Set-Top Box (STB) Market Summary

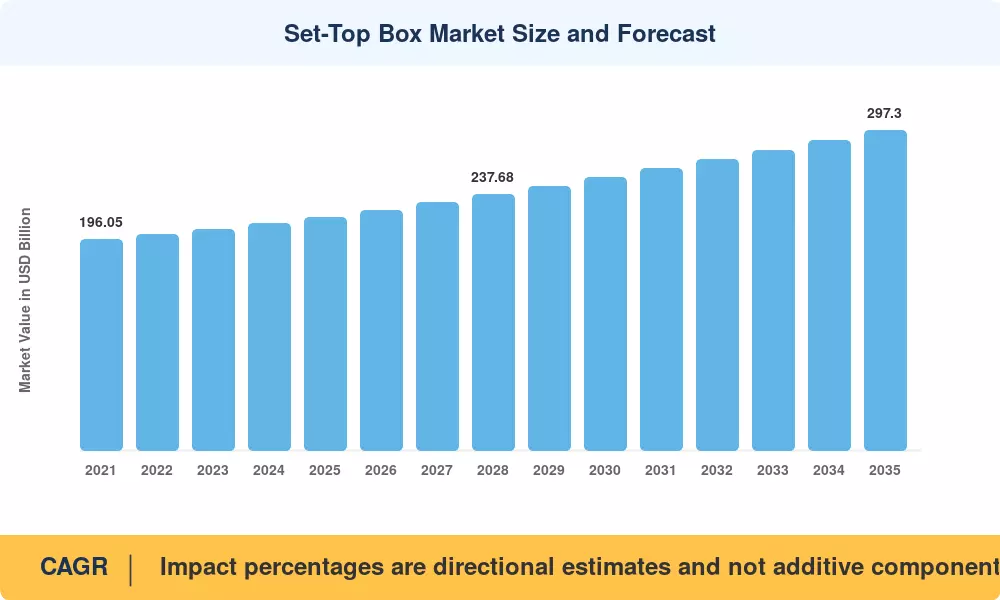

The Set-Top Box Market was valued at USD 216.40 billion in 2025 and is projected to reach USD 222.95 billion in 2026 before climbing to USD 297.30 billion by 2035, registering a CAGR of 3.25% across the 2026–2035 forecast window. Fibre-to-the-home rollouts across Europe and the Asia-Pacific, combined with aggressive 4K content acquisition by cable operators ahead of major global sporting events, are anchoring demand for next-generation receiver hardware. Government broadband subsidies — including programs that have directed over USD 42 billion toward last-mile connectivity in the United States alone — continue to expand the addressable installed base for IP-connected devices [1].

A structural technology shift is reshaping the Set-Top Box Market. Legacy proprietary middleware stacks are giving way to operator-grade open platforms such as Reference Design Kit and standardized Linux distributions, compressing product development cycles from 18 months to under 8 months. Operators that migrated to open platforms have reported 20–30% reductions in software maintenance costs, freeing capital for user-experience enhancements and cloud-DVR integration [2]. The result is a device category that increasingly resembles a managed smart TV appliance rather than a simple descrambler.

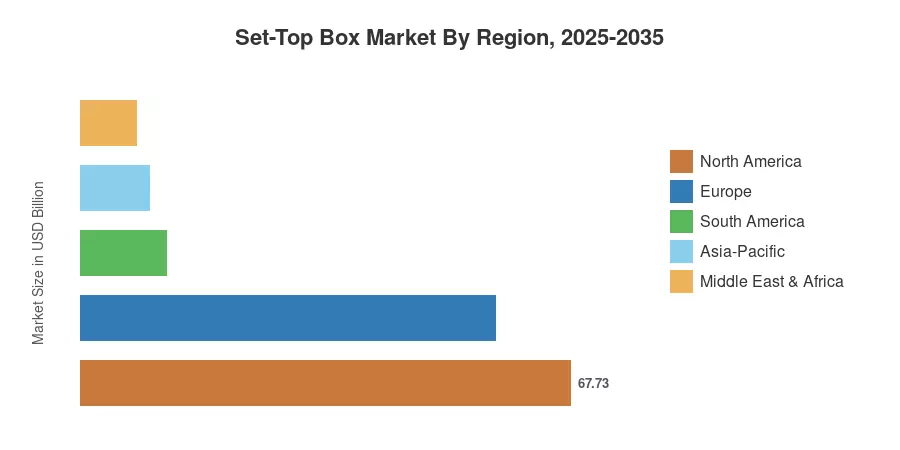

North America held approximately 31.3% of the Set-Top Box Market in 2025, supported by high average revenue per user among cable multisystem operators. Asia-Pacific is the fastest-growing region, forecast to expand at a 4.40% CAGR through 2035, driven by broadband densification in India and Southeast Asia. Europe contributed roughly 26.5% of global revenue, with IPTV uptake in France, Germany, and the Nordic nations offsetting satellite declines. The next decade will increasingly reward vendors capable of bridging linear broadcast and over-the-top streaming within a single hybrid architecture.

Key Report Takeaways

• By Technology

- Satellite and direct-to-home platforms accounted for approximately 48.0% of the Set-Top Box Market in 2025, reflecting their entrenched position in regions with limited fixed broadband.

- Internet protocol television is forecast to grow at a 4.10% CAGR from 2026 to 2035, fueled by telco triple-play bundling and fibre network expansion.

• By End User

- Residential subscribers represented roughly 71.5% of the Set-Top Box Market in 2025, driven by multi-room viewing and whole-home networking requirements.

- The transportation segment is projected to record the fastest end-user CAGR at approximately 4.15% through 2035.

• By Region

- North America dominated with a 31.3% share of the Set-Top Box Market in 2025, underpinned by premium 4K unit pricing and bundled broadband strategies.

- Asia-Pacific is set to expand at a 4.40% CAGR during 2026–2035, led by India's BharatNet broadband initiative and rising IPTV adoption across ASEAN economies.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from vendor shipment data, operator procurement disclosures, and regional trade statistics. Forecast projections layer in broadband penetration trajectories, content-licensing investment trends, and regulatory impact modeling across 35 countries.