Robotic Vision Market Summary

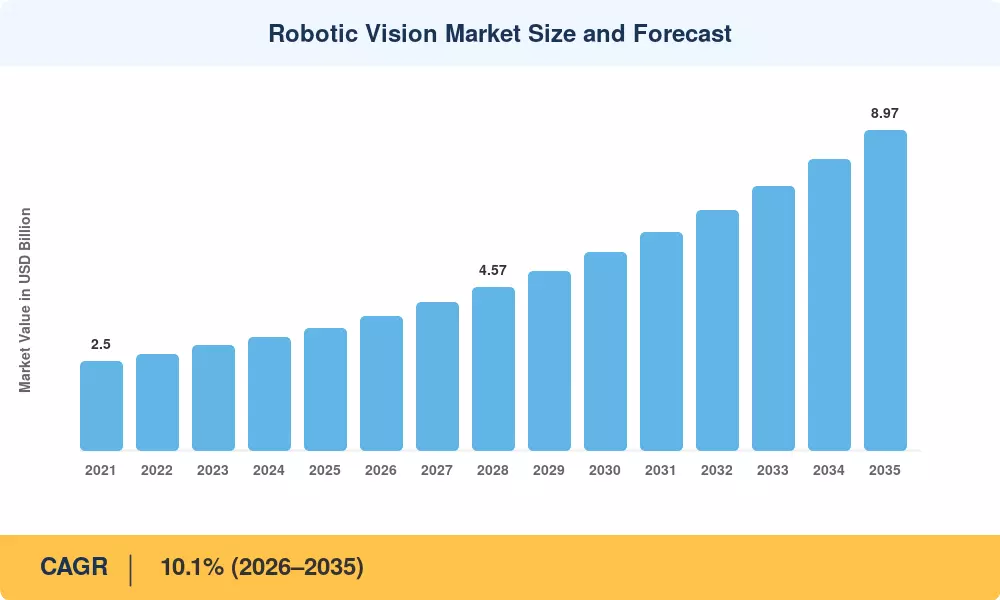

The global Robotic Vision Market was valued at USD 3.42 billion in 2025 and is projected to reach USD 8.97 billion by 2035, expanding at a CAGR of 10.1% during the forecast period 2026–2035. Government-led Industry 4.0 programs — including Germany's €5.3 billion Platform Industrie 4.0 and China's Made in China 2025 manufacturing upgrade mandate — are channeling capital into intelligent production lines that rely on vision-guided robots [1][2]. The convergence of cheaper compute silicon, mature deep learning frameworks, and tightening product-liability standards is pulling factory operators away from manual inspection toward automated visual intelligence.

The Robotic Vision Market is undergoing a key technical shift from traditional 2D pattern-matching systems to AI-enabled 3D volumetric sensing. Data suggests that global venture funding for vision-enabled robotics exceeded USD 4.8 billion in 2023-2025, with more than 40% of the money going to businesses developing edge-inference cameras and sensor-fusion platforms [3]. The European Union’s Machinery Regulation 2023/1230, coming into force from January 2027, will require autonomous risk-assessment logging for robotic workcells, effectively forcing vision system upgrades across the region [4].

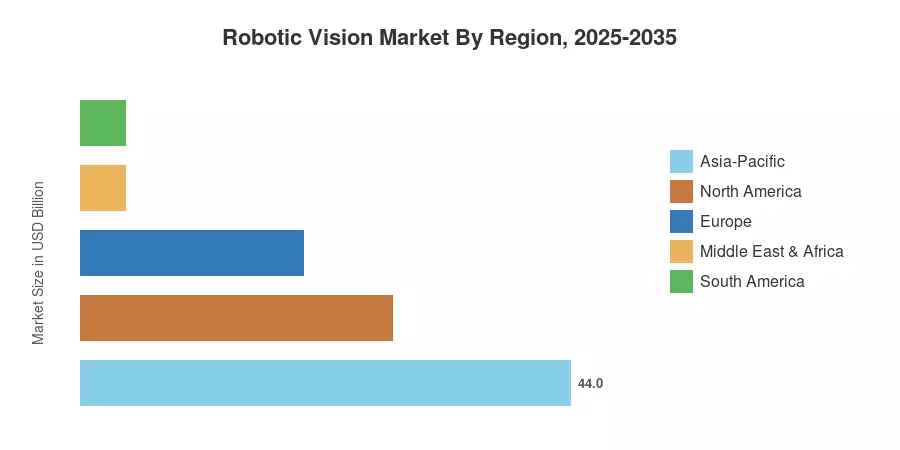

Asia Pacific dominates the Robotic Vision Market, capturing about 44% of global revenue due to China’s push for manufacturing automation and Japan’s subsidies for an aging workforce. North America is the second largest with about 28% share, supported by reshoring incentives under the U.S. CHIPS and Science Act. Europe follows at roughly 20%, with Germany and France dominating uptake. As collaborative-robot deployments speed across Southeast Asia and Latin America, the market's geographic base is anticipated to grow greatly through 2035.

Key Report Takeaways — Robotic Vision Market

By Technology

- 2D vision systems commanded a 52% share of the Robotic Vision Market in 2025, reflecting the installed base in automotive and electronics assembly lines.

- 3D vision systems are forecast to register an 11.2% CAGR through 2035, driven by adoption in aerospace and pharmaceutical quality control.

By Component & Robot Type

- Hardware generated approximately 62% of the Robotic Vision Market revenue in 2025, spanning cameras, optics, frame grabbers, and illumination units.

- Collaborative robots are projected to advance at an 11.3% CAGR during 2026–2035, as small and medium enterprises integrate compact vision-guided cobots.

By Application & End-User

- Material handling accounted for roughly 35% of the Robotic Vision Market in 2025, anchored by warehouse sortation and palletizing operations.

- Logistics and warehousing end users are anticipated to grow at a 12.0% CAGR to 2035, reflecting the e-commerce fulfillment surge.

By Geography

- Asia-Pacific led with a 44% share of the Robotic Vision Market in 2025 and is expected to post an 11.2% CAGR through 2035.

- North America held a roughly 28% share in 2025, underpinned by U.S. defense and semiconductor automation spending.

Robotic Vision Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s size model aggregates bottom-up revenue projections from more than 120 vision-system OEMs and integrators, validated against public financial disclosures, patent filing trends, and import/export databases across 42 countries. Historical statistics (2021–2024) derive from audited firm revenues, whereas future values (2026–2035) apply a segmented compound growth model calibrated to macroeconomic and technology-adoption variables.