Neurorehabilitation Devices Market Summary

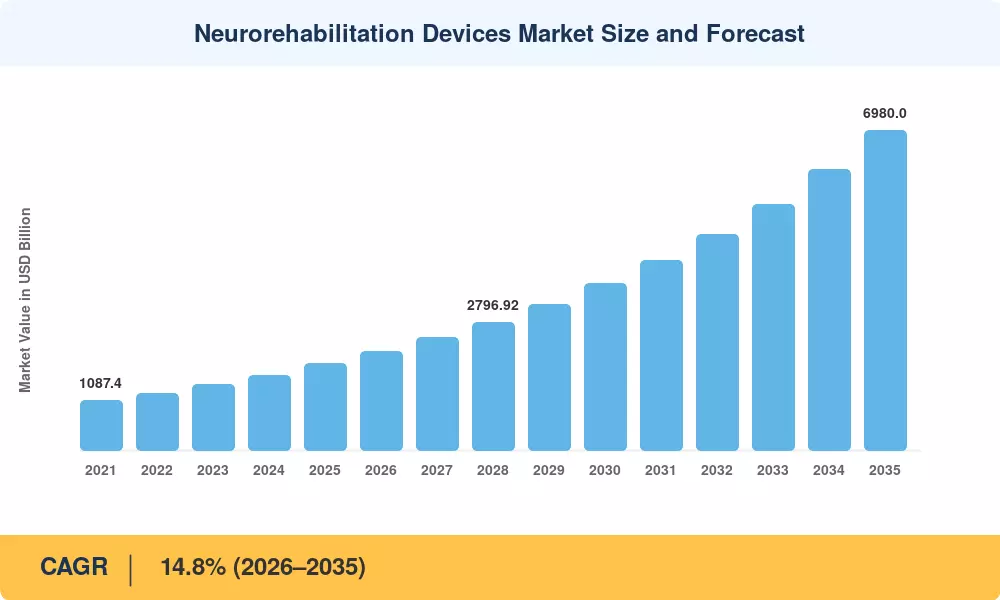

The Neurorehabilitation Devices Market reached an estimated USD 1,890 million in 2025 and is projected to grow from USD 2,170 million in 2026 to approximately USD 6,980 million by 2035, registering a CAGR of 14.8% over the forecast period (2026–2035). This acceleration is anchored to two converging forces: the global surge in neurological disorder prevalence — with over 55 million people now living with dementia alone [2] — and aggressive government investment in brain injury recovery tools through programs like the U.S. BRAIN Initiative, which has channeled more than USD 3.2 billion into neuroscience research since inception [3].

A decisive technology transformation is reshaping the landscape. Legacy manual therapy protocols and passive rehabilitation equipment are giving way to robotic-assisted neuro therapy platforms, closed-loop brain-computer interfaces, and AI-driven cognitive rehabilitation technology. The FDA's 2021 clearance of the IpsiHand System — a brain-computer interface for stroke rehabilitation equipment — signaled a regulatory inflection point, and investment in neural plasticity therapy devices has since surged past USD 780 million annually across venture and strategic channels [4]. Hospital systems are actively replacing static exercise stations with sensor-equipped neuro-robotic systems that capture real-time patient neuroplasticity data.

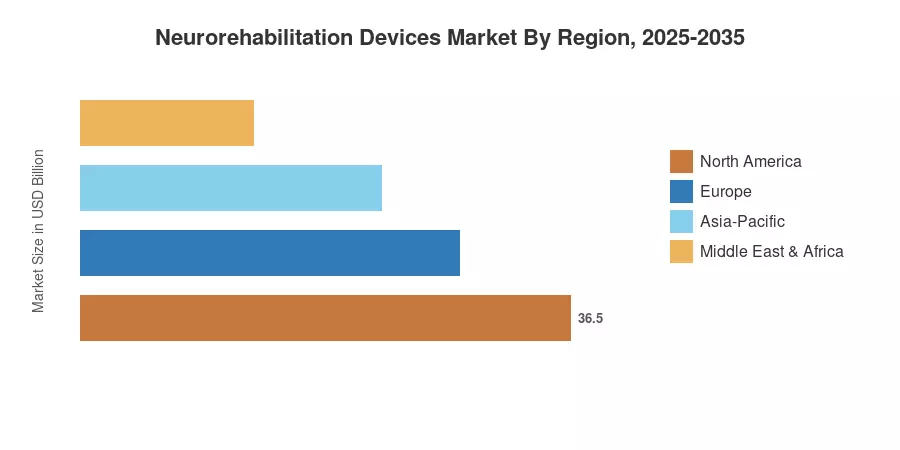

North America dominates the Neurorehabilitation Devices Market with roughly 38% revenue share, driven by advanced hospital infrastructure and favorable reimbursement frameworks. Asia-Pacific stands as the fastest-growing region at a projected CAGR exceeding 16.5%, propelled by expanding healthcare access in China and India. Europe holds the second-largest share at approximately 29%, with Germany and the UK leading adoption of stroke rehabilitation equipment in public health networks The decade ahead promises further disruption as telerehabilitation and AI-personalized therapy protocols redefine care delivery worldwide.

Key Report Takeaways

• By Product Type

- Neuro-robotic devices command roughly 35% of the Neurorehabilitation Devices Market, driven by growing demand for robotic-assisted neuro therapy in post-stroke recovery settings

- Brain-computer interfaces represent the fastest-growing segment at an estimated CAGR of 18.2%, fueled by regulatory clearances and expanding clinical evidence for neural plasticity therapy devices

- Non-invasive stimulators account for approximately USD 420 million in 2025 revenue, underpinned by outpatient adoption and insurance coverage expansion

• By End User

- Hospitals and clinics generate the largest end-user share in the Neurorehabilitation Devices Market at roughly 52%, reflecting capital equipment procurement cycles and specialist staffing availability

- Cognitive care centers are growing at an estimated CAGR of 16.1%, as dedicated brain injury recovery tools become central to dementia and TBI treatment pathways

• By Region

- North America leads with approximately USD 718 million in 2025 revenue, anchored by Medicare reimbursement codes for cognitive rehabilitation technology

- Asia-Pacific is projected to reach a 24% regional share by 2035, with China and India expanding public neurorehabilitation infrastructure

- Europe captures roughly 29% of global revenue, with Germany alone accounting for a CAGR of 14.3% through 2035

Market Size and Forecast (2021–2035)

The Neurorehabilitation Devices Market size estimates below integrate primary research with hospital procurement databases, regulatory filing analysis, and manufacturer revenue disclosures. Historical figures (2021–2024) are based on validated shipment data; the base year (2025) reflects confirmed purchase orders and installed-base surveys. Forecast values (2026–2035) apply a compound growth model calibrated to clinical adoption curves and reimbursement pipeline analysis.