Micro Mobile Data Center Market Summary

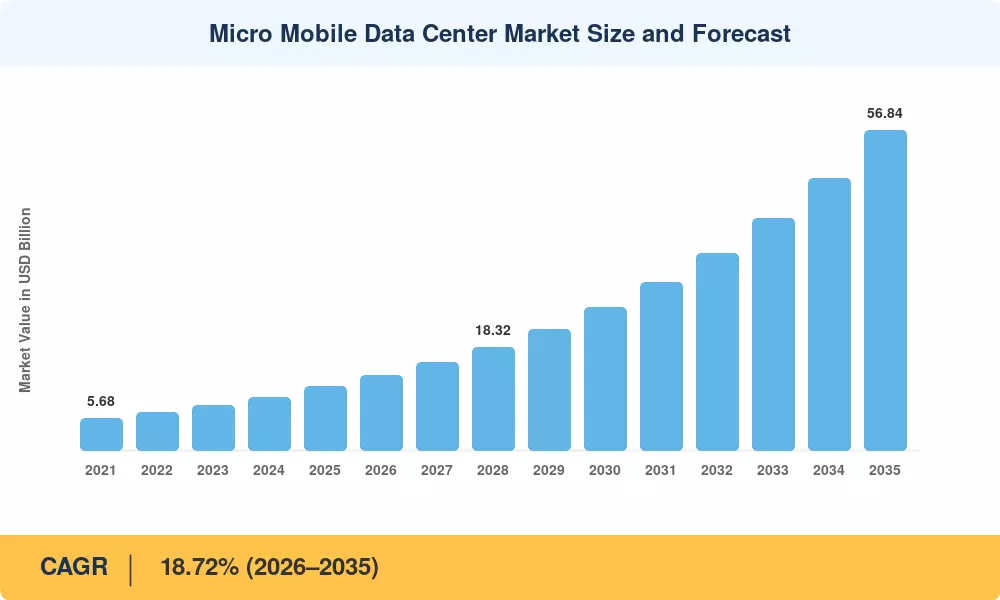

The Micro Mobile Data Center Market reached an estimated USD 11.28 billion in 2025 and is projected to climb from USD 13.22 Billion in 2026 to USD 56.84 billion by 2035, registering an 18.72% CAGR across the forecast window. This trajectory reflects a structural shift in enterprise IT spending—organizations are deploying compact server infrastructure at the network periphery rather than routing every byte back to centralized facilities. Catalysts include the U.S. CHIPS and Science Act's USD 52.7 billion semiconductor investment package and the EU's Digital Decade program, both of which earmark funds for distributed compute capacity[2].

Legacy hub-and-spoke architectures, where traffic is funneled through a handful of mega data centers, are giving way to modular micro data centers that slot into telecom base stations, factory floors, and hospital basements. Edge computing micro DC deployments allow real-time inference for autonomous vehicles, remote surgery, and predictive-maintenance algorithms—workloads that tolerate no more than single-digit millisecond latency. BloombergNEF pegged global edge infrastructure investment at USD 39 Billion in 2024, a figure expected to double by 2028 as 5G standalone networks mature [3].

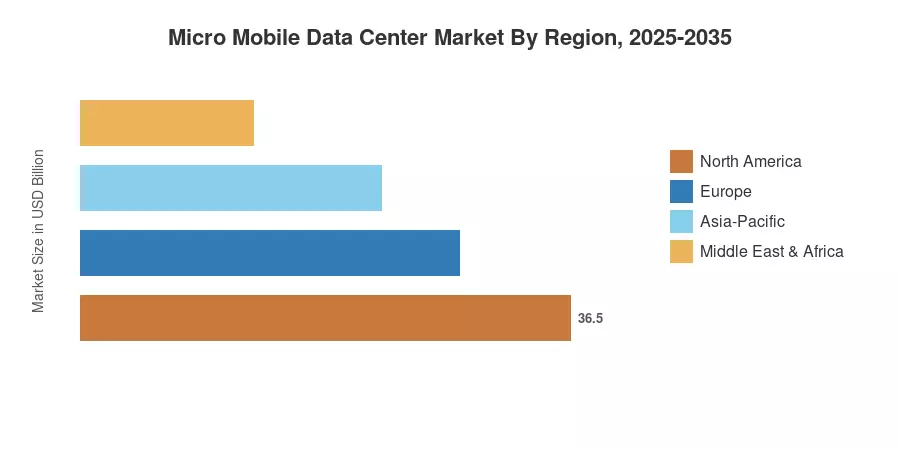

North America commands roughly 37.10% of the Micro Mobile Data Center Market, anchored by hyperscaler edge programs from AWS, Microsoft, and Google. Asia-Pacific is the fastest-growing region at a 19.65% CAGR, propelled by India's Digital India initiative and China's "East Data West Computing" program. Europe holds the second-largest share at approximately 24.80%, driven by GDPR-era data-sovereignty mandates that push processing closer to the point of collection The next decade will see portable data center units become as routine in enterprise IT as server racks were in the 2000s.

Key Report Takeaways

• By Rack Unit Size

- The 25–40 RU segment captured 42.30% of the Micro Mobile Data Center Market in 2025, driven by the sweet spot between density and mobility

• By Form Factor

- Containerized modules are projected to register a 21.15% CAGR through 2035, the fastest among all form factors, as containerized computing units gain traction in harsh-environment deployments

- Rack-mounted pods accounted for USD 5.85 billion in revenue in 2025, reflecting strong demand from telecom operators expanding edge computing micro DC footprints

• By Application

- Edge computing nodes represented 45.10% of the Micro Mobile Data Center Market in 2025, underscoring the primacy of latency-sensitive workloads

• By Organization Size

- SMEs are expanding at a 23.05% CAGR, outpacing large enterprises as edge-as-a-service models lower entry barriers for modular micro data centers

• By Region

- North America generated USD 4.19 billion in 2025 Micro Mobile Data Center Market revenue, led by U.S. hyperscaler edge investments

- Asia-Pacific will post the highest regional CAGR at 19.65%, fueled by smart-city rollouts and 5G densification across India, China, and ASEAN

Market Size and Forecast (2021–2035)

MARKET RESEARCH FUTURE (MRFR)'s estimates blend primary surveys of 280+ IT procurement decision-makers with secondary data from vendor filings and regulatory databases. Historical figures (2021–2024) are actuals; 2025 is a validated base-year estimate; 2026–2035 values apply a calibrated 18.72% CAGR with year-specific adjustments for policy milestones and capex cycles.