Mobility as a Service Market Summary

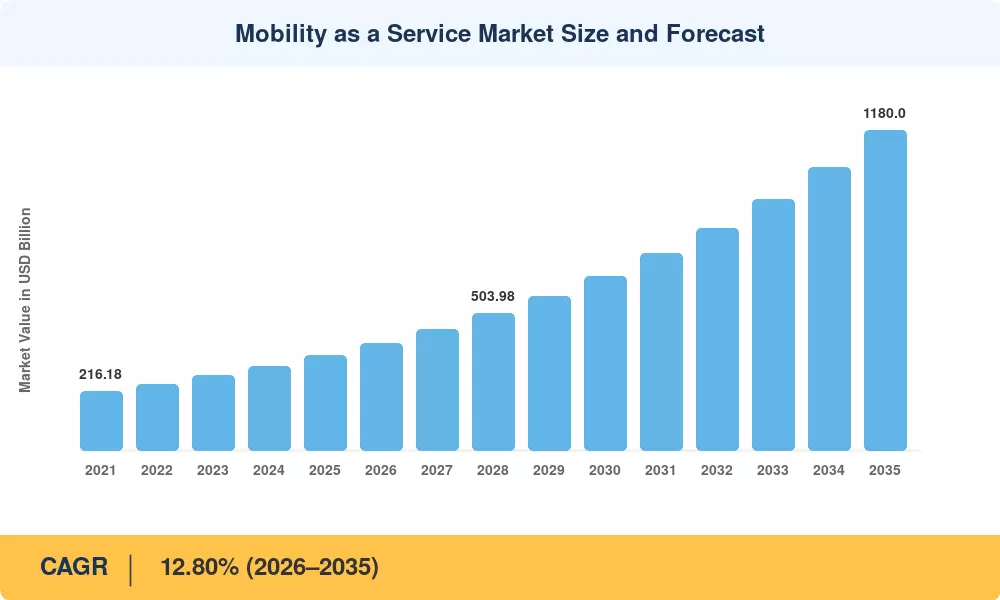

The Mobility as a Service Market reached an estimated USD 350.00 Billion in 2025 and is projected to grow from USD 399.00 Billion in 2026 to USD 1,180.00 Billion by 2035, registering a CAGR of 12.80% during 2026–2035. This acceleration is anchored in aggressive municipal zero-emission mandates across the EU and North America, coupled with over USD 48 billion in cumulative venture capital deployed into on-demand mobility platforms since 2021[2]. Governments are tying federal transit grants to integrated transport solutions that unify ticketing, routing, and payment into single-app ecosystems, creating a strong policy tailwind for platform providers.

A sweeping technology transformation underpins this trajectory. Legacy siloed transit systems — separate ticketing for rail, bus, and ride-hail — are giving way to unified smart transportation apps that orchestrate multimodal journeys through a single interface. The European Commission's 2024 Sustainable Urban Mobility Framework earmarked EUR 12 billion toward interoperable shared mobility technology infrastructure across 27 member states, while the U.S. DOT allocated USD 3.2 billion under the Bipartisan Infrastructure Law for urban mobility services pilots in 45 metropolitan areas [3][4].

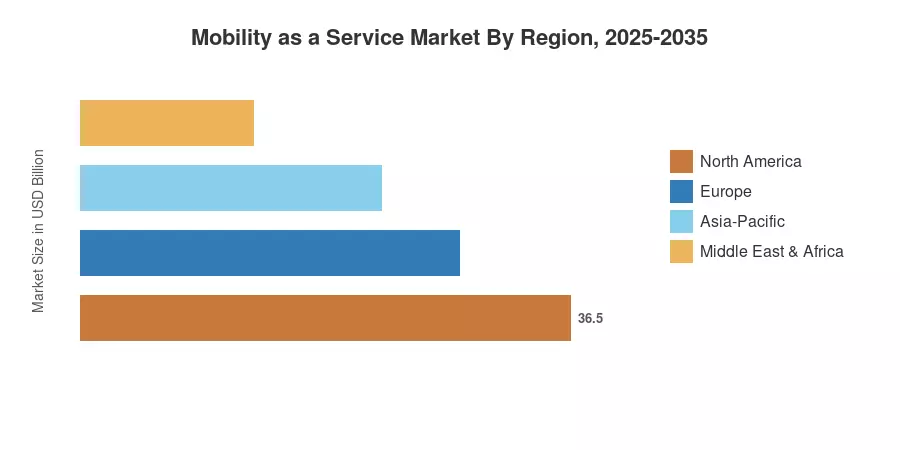

North America commands roughly 34% of the global Mobility as a Service Market, driven by mature ride-hailing ecosystems and high smartphone penetration. Asia-Pacific is the fastest-growing region at an estimated 15.20% CAGR, propelled by India's and China's rapid urbanization and government-backed digital transit rollouts. Europe holds the second-largest share at approximately 28%, with Nordic countries serving as global benchmarks for subscription-based urban mobility services The decade ahead will see autonomous vehicle integration and AI-powered journey orchestration reshape competitive dynamics fundamentally.

Key Report Takeaways

• By Service Type

- Ride-hailing captured approximately 48.7% of the Mobility as a Service Market revenue in 2025, reflecting deep consumer penetration of on-demand mobility platforms in urban centers

- Micro-mobility services are forecast to expand at a 20.5% CAGR through 2035, the fastest among all service categories, driven by last-mile connectivity needs and smart transportation apps for e-scooters and bikes

• By Solution

- Technology platform solutions held an estimated 40.2% share in 2025, underscoring demand for integrated transport solutions that unify routing, booking, and analytics

- Payment and wallet services are anticipated to grow at a 22.5% CAGR, fueled by contactless and tokenized fare collection across shared mobility technology networks

• By Region

- North America led the Mobility as a Service Market with approximately USD 119.00 Billion in 2025 revenue

- Asia-Pacific is set to register the highest regional CAGR at 15.20%, underpinned by smart city programs and urban mobility services expansion in China and India

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s sizing model integrates bottom-up revenue analysis from platform operators, transit agencies, and fleet management providers with top-down macroeconomic indicators, including urbanization rates, smartphone penetration, and per-capita transport expenditure. Historical data (2021–2024) relies on audited company filings and government transport statistics; the forecast (2026–2035) applies a calibrated CAGR verified against multiple third-party benchmarks[5].

.webp?v=1784551656)