Municipal Solid Waste Management Market Summary

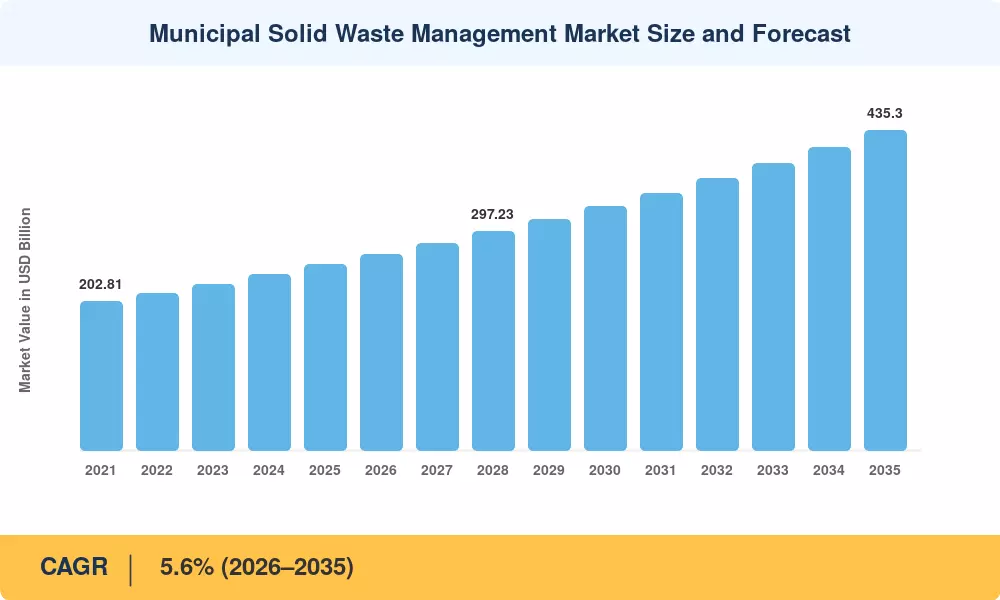

The Municipal Solid Waste Management Market reached an estimated USD 252.4 billion in 2025 and is projected to grow from USD 266.5 billion in 2026 to USD 435.3 billion by 2035, registering a CAGR of 5.6% during the forecast period (2026–2035). Two catalysts anchor this trajectory: China's "zero-waste city" pilot program—now spanning 113 cities with an aggregate investment exceeding USD 14 billion [1]—and the European Union's binding target to recycle 65% of municipal waste by 2035 under Directive 2018/851 [2]. These policy mandates have transformed what was once a basic municipal utility into a capital-intensive, technology-driven industry.

Legacy open-dump and uncontrolled landfill systems are rapidly being replaced by engineered treatment chains integrating mechanical-biological processing, sophisticated heat recovery and sensor-driven collection logistics. The World Bank projects that worldwide garbage generation would jump to 3.4 billion tonnes per year in 2050 from 2.01 billion in 2016 [3], pushing communities to invest in scalable infrastructure today. Private-sector participation in terms of build-operate-transfer (BOT) concessions exceeded USD 9.2 billion in new contract value in 2024 alone [4].

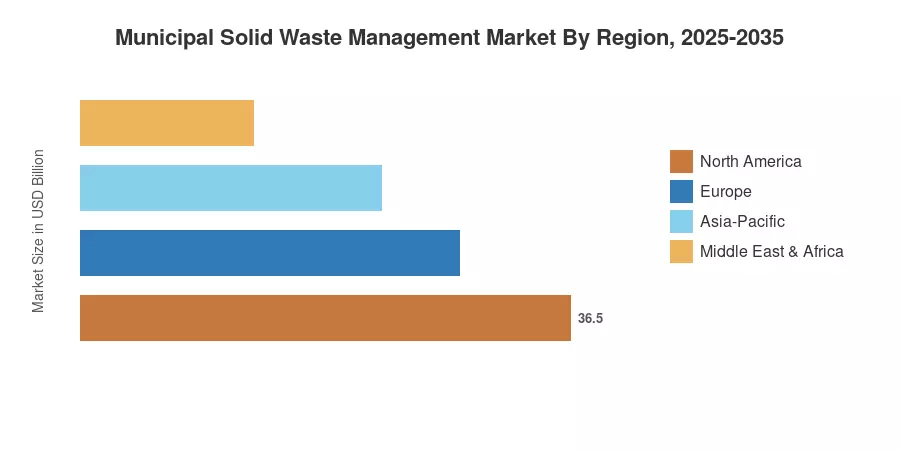

Asia-Pacific leads the Municipal Solid Waste Management Market with around 38% of the worldwide revenue, due to the high rates of urbanization, which are greater than 2.3% each year in India and Southeast Asia. This region also accounts for the fastest expanding opportunity with a projected CAGR of 6.9%. North America is the second largest, with about 27%, supported by strict EPA subtitle D restrictions and a developed recycling infrastructure [5]. Circular-economy mandates drive Europe’s share of about 23%. The Municipal Solid Waste Management Market will structurally continue to grow through 2035 as landfill prohibitions increase and carbon pricing mechanisms tighten.

Key Report Takeaways

• By Treatment Method

- Landfill operations account for the largest revenue share at approximately 41% of the Municipal Solid Waste Management Market, though regulatory pressure is steadily contracting new capacity additions.

- Recycling and material-recovery operations are growing at the fastest segment CAGR of 7.1%, fueled by extended producer responsibility (EPR) legislation across 48 countries.

- Thermal treatment (incineration and energy recovery) generated roughly USD 52.6 billion in 2025, reflecting rising adoption in land-scarce economies.

• By Waste Type

- Organic waste constitutes approximately 44% of total MSW volume globally and commands the highest treatment expenditure within the Municipal Solid Waste Management Market.

- Plastic waste segments are posting a CAGR of 6.8%, driven by chemical recycling investment and single-use plastic bans.

• By Region

- Asia-Pacific leads the Municipal Solid Waste Management Market at 38% share, with China and India contributing over 60% of regional revenue.

- The Middle East & Africa region is expected to grow at a CAGR of 7.3%, the highest among non-APAC regions, as Gulf states invest in modern waste infrastructure.

- North America's market value is projected to reach approximately USD 112.8 billion by 2035, supported by federal infrastructure grants.

Municipal Solid Waste Management Market Size and Forecast (2021–2035)

Market-sizing combines bottom-up revenue summation from municipal contract databases, waste authority filings, and publicly stated operating revenue of prominent operators. Top-down validation cross-links World Bank, OECD and UNEP waste-generation figures with per-tonne treatment cost benchmarks to derive regional and worldwide revenue projections for the Municipal Solid Waste Management Market.