessment segments in the Managed Print Services Market

• By Deployment Mode

- Cloud-based deployment accounted for USD 36.67 billion of the Managed Print Services Market in 2025, reflecting the dominance of SaaS-first enterprise printer fleet management platforms

• By Organization Size

- Small and medium enterprises are forecast to expand at a 10.34% CAGR as affordable, subscription-based outsourced print management models lower adoption barriers

• By Region

- North America leads the Managed Print Services Market with over 43% of 2025 global revenue, driven by mature IT procurement cycles and regulatory-driven print cost optimization

- Asia-Pacific is projected to grow at 11.32% CAGR through 2035, with India and China accounting for the bulk of incremental managed document services demand

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing combines top-down revenue analysis of publicly reporting MPS providers with bottom-up device-fleet and contract-value modeling across 42 countries. Historical figures (2021–2024) are benchmarked against vendor annual reports and Quocirca's print management tracking surveys, while forecast values (2026–2035) are extrapolated using the calibrated 9.62% CAGR.

.webp?v=1785866958)