Procurement Software Market Summary

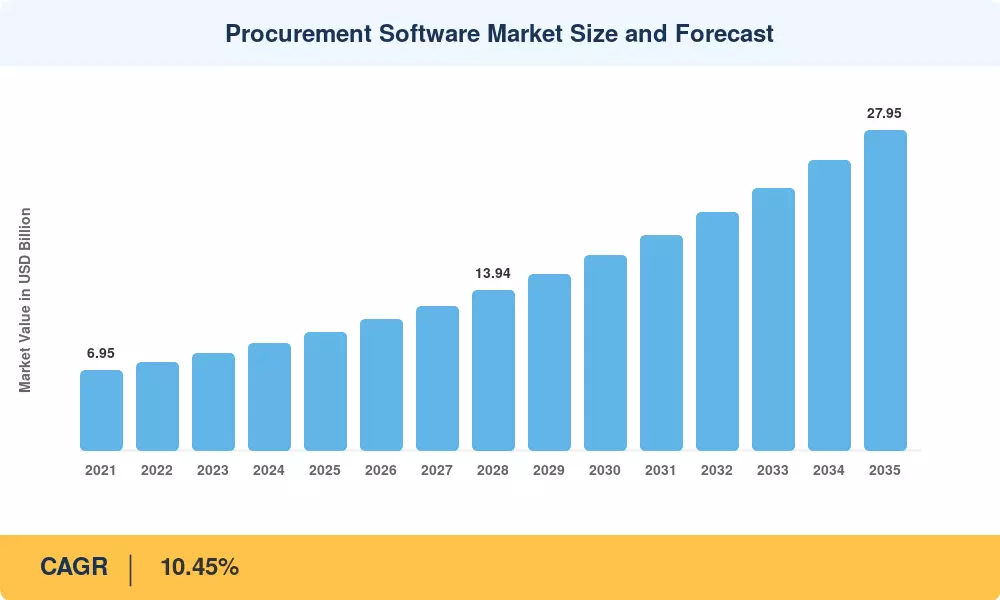

The Procurement Software Market reached an estimated USD 10.35 Billion in 2025 and is projected to grow from USD 11.43 Billion in 2026 to USD 27.95 Billion by 2035, registering a CAGR of 10.45% during the forecast period. Digital procurement mandates from governments worldwide — including the European Union's eProcurement Directive and the U.S. Federal Acquisition Regulation modernization initiative — are forcing organizations to replace manual requisition cycles with automated, audit-ready workflows [1]. Enterprise CFOs, under pressure to demonstrate real-time spend visibility, have tripled pilot budgets for e-procurement platforms since 2022 [2].

Legacy fax-and-spreadsheet procurement stacks are giving way to cloud-native suites that bundle purchase order automation, contract lifecycle management, and AI-driven sourcing management tools into unified dashboards. estimates that 65% of Fortune 500 procurement teams will run generative-AI copilots inside their spend management solutions by 2027, up from 12% in 2024 [3]. This shift is dismantling information silos that historically separated strategic sourcing from accounts payable.

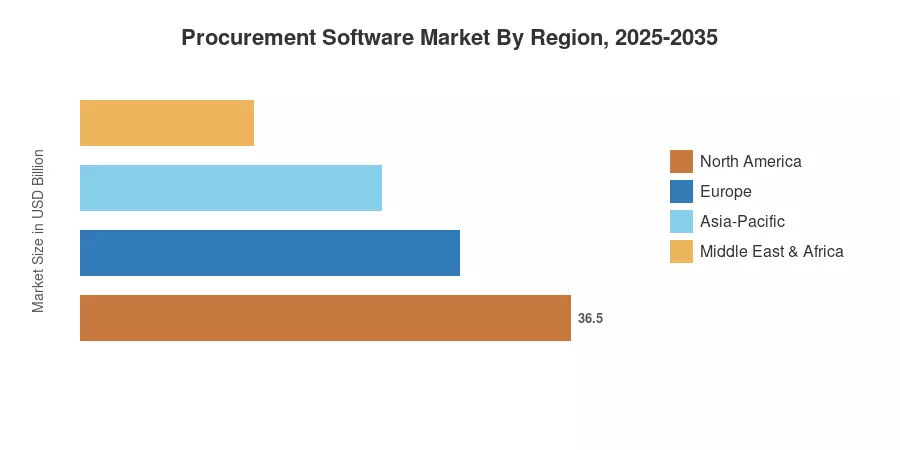

North America commands roughly 36% of global revenue, anchored by early SaaS adoption and a deep supplier management software ecosystem. Asia-Pacific leads on growth velocity with a CAGR surpassing 10.6%, propelled by India's GeM portal and China's state-backed digital supply-chain programs. Europe holds the second-largest share at approximately 27%, driven by ESG procurement regulations and cross-border e-invoicing mandates. As autonomous procurement cycles mature, the Procurement Software Market is set to redefine how enterprises convert spend data into competitive advantage.

Key Report Takeaways

• By Deployment & Component

- Cloud deployment captured approximately 72% of the Procurement Software Market in 2025, driven by elastic SaaS architectures and zero-infrastructure onboarding.

- Services (implementation, consulting, managed services) are expanding at a 10.6% CAGR through 2035, outpacing software licenses as vendors shift toward recurring-revenue models.

• By End-User Industry & Organization Size

- Manufacturing accounted for a 23% revenue share in the Procurement Software Market, reflecting complex multi-tier supplier networks that demand real-time sourcing management tools.

- SMEs are the fastest-growing organization segment at a projected 10.5% CAGR, fueled by freemium e-procurement platforms and embedded financing.

• By Region

- North America generated USD 3.73 Billion in 2025, supported by deep integration of purchase order automation into ERP ecosystems.

- Asia-Pacific's 10.65% CAGR reflects public e-procurement mandates and leapfrog cloud adoption across emerging economies.

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up vendor revenue aggregation with top-down macroeconomic demand modeling, cross-referenced against 120+ procurement technology vendor filings and validated through primary interviews with 80 CPOs across six regions.