Orthobiologics Market Summary

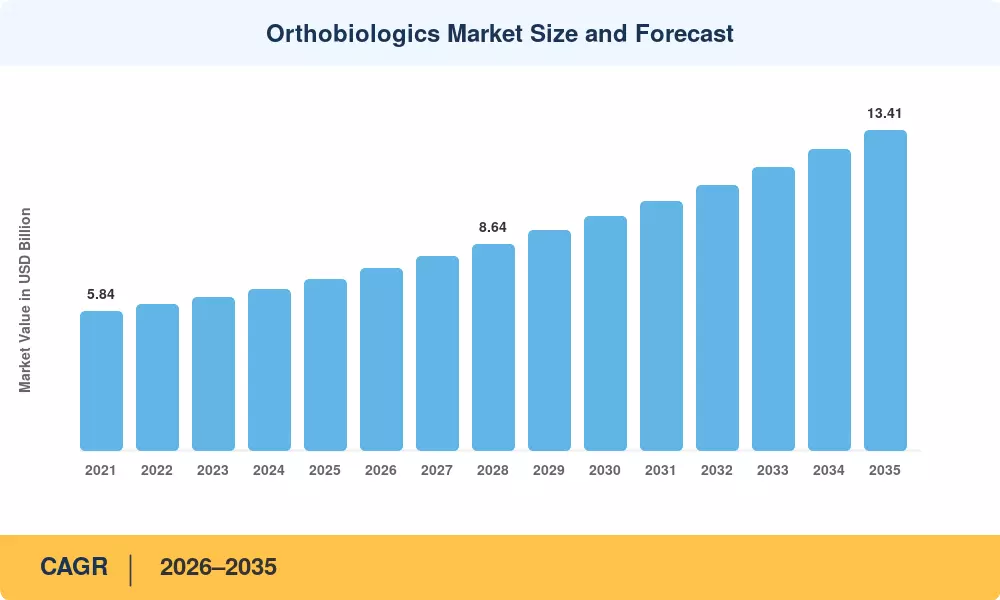

The Orthobiologics Market size was valued at USD 7.15 Billion in 2025, and the market is projected to grow from USD 7.61 Billion in 2026 to USD 13.41 Billion by 2035, registering a CAGR of 6.5% during the forecast period 2026–2035. Accelerating demand traces back to two converging forces: a global osteoarthritis burden that the WHO projects will affect 528 million people by 2030, and a regulatory environment increasingly receptive to regenerative orthopedic therapies [1]. The U.S. FDA cleared 18 new platelet-rich plasma preparation devices through its 510(k) pathway in 2024, signaling a meaningful commercial on-ramp for point-of-care biologic treatments [2].

A broader transformation is reshaping how clinicians manage musculoskeletal tissue repair. Traditional metallic fixation hardware — screws, plates, and cages — is being supplemented and in some indications replaced by biologically active alternatives that recruit the body's own healing cascades. The National Institutes of Health allocated over USD 320 Million to musculoskeletal regenerative research grants in fiscal year 2024, underscoring institutional confidence in biologic approaches [3]. Domestic tissue processors in the United States have also reshored manufacturing capacity to offset tariff-driven cost increases on imported orthopedic hardware [4].

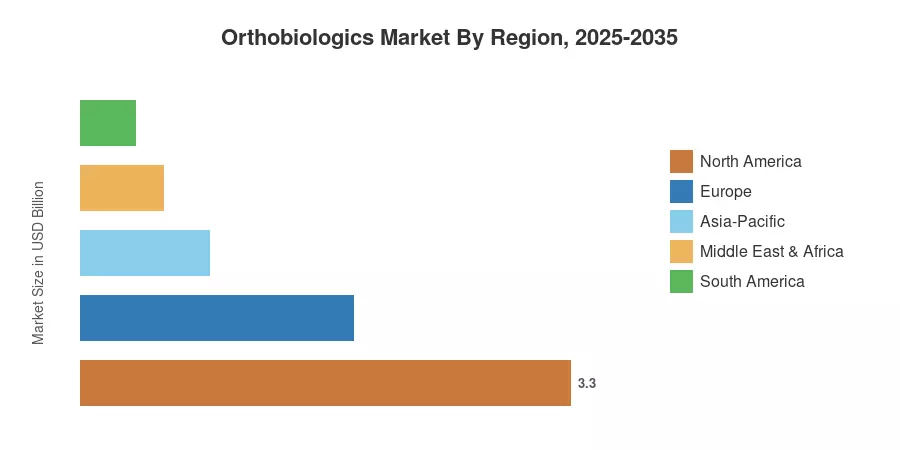

North America commands approximately 46.2% of global Orthobiologics Market revenue, anchored by high procedural volumes and robust payer infrastructure. Asia-Pacific is the fastest-growing region, projected to expand at a 12.1% CAGR to 2035, fueled by rising disposable incomes and healthcare infrastructure buildouts across China and India. Europe holds the second-largest share at roughly 25.8%, driven by aging demographics and strong clinical research ecosystems. Together, these regional dynamics position the Orthobiologics Market for sustained mid-single-digit growth throughout the next decade.

Key Report Takeaways

• By Product Type

- Viscosupplementation products captured 46.1% of the Orthobiologics Market in 2025, led by hyaluronic acid injectable therapies for knee osteoarthritis.

- Platelet-rich plasma is forecast to expand at a 7.6% CAGR through 2035, reflecting growing adoption in sports medicine and outpatient settings.

• By Application

- Spinal fusion accounted for 57.0% of 2025 Orthobiologics Market revenue, driven by the rising incidence of degenerative disc disease in populations aged 50 and older.

- Osteoarthritis and joint degeneration applications are advancing at a 10.3% CAGR to 2035 as non-surgical biologic interventions gain clinical traction.

• By End User

- Hospitals and orthopedic centers controlled 67.4% of Orthobiologics Market revenue in 2025, reflecting centralized surgical workflows and procurement scale.

- Ambulatory surgical centers are growing at an 8.8% CAGR, benefiting from cost-efficiency mandates and shifting payer preferences.

• By Region

- North America captured 46.2% of 2025 global revenue for the Orthobiologics Market, underpinned by commercial payer coverage for viscosupplementation and bone grafting.

- Asia-Pacific is projected to expand at a 12.1% CAGR, the fastest of any region to 2035.

Market Size and Forecast (2021–2035)

Market Research Future derives its sizing estimates from a triangulated approach combining company revenue disclosures, procedural volume databases, and proprietary primary interviews with orthopedic surgeons and procurement specialists across 22 countries.