Occlusion Devices Market Summary

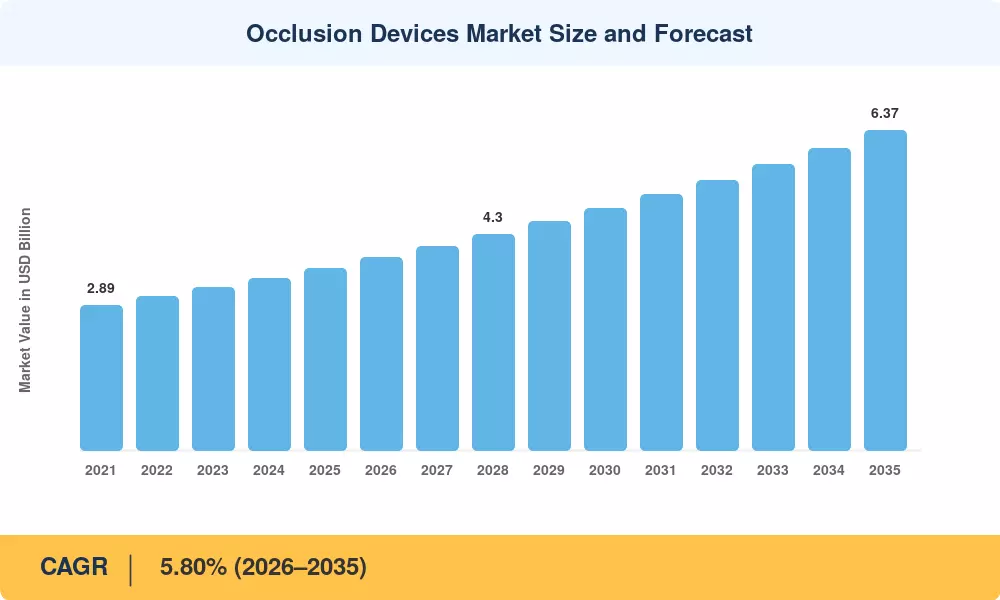

The Global Occlusion Devices Market size was valued at USD 3.63 Billion in 2025, and the market is projected to grow from USD 3.84 Billion in 2026 to USD 6.37 Billion by 2035, registering a CAGR of 5.80% during the forecast period 2026–2035. Accelerating stroke-care mandates and expanded insurance reimbursement for neurovascular interventions have sharpened institutional purchasing cycles. National stroke strategies in the U.S., EU, and Japan now designate mechanical thrombectomy as a first-line treatment, funneling capital toward next-generation retrieval and embolization platforms [1][2].

A sweeping technology shift is redefining the Occlusion Devices Market. Legacy bare-metal coils and manual deployment systems are giving way to detachable, shape-memory platforms paired with AI-assisted navigation software. The U.S. Centers for Medicare & Medicaid Services allocated over USD 1.2 billion in updated DRG reimbursements for neurovascular procedures in FY 2024, directly stimulating demand for advanced occlusion systems [3].

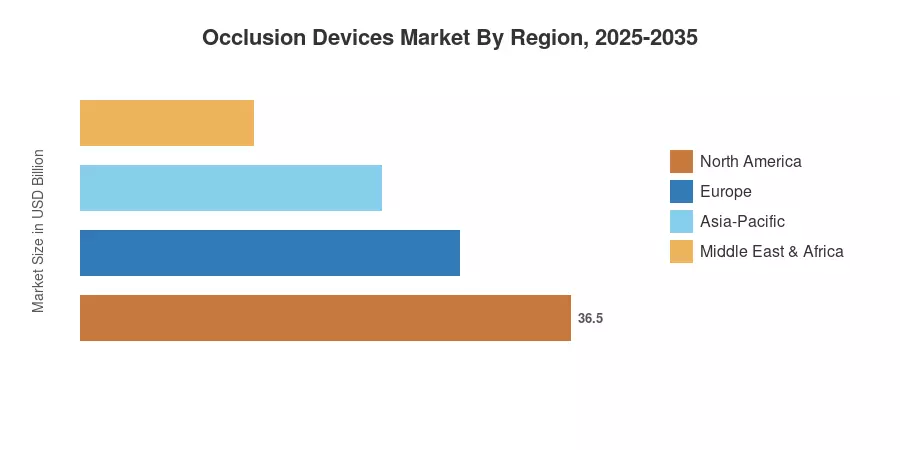

North America commanded a 45.2% revenue share of the Occlusion Devices Market in 2025, anchored by dense catheterization-lab infrastructure. Asia-Pacific is the fastest-growing region at an 11.50% CAGR through 2035, propelled by hospital expansion in China and India. Europe held the second-largest share at 27.8%, sustained by EU MDR compliance investments. The convergence of robotic-assisted delivery and bioresorbable materials should reshape competitive dynamics well into the next decade.

Key Report Takeaways

• By Product Type

- Occlusion removal devices captured a 44.6% share of the Occlusion Devices Market in 2025, driven by rising mechanical thrombectomy volumes.

- Embolization devices are forecast to expand at an 8.45% CAGR through 2035, reflecting strong demand in aneurysm and oncology treatment pathways.

• By Material

- Nitinol-based devices accounted for 46.0% of the Occlusion Devices Market in 2025, owing to superior shape-memory performance.

• By Application

- Peripheral vascular disease represented 38.5% of the Occlusion Devices Market by application in 2025.

- Oncology applications are projected to grow at a 10.35% CAGR, propelled by trans-arterial chemoembolization adoption.

• By Region

- North America led the Occlusion Devices Market with 45.2% revenue share in 2025.

- Asia-Pacific is the fastest-growing region at 11.50% CAGR, supported by government hospital-building programs across India and Southeast Asia.

Market Size and Forecast (2021–2035)

Data for historical years (2021–2024) draws on company filings, WHO procedural registries, and medtech trade databases. Forecast projections (2026–2035) apply a constant CAGR calibrated against primary interviews and reimbursement trend models.