Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

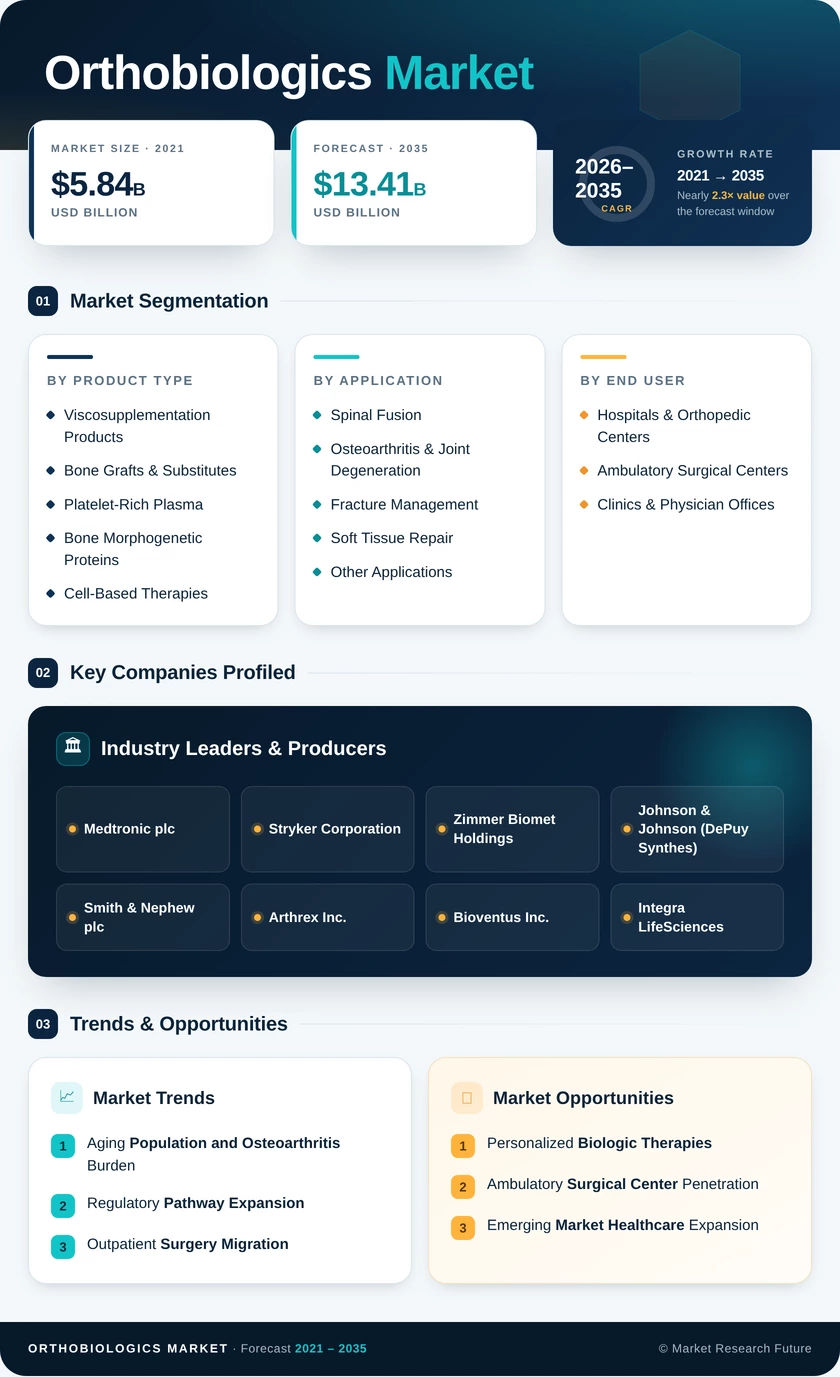

| Product Type | Viscosupplementation Products, Bone Grafts & Substitutes, Platelet-Rich Plasma, Bone Morphogenetic Proteins, Cell-Based Therapies, Other Products | Viscosupplementation Products (46.1%) | Cell-Based Therapies (8.9% CAGR) |

| Application | Spinal Fusion, Osteoarthritis & Joint Degeneration, Fracture Management, Soft Tissue Repair, Other Applications | Spinal Fusion (57.0%) | Osteoarthritis & Joint Degeneration (10.3% CAGR) |

| End User | Hospitals & Orthopedic Centers, Ambulatory Surgical Centers, Clinics & Physician Offices | Hospitals & Orthopedic Centers (67.4%) | Ambulatory Surgical Centers (8.8% CAGR) |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America (46.2%) | Asia-Pacific (12.1% CAGR) |

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Viscosupplementation Products | Single-injection formulations gaining share over multi-injection regimens |

| Bone Grafts & Substitutes | Synthetic ceramics closing performance gap with allografts |

| Platelet-Rich Plasma | Chairside preparation systems expanding ambulatory adoption |

| Bone Morphogenetic Proteins | Next-generation controlled-release carriers improving safety profiles |

| Cell-Based Therapies | Regulatory pathways maturing; commercial launches expected 2028–2030 |

| Other Products | Demineralized bone matrix maintaining stable niche demand |

Viscosupplementation remains the commercial backbone of the product mix, although single-injection products with extended duration claims are shifting competitive dynamics toward fewer, higher-value treatments per patient episode. Platelet-rich plasma preparation technology continues to simplify, lowering the procedural complexity barrier that historically limited PRP to specialized clinics.

By Application

| Sub-Segment | Key Trend |

| Spinal Fusion | Biologics-first approaches replacing autograft harvest in anterior procedures |

| Osteoarthritis & Joint Degeneration | Joint preservation strategies delaying total arthroplasty |

| Fracture Management | Bioactive bone cements and injectable scaffolds gaining traction |

| Soft Tissue Repair | PRP augmentation protocols standardizing across sports medicine |

| Other Applications | Dental and maxillofacial biologics showing steady but moderate growth |

Spinal fusion consumes the highest per-procedure biologic volume of any application, driven by the shift away from iliac crest autograft harvesting toward commercially processed allograft and synthetic alternatives. Osteoarthritis management is the fastest-expanding application as aging demographics and patient preference for non-surgical options align with clinical evidence improvements.

By End User

| Sub-Segment | Key Trend |

| Hospitals & Orthopedic Centers | Volume purchasing agreements consolidating vendor relationships |

| Ambulatory Surgical Centers | Cost-efficiency mandates favoring injectable over implantable biologics |

| Clinics & Physician Offices | Point-of-care PRP systems enabling office-based regenerative treatments |

Hospitals continue to dominate biologic orthopedic product consumption due to the complexity of surgical procedures requiring inpatient infrastructure. Ambulatory surgical centers represent the fastest-growing channel as payer incentives reward outpatient delivery of injectable biologic therapies with lower facility overhead.