Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Drug Class | NSAIDs, Analgesics, Corticosteroids, Hyaluronic Acid, Others | NSAIDs | Hyaluronic Acid |

| Anatomy | Knee, Hip, Shoulder, Ankle, Other Anatomies | Knee | Shoulder |

| Distribution Channel | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies | Hospital Pharmacies | Online Pharmacies |

| End User | Hospitals, Orthopedic Clinics, Others | Hospitals | Orthopedic Clinics |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

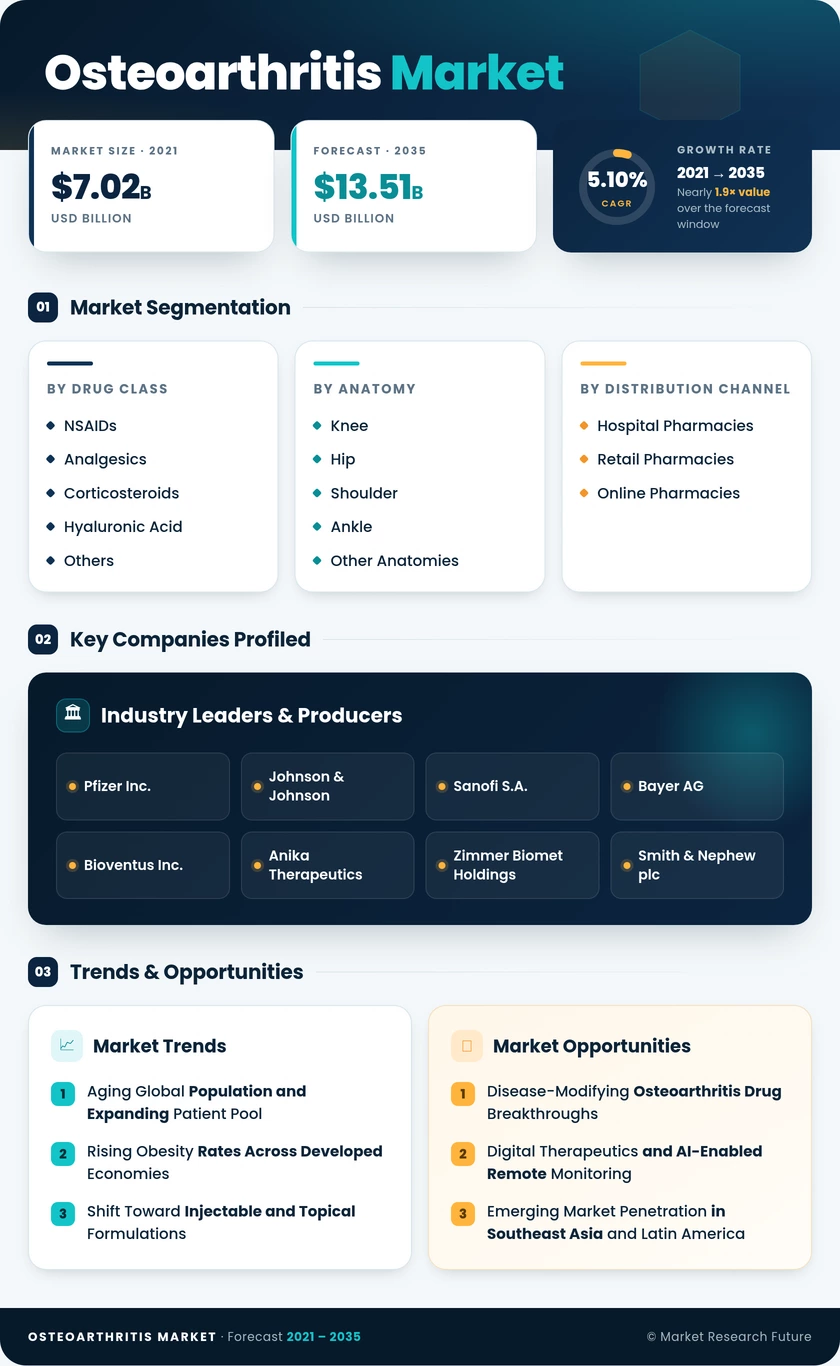

Market Segmentation Overview

By Drug Class

| Sub-Segment | Key Trend |

| NSAIDs | Shift from oral to topical formulations for improved safety profiles |

| Analgesics | Combination acetaminophen-tramadol protocols for moderate pain management |

| Corticosteroids | Extended-release intra-articular formulations reducing injection frequency |

| Hyaluronic Acid | Single-injection cross-linked products replacing multi-dose regimens |

| Others | Emerging biologics, nutraceuticals, and disease-modifying pipeline agents |

NSAIDs remain the largest drug class due to established efficacy and low cost, while hyaluronic acid injectables lead growth as clinical evidence increasingly supports their role in deferring surgical intervention.

By Anatomy

| Sub-Segment | Key Trend |

| Knee | Largest addressable population; highest injectable procedure volumes |

| Hip | Growing demand for pre-arthroplasty pharmaceutical management |

| Shoulder | Rising detection through advanced MRI and ultrasound imaging |

| Ankle | Post-traumatic osteoarthritis driving specialist referrals |

| Other Anatomies | Hand and spine osteoarthritis gaining clinical attention |

Knee disease dominates therapeutic spending across all regions, while shoulder osteoarthritis is emerging as a high-growth segment as improved imaging expands the diagnosed patient pool.

By Distribution Channel

| Sub-Segment | Key Trend |

| Hospital Pharmacies | Institutional procurement of injectable therapies for in-patient and outpatient administration |

| Retail Pharmacies | Outpatient dispensing of oral NSAIDs and topical analgesics |

| Online Pharmacies | Chronic medication refill automation and home delivery for elderly patients |

Hospital pharmacies lead by revenue share given the clinical administration requirements of injectable products, while online channels are growing fastest as digital pharmacy platforms improve access for chronic disease management.

By End User

| Sub-Segment | Key Trend |

| Hospitals | Comprehensive diagnostic, pharmaceutical, and surgical osteoarthritis management |

| Orthopedic Clinics | Ambulatory injection procedures shifting away from hospital settings |

| Others | Primary care physicians, rehabilitation centers, and physiotherapy clinics |

Hospitals capture the largest share of end-user spending, but orthopedic clinics represent the fastest-growing segment as ambulatory care models reduce procedural costs and improve patient access.