Osteoarthritis Therapeutics Market Summary

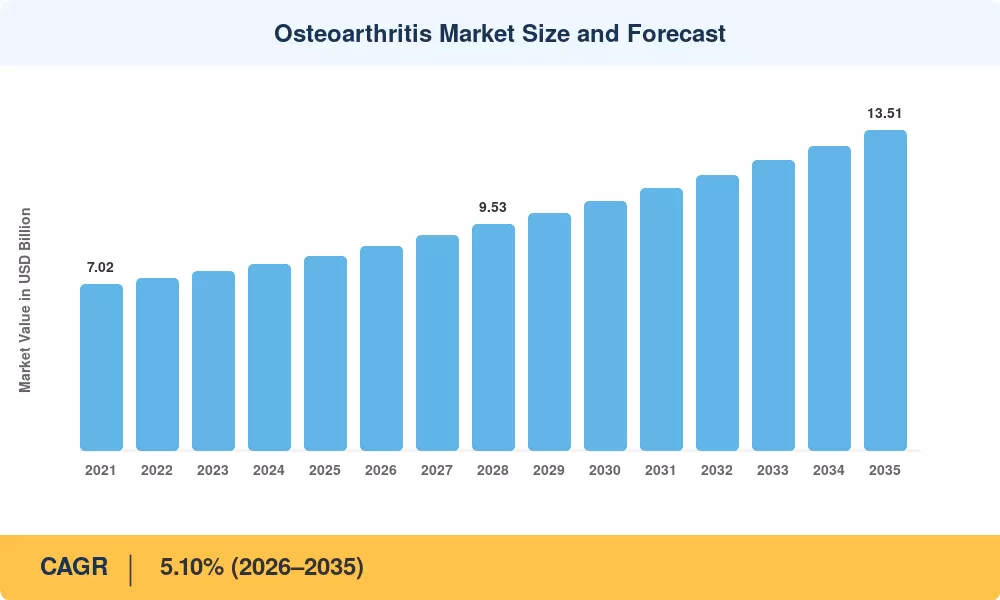

The Osteoarthritis Market size was valued at USD 8.21 Billion in 2025, and the market is projected to grow from USD 8.63 Billion in 2026 to USD 13.51 Billion by 2035, registering a CAGR of 5.10% during the forecast period 2026–2035. The rising prevalence of degenerative joint conditions among aging populations worldwide, combined with WHO projections indicating that over 500 million adults live with osteoarthritis globally, has elevated this therapeutic area to a healthcare spending priority [1]. National reimbursement reforms in the U.S. and EU are channeling hospital budgets toward minimally invasive interventions that delay costly total joint replacements, sustaining demand across pharmaceutical and device segments alike [2].

Treatment paradigms are shifting from symptom-only management toward disease-modification ambitions. Conventional oral anti-inflammatory regimens still anchor first-line care, yet clinicians are progressively adopting topical formulations and extended-release injectable therapies that improve safety profiles. Regulatory bodies, including the FDA and EMA, have fast-tracked several pipeline assets targeting nerve growth factor pathways and Wnt-signaling modulators, signaling a potential inflection point for the Osteoarthritis Market over the coming decade [3]. Biopharma investment in regenerative cartilage programs exceeded USD 2.8 billion cumulatively between 2022 and 2025 [4].

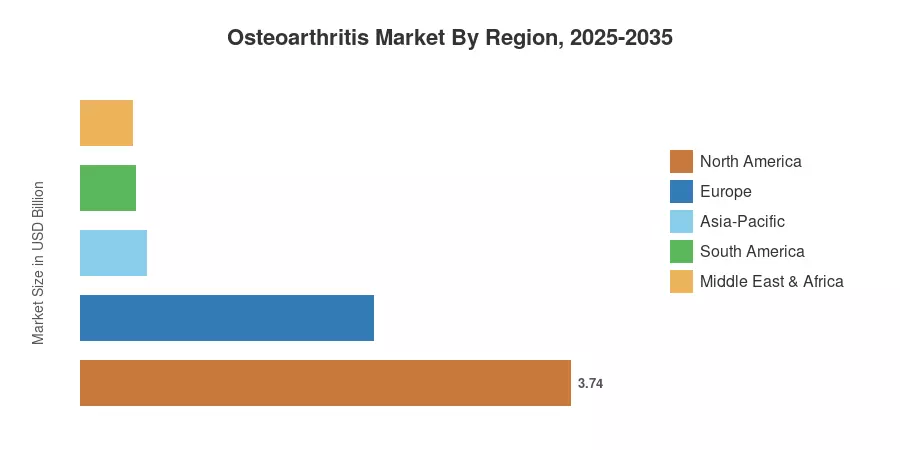

North America leads the Osteoarthritis Market with a 45.6% revenue share, driven by high per-capita pharmaceutical expenditure and broad private insurance coverage. Asia-Pacific is the fastest-growing region at a projected CAGR of 6.05%, propelled by rapidly expanding middle-class populations in China and India seeking specialist orthopedic care. Europe holds the second-largest share at 27.3%, supported by universal healthcare frameworks that encourage standardized treatment protocols. As demographic pressures intensify globally, the Osteoarthritis Market is poised for sustained, broad-based expansion through 2035.

Key Report Takeaways

• By Drug Class

- NSAIDs commanded a 44.3% share of the Osteoarthritis Market in 2025, remaining the dominant therapeutic category due to cost-effectiveness and wide formulary inclusion.

- Single-injection hyaluronic acid products are forecast to expand at a 7.05% CAGR through 2035, reflecting clinician preference for viscosupplementation that delays surgical intervention.

• By Anatomy

- Knee osteoarthritis accounted for 50.1% of the Osteoarthritis Market in 2025, correlating with the joint's high mechanical load-bearing burden.

- Shoulder cases are projected to advance at a 7.24% CAGR through 2035 as diagnostic imaging improvements increase detection rates.

• By Region

- North America retained a 45.6% revenue share of the Osteoarthritis Market in 2025, anchored by the United States' outsized pharmaceutical spending.

- The Asia-Pacific region is projected to grow at a 6.05% CAGR through 2035, led by rising healthcare access in China and India.

Osteoarthritis Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with orthopedic specialists, hospital procurement officers, and pharmaceutical executives, triangulated against national health expenditure databases, prescription audit data from IQVIA, and proprietary demand models calibrated to demographic projections from the United Nations Population Division [1][5].