Photoelectric Sensor Market Summary

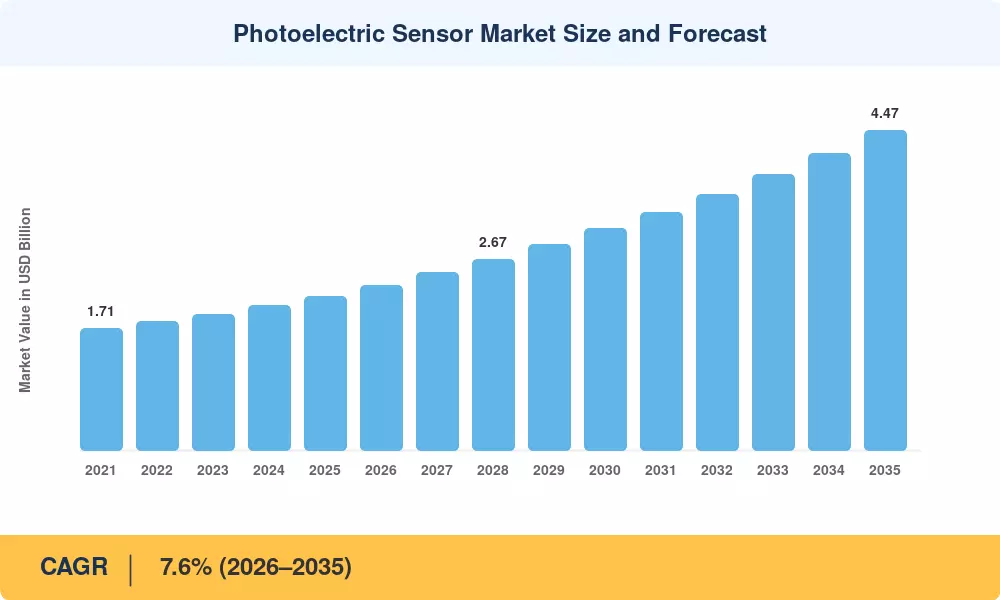

The Photoelectric Sensor Market reached USD 2.15 Billion in 2025 and is projected to grow from USD 2.31 Billion in 2026 to USD 4.47 Billion by 2035, registering a CAGR of 7.6% during the forecast period. This expansion tracks closely with global capital spending on smart-factory retrofits, where government tax incentives across major economies are accelerating adoption. The EU's €1.3 billion Digital Europe Programme and India's Production-Linked Incentive scheme for electronics both channel investment directly into automated inspection and packaging lines — exactly the environments where photoelectric sensors are indispensable [1][2].

A technology shift is well underway. Legacy inductive and mechanical limit switches are giving way to solid-state optical sensing platforms that integrate AI-enabled self-calibration, cutting routine maintenance labor by roughly 27%. Declining costs of high-power laser emitters — down an estimated 18% since 2022 — have widened the addressable market beyond premium automotive lines into mid-tier food processing and warehousing operations [3]. The adoption of IEC 61496-5 safety ratings has further raised the compliance bar, converting photoelectric sensors from optional upgrades into regulatory necessities for pharmaceutical and beverage producers.

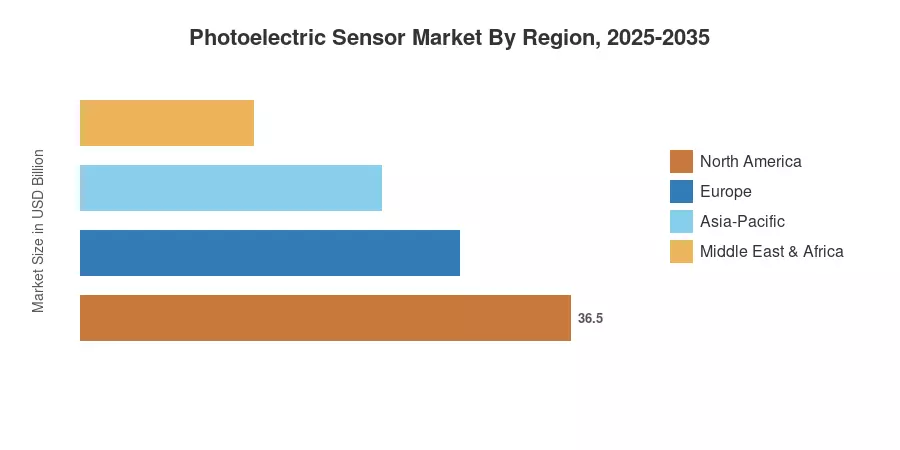

Asia-Pacific commands the dominant position in the Photoelectric Sensor Market with a 44.1% revenue share in 2025, powered by China's factory automation buildout and Japan's mature robotics ecosystem. The Middle East & Africa region is the fastest-growing region, forecast to expand at a 14.1% CAGR through 2035 as Saudi Arabia and the UAE invest heavily in Vision 2030 industrial diversification. Europe holds the second-largest share at 20.8%, anchored by Germany's Industrie 4.0 leadership. The decade ahead will be shaped by convergence between edge AI, miniaturized sensor packages, and predictive-maintenance platforms.

Key Report Takeaways

• By Product Type

- Laser sensors accounted for 36.0% of Photoelectric Sensor Market share in 2025, driven by their superior range and precision in high-speed assembly verification.

- Background-suppression sensors are forecast to grow at a 10.8% CAGR through 2035, supported by demand for reliable detection on reflective or irregularly shaped surfaces.

• By Detection Technology

- Through-beam configurations held 43.5% of the Photoelectric Sensor Market in 2025, preferred in conveyor-based logistics and packaging for their long sensing ranges.

- Retro-reflective sensors are gaining traction in compact machine enclosures where single-sided mounting reduces installation costs.

• By Housing Style

- Cylindrical housings (M8–M30) captured 47.3% of the Photoelectric Sensor Market revenue in 2025, reflecting widespread standardization across automotive and general manufacturing.

- PCB-mount devices are projected to register an 11.4% CAGR through 2035 as OEMs integrate sensors directly into compact electronic assemblies.

• By End-User Industry

- Automotive and e-mobility represented 23.7% of the Photoelectric Sensor Market in 2025, supported by rising EV production line complexity.

- Pharmaceuticals and medical devices will grow fastest at a 12.8% CAGR to 2035, propelled by stringent traceability mandates.

• By Region

- Asia-Pacific led the Photoelectric Sensor Market with a 44.1% revenue share in 2025.

- The Middle East & Africa region is projected to register a 14.1% CAGR through 2035, the highest among all regions.

Photoelectric Sensor Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up revenue estimates from sensor OEM filings, customs and trade databases, and primary interviews with automation integrators. Historical figures reflect actual shipment values; forecast-period estimates apply the calibrated CAGR while accounting for macroeconomic cycles and policy-driven investment surges.