Microelectronic Medical Implants Market Summary

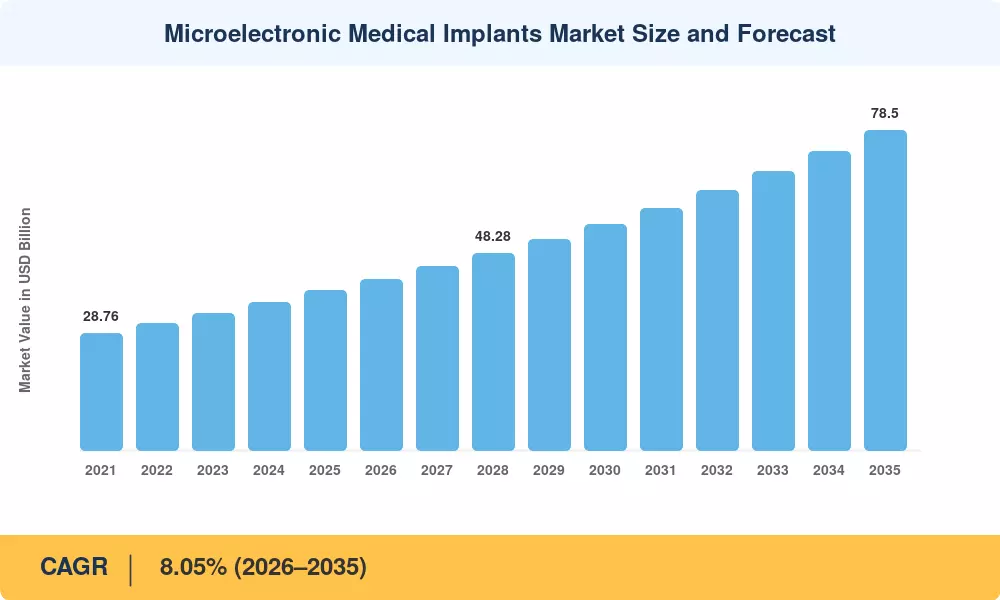

The Global Microelectronic Medical Implants Market size was valued at USD 39.20 Billion in 2025, and the market is projected to grow from USD 42.35 Billion in 2026 to USD 78.50 Billion by 2035, registering a CAGR of 8.05% during the forecast period 2026–2035. Two structural catalysts anchor this trajectory: the U.S. FDA's 2024 expanded De Novo pathway for AI-adaptive implantable biosensor chip platforms [2], and the European Commission's EUR 1.8 Billion Horizon Europe allocation for next-generation miniaturized medical electronics through 2027 [3]. Together, these policy vectors channel public and private capital toward closed-loop therapeutic devices that adapt in real time to patient physiology.

A generational technology shift is underway. Legacy pacemakers and fixed-rate neurostimulators built on discrete-component architectures are giving way to system-on-chip implants integrating neural electrode arrays, wireless implant communication modules, and onboard machine-learning inference engines. Medtronic's 2024 annual report disclosed USD 2.1 billion in R&D spending on MEMS biomedical devices and algorithm-driven therapy platforms, reflecting the industry's pivot from hardware-centric design to software-defined implant ecosystems [4]. Conductive polymer substrates and bioresorbable sensor packages promise to eliminate secondary extraction surgeries entirely within the coming decade.

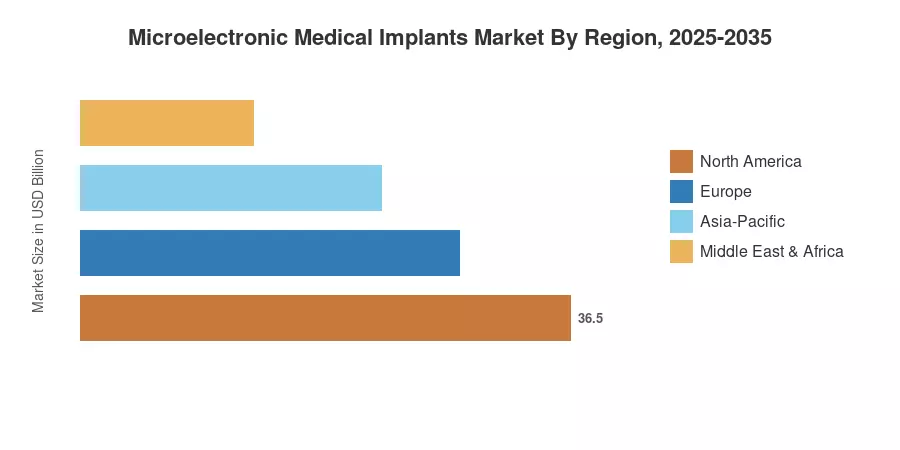

North America commands roughly 42% of the Microelectronic Medical Implants Market, driven by Medicare reimbursement expansions and a dense clinical-trial infrastructure Asia-Pacific records the fastest compounded gains at a projected 10.4% CAGR, as China and India modernize tertiary hospitals and chronic cardiovascular disease prevalence climbs [5]. Europe holds the second-largest share, near 27%, anchored by Germany's medtech manufacturing corridor and the EU MDR compliance wave reshaping competitive dynamics. The Microelectronic Medical Implants Market is positioned for sustained double-digit segment-level growth in neurostimulation and bioresorbable electronics through 2035.

Key Report Takeaways

• By Product Type

- Cardiac rhythm management devices accounted for 49.2% of the Microelectronic Medical Implants Market in 2024, reinforced by remote-monitoring mandates across U.S. and EU payer systems

- Neurostimulation devices are expanding at a 12.3% CAGR through 2035, fueled by FDA breakthrough designations for closed-loop deep brain stimulation platforms

- Cochlear implants contributed approximately USD 4.80 billion in 2024 revenue, with bilateral implantation rates rising in pediatric populations

• By Communication & Power

- Primary battery-powered systems held 79.1% of the Microelectronic Medical Implants Market size in 2024, although next-generation lithium-carbon-fluoride chemistries are extending device longevity beyond 15 years

- Bioresorbable electronics are forecast to surge at a 21.8% CAGR to 2035, eliminating extraction procedures for temporary monitoring applications

• By Region

- North America led with a 42.0% revenue share in 2024, supported by robust wireless implant communication reimbursement codes

- Asia-Pacific is projected to grow at a 10.4% CAGR, with China's 14th Five-Year Plan earmarking CNY 45 billion for domestic implantable biosensor chip manufacturing capacity

Microelectronic Medical Implants Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s proprietary sizing model synthesizes bottom-up revenue analysis from device manufacturer filings, top-down macro indicators (aging demographics, chronic disease prevalence, surgical volume databases), and triangulation against peer estimates. Historical figures derive from audited company revenues and customs-trade data; forecast values apply the calibrated 8.05% CAGR with adjustments for regulatory cycle timing and technology adoption curves.