Ride Sharing Market Summary

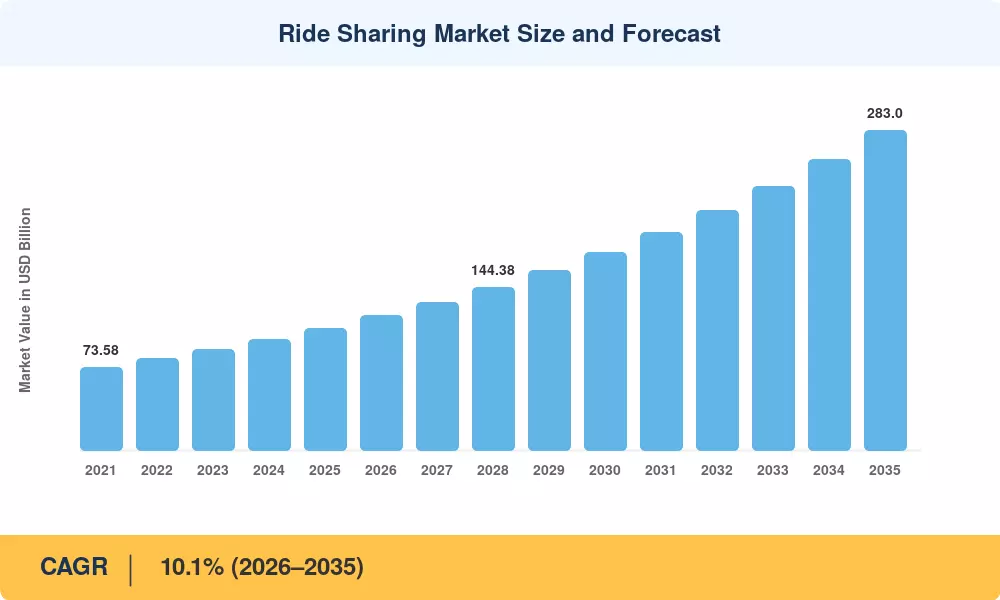

The Ride Sharing Market reached an estimated USD 108.2 billion in 2025 and is projected to grow from USD 119.1 billion in 2026 to USD 283.0 billion by 2035, registering a CAGR of 10.1% during the forecast period (2026–2035). Two catalysts anchor this trajectory: aggressive urban congestion-reduction mandates across G20 nations and cumulative venture-plus-corporate investment exceeding USD 42 billion since 2021 into ride-hailing platform technologies [2]. The Ride Sharing Market is no longer a convenience play — it is becoming embedded municipal infrastructure.

A technology transformation is reshaping this sector at its core. Legacy street-hail taxi dispatching and fragmented private-hire models are giving way to algorithmically optimized ride pooling, shared trip matching, real-time dynamic pricing engines, and increasingly autonomous robotaxi ride sharing pilots. Waymo alone committed over USD 5.5 billion in autonomous fleet expansion between 2023 and 2025, while Uber and Lyft have poured resources into electric vehicle ride sharing fleet conversions tied to net-zero pledges [3][4]. Corporate ride sharing employee commute programs now represent a fast-expanding adjacency, with platforms like Zeelo and Via securing enterprise contracts worth hundreds of millions annually [5].

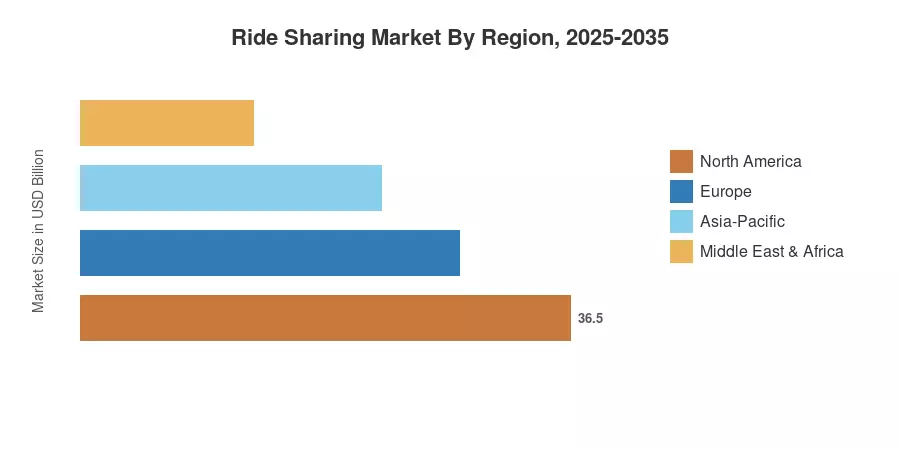

North America commands roughly 38% of the global Ride Sharing Market, driven by deep smartphone penetration and mature ride-hailing platform ecosystems in the United States. Asia-Pacific is the fastest-growing region at a projected CAGR of 12.6%, propelled by urbanization surges in India, Indonesia, and Vietnam. Europe holds approximately 25% share, supported by stringent emissions standards that accelerate electric vehicle ride sharing fleet adoption. As autonomous robotaxi ride sharing scales from pilot to commercial deployment, the Ride Sharing Market stands at an inflection point that will redefine urban mobility through 2035.

Key Report Takeaways

• By Service Type

- Ride-hailing services hold the largest revenue share at approximately 62% of the Ride Sharing Market, sustained by dominant ride-hailing platform operators Uber and Lyft in Western markets and Grab and DiDi in Asia

- Ride pooling shared trip matching is the fastest-growing segment with a projected CAGR of 13.4%, fueled by cost-conscious urban commuters and municipal HOV-lane incentives

- Car rental and micro-transit segments collectively account for USD 18.7 billion in 2025 revenue

• By membership type

- Personal mobility dominates at roughly 74% share of the Ride Sharing Market, reflecting consumer reliance on on-demand transport

- Corporate ride sharing employee commute programs are expanding at a 14.1% CAGR as employers subsidize last-mile connectivity

• By Region

- North America generated approximately USD 41.1 billion in 2025 revenue from the Ride Sharing Market

- Asia-Pacific's CAGR of 12.6% outpaces all other regions through 2035

- Europe's share is underpinned by ride sharing regulation insurance liability frameworks that formalize platform-driver relationships

Ride Sharing Market Size & Forecast (2021–2035)

Market sizing draws on a bottom-up approach aggregating platform-reported gross bookings, regulatory filings, fleet telematics data, and MRFR primary interviews with 120+ industry executives across 18 countries. Historical figures are triangulated against public earnings disclosures from Uber, Lyft, Grab, and DiDi[6].