Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

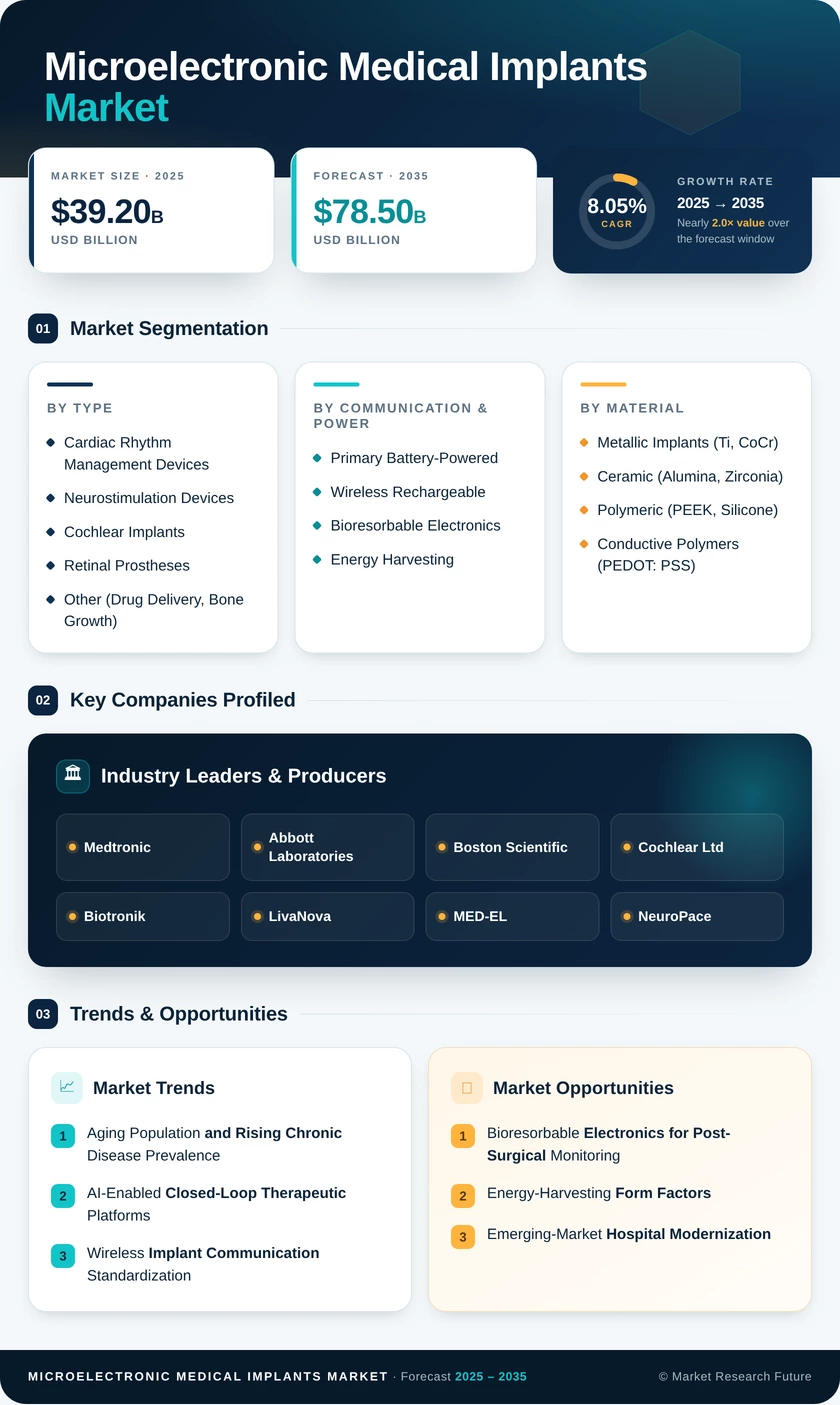

| Product Type | Cardiac Rhythm Management Devices, Neurostimulation Devices, Cochlear Implants, Retinal Prostheses, Other | Cardiac Rhythm Management Devices | Neurostimulation Devices |

| Communication & Power | Primary Battery-Powered, Wireless Rechargeable, Bioresorbable Electronics, Energy Harvesting | Primary Battery-Powered | Bioresorbable Electronics |

| Material | Metallic Implants, Ceramic, Polymeric, Conductive Polymers | Metallic Implants | Conductive Polymers |

| End User | Hospitals, Ambulatory Surgery Centers, Home Care Settings, Specialty Clinics | Hospitals | Home Care Settings |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Cardiac Rhythm Management Devices | Transition from transvenous to leadless pacemaker platforms with integrated implantable biosensor chip modules |

| Neurostimulation Devices | Closed-loop deep brain stimulation using adaptive neural electrode arrays and onboard AI inference |

| Cochlear Implants | Rising bilateral implantation rates in pediatric populations; market consolidation post-Oticon acquisition |

| Retinal Prostheses | Cortical vision prosthesis development combining miniaturized medical electronics with gene-therapy adjuncts |

| Other (Drug Delivery, Bone Growth) | MEMS-actuated drug-delivery pumps for intrathecal pain management and oncology applications |

The product-type dimension reflects the Microelectronic Medical Implants Market's evolution from single-function therapeutic devices toward multi-sensor, software-defined platforms. Cardiac rhythm management remains the volume anchor, but the fastest revenue growth concentrates in neurostimulation and retinal prostheses, where clinical unmet need is high, and reimbursement pathways are expanding.

By Communication & Power

| Sub-Segment | Key Trend |

| Primary Battery-Powered | Lithium-carbon-fluoride cathodes extending device lifespans beyond 15 years |

| Wireless Rechargeable | Inductive and resonant wireless implant communication for neurostimulator recharging at home |

| Bioresorbable Electronics | Transient silicon-nanomembrane sensors for post-surgical monitoring that dissolve within weeks |

| Energy Harvesting | Piezoelectric and thermoelectric modules scavenging body energy for indefinite implant operation |

Power architecture is a defining competitive axis: manufacturers that master energy harvesting and bioresorbable form factors can bypass the replacement-surgery cycle entirely, reshaping the lifetime cost equation and competitive positioning within the Microelectronic Medical Implants Market.

By Material

| Sub-Segment | Key Trend |

| Metallic Implants (Ti, CoCr) | Established structural platform; incremental innovation in nano-textured surface coatings |

| Ceramic (Alumina, Zirconia) | Hermetic encapsulation for MEMS biomedical devices requiring long-term implant integrity |

| Polymeric (PEEK, Silicone) | Flexible substrates enabling conformal neural interfaces and body-contour device housings |

| Conductive Polymers (PEDOT: PSS) | Low-impedance electrode coatings dramatically improve signal fidelity in neural electrode arrays |

Material selection dictates device biocompatibility, longevity, and signal quality. Conductive polymers are the fastest-growing material subsegment, driven by their superior electrochemical properties for miniaturized medical electronics used in brain-computer interfaces.

By End User

| Sub-Segment | Key Trend |

| Hospitals | Primary implantation site; catheterization and electrophysiology lab infrastructure |

| Ambulatory Surgery Centers | Growing share of outpatient neurostimulator and leadless pacemaker implants |

| Home Care Settings | Remote monitoring of implantable biosensor chip devices via wireless implant communication hubs |

| Specialty Clinics | Audiology and chronic-pain management clinics are driving cochlear and SCS device adoption |

Hospital dominance persists due to surgical infrastructure requirements, but the fastest growth is migrating toward home care settings where remote-monitoring platforms extend the clinical reach of implant-based therapies and reduce readmission rates.