Property and Casualty Insurance Market Summary

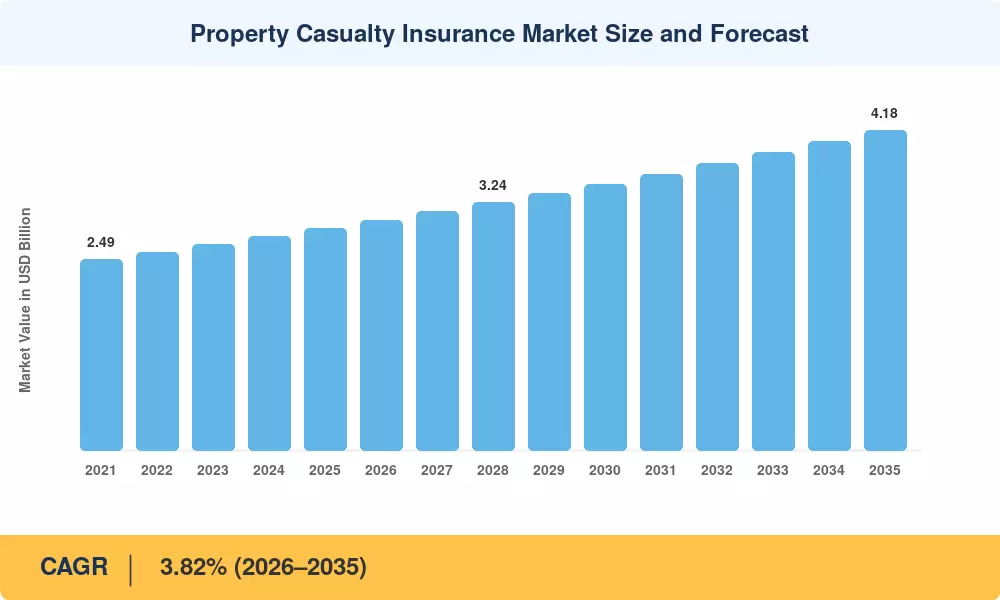

The property casualty insurance market reached USD 2.90 billion in 2025, with the forecast period opening at USD 3.01 billion in 2026 and climbing to USD 4.18 billion by 2035 at a 3.82% CAGR. Premium repricing driven by climate volatility and regulatory mandates around transparent IFRS-17 reporting has injected fresh capital into underwriting operations globally. Governments across the US, EU, and emerging Asian economies have tightened solvency requirements, compelling insurers to adopt catastrophe modeling for property insurance and strengthen reserve adequacy—catalysts that continue to push steady premium volume growth across the property casualty insurance market.

AI-powered P&C claims automation technologies are replacing legacy paper-based claims processing and manual commercial property liability underwriting workflows. Global InsurTech investment hit USD 7.4 billion in 2024, driving digital distribution for personal lines P&C and parametric coverage packages. A significant number of new policy originations today are being driven by usage-based telematics and embedded insurance APIs, changing how carriers price risk and gain clients in the property casualty insurance market.

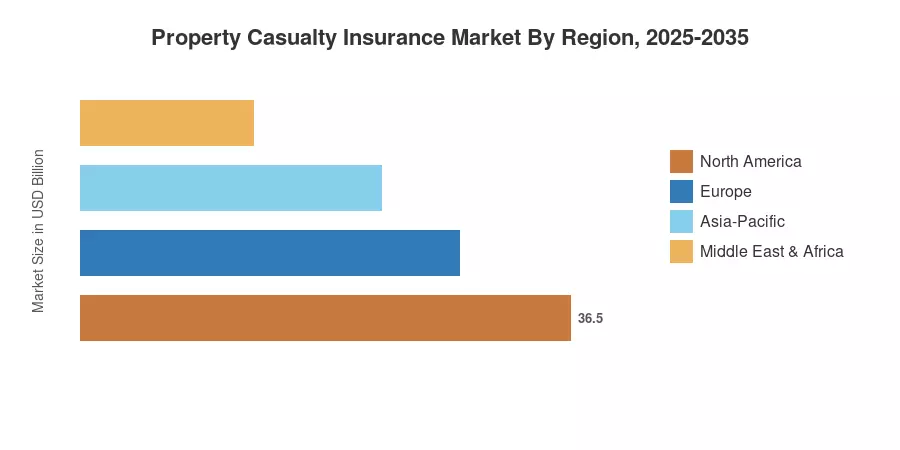

The US contributes about 41% of worldwide sales in North America, with residential and commercial liability categories. Asia-Pacific is the fastest-growing market with a predicted CAGR of 4.95% through 2035, driven by increased middle-class asset ownership and required motor coverage mandates in India and China. Europe is the second-largest market at about 27%, with demand supported by revisions to Solvency II and green-building insurance regulations. The property casualty insurance market is ripe for fundamental change as digital-first carriers compete with legacy incumbents across all geographies.

Key Report Takeaways

• By Product Type

- Motor insurance held approximately 46% of the property casualty insurance market share in 2025, driven by compulsory third-party liability mandates and rising vehicle values.

- Liability insurance is forecast to expand at an 8.65% CAGR through 2035, fueled by commercial property liability underwriting complexity and litigation cost inflation.

- Homeowner insurance contributed USD 0.58 billion in 2025 as climate-driven claims pushed carriers toward catastrophe modeling for property insurance.

• By Distribution Channel

- Brokers accounted for a 48% share of the property casualty insurance market in 2025, reflecting entrenched corporate relationships.

- Digital aggregators and InsurTech solutions for property and casualty channels are forecast to grow at a 4.82% CAGR, the fastest among all distribution modes.

• By Geography

- North America dominated the property casualty insurance market with 41% revenue share, underpinned by robust commercial lines demand.

- Asia-Pacific is projected to reach the highest CAGR of 4.95% through 2035.

The data below are a mix of bottom-up premium volume analysis and top-down macroeconomic calibration. Historical figures (2021-2024) are sourced from annual statutory files, reinsurance reports and national regulatory disclosures. Forecast estimates (2026–2035) are calculated using the calibrated 3.82% CAGR with changes for expected catastrophe loss trend and the digital distribution for personal lines P&C adoption curves across the property casualty insurance industry.

.webp?v=1782888030)