Pneumatic Tube System Market Summary

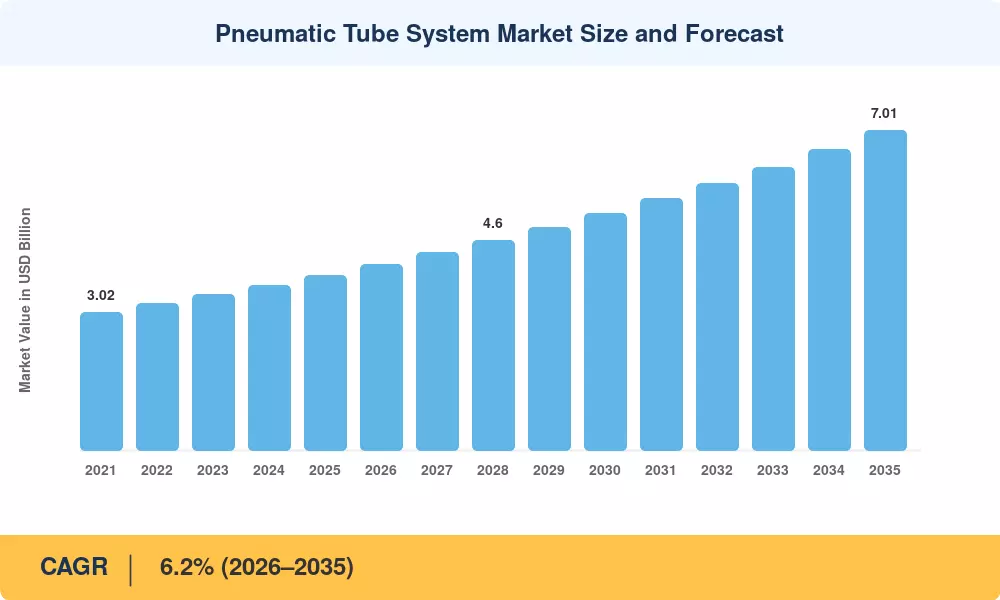

The Pneumatic Tube System Market reached an estimated USD 3.84 billion in 2025 and is projected to grow from USD 4.08 billion in 2026 to USD 7.01 billion by 2035, registering a CAGR of 6.2% during the forecast period. Two forces are propelling this expansion: a global surge in hospital infrastructure investment — the World Bank committed over USD 26 billion in health-sector lending between 2022 and 2024 alone — and escalating regulatory pressure on specimen turnaround times that makes manual courier systems untenable in modern clinical workflows.

Software-controlled, sensor-embedded tube networks are replacing outdated gravity-chute and manual-porter transport technologies. Pneumatic tube usage is currently indirectly encouraged by the U.S. Centers for Medicare & Medicaid Services (CMS), which links hospital compensation to quality measures that depend on quick laboratory turnaround [2]. Approximately EUR 4.5 billion has been set aside by smart hospital projects throughout the European Union for intralogistics upgrades until 2028 [3], with a portion of that money going directly toward the purchase of tube systems.

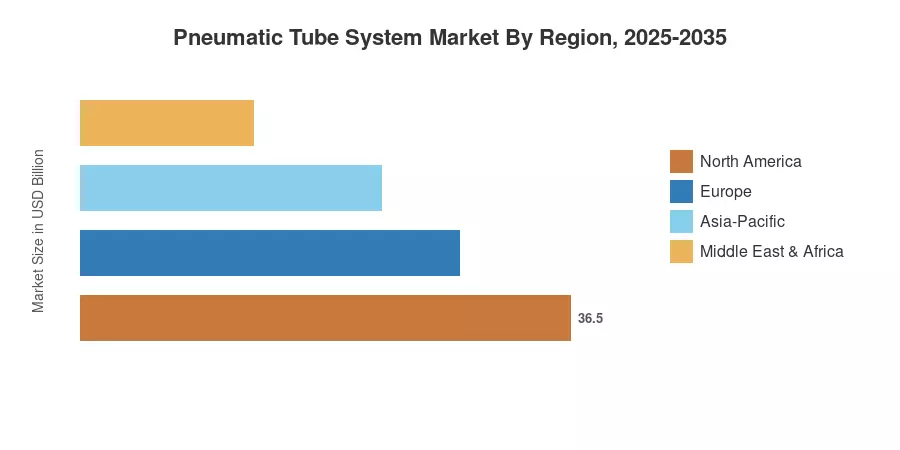

Due to a dense installed base and replacement-cycle investment, North America holds around 37% of the market for pneumatic tube systems. With a predicted 7.8% CAGR, Asia-Pacific is the fastest-growing area, driven by the development of new hospitals in Southeast Asia, China, and India. Europe has the second-largest proportion, at about 27%, thanks to Germany's mandate for hospital modernization. Over 90% of new system deployments will occur in these three locations over the course of the next ten years.

Key Report Takeaways

• By Technology

- Bidirectional systems hold the largest technology share (~48%) in the Pneumatic Tube System Market, reflecting the shift toward two-way carrier routing in multi-floor hospitals.

- Multistation networks are the fastest-growing technology segment at a projected CAGR of 7.4%, driven by campus-wide hospital complexes.

• By Application

- Healthcare facilities represent USD 1.73 billion in 2025 revenue, reinforcing the sector's dominance in the Pneumatic Tube System Market.

- Logistics and transportation applications are expanding at a 7.1% CAGR as airport operators integrate tube systems for secure document and small-parcel transfer.

• By Geography

- North America accounts for roughly 37% of global revenue, led by replacement-cycle demand in U.S. hospitals.

- Asia-Pacific is projected to grow at 7.8% CAGR through 2035, surpassing Europe in absolute market size by 2032.

- Germany alone generates an estimated 9% of the global Pneumatic Tube System Market revenue.

Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining bottom-up installation counts from hospital construction databases, top-down revenue estimates from manufacturer filings, and cross-validation against third-party benchmark sources. All historical figures are calibrated to audited financial disclosures where available.