Single Use Bioprocessing Market Summary

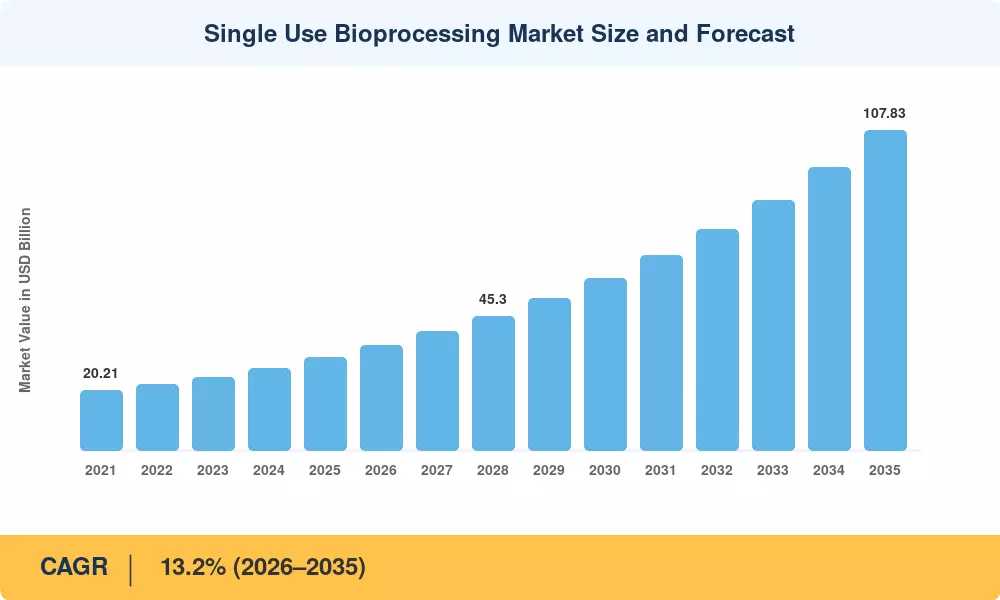

The Single Use Bioprocessing Market reached USD 31.23 Billion in 2025, reflecting a pronounced shift from traditional stainless-steel infrastructure toward pre-sterilized, polymer-based production systems across the global biomanufacturing landscape. The market is projected to expand from USD 35.35 Billion in 2026 to USD 107.83 Billion by 2035, registering a CAGR of 13.2% over the forecast period. This trajectory is anchored in two catalysts: the FDA's 2025 guidance update that streamlined validation pathways for closed single-use assemblies, and an estimated USD 18 Billion in new biologics facility investments announced across the United States and the European Union between 2023 and 2025 [1][2].

The technology transformation reshaping the Single Use Bioprocessing Market centers on replacing fixed, multi-use stainless-steel vessels — which require costly clean-in-place and steam-in-place cycles — with integrated disposable systems spanning bioreactors, mixers, filtration trains, and sensor arrays. AI-driven process analytical technology (PAT) platforms now connect directly to disposable inline sensors, enabling real-time control without permanent hardware. The European Medicines Agency's revised Annex 1 guidelines, enforced from August 2024, further accelerated adoption by mandating contamination-control strategies where single-use closed systems offered the clearest compliance path [3][4].

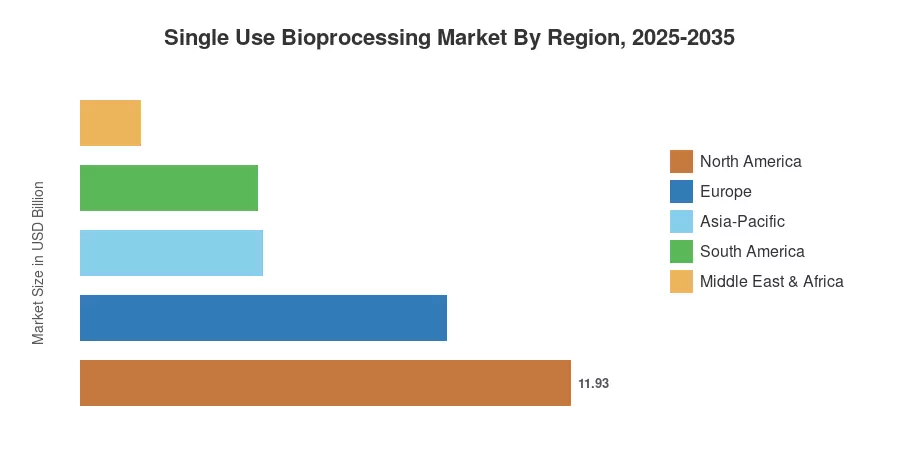

North America commanded approximately 38.2% of the Single Use Bioprocessing Market in 2025, buoyed by concentrated biologics manufacturing in the U.S. mid-Atlantic corridor and strong regulatory clarity from the FDA. Asia-Pacific stands as the fastest-growing region at a projected CAGR of 14.2%, driven by biosimilar production scale-ups in India, South Korea, and China. Europe held the second-largest share at roughly 28.5%, supported by the EU's Pharmaceutical Strategy investments. As cell and gene therapy pipelines mature and CDMOs scale commercial operations, the Single Use Bioprocessing Market is positioned for sustained double-digit expansion through 2035[5].

Key Report Takeaways

• By Product

- Single-use bioreactors captured approximately 42% of the Single Use Bioprocessing Market in 2025, driven by the transition from stainless-steel fermenters across mid-scale commercial campaigns.

- Sensors and analytics modules represent the fastest-growing product category, advancing at a 17.5% CAGR through 2035 as real-time PAT adoption intensifies.

- Filtration assemblies accounted for an estimated USD 5.8 Billion in 2025 revenue, reflecting downstream purification demand.

• By End User

- Biopharmaceutical companies held roughly 69.5% of the Single Use Bioprocessing Market revenue in 2025, encompassing monoclonal antibody and vaccine production.

- Contract development and manufacturing organizations (CDMOs) are expanding at a 16.0% CAGR to 2035, reflecting outsourcing momentum among mid-size biotechs.

• By Region

- North America led the Single Use Bioprocessing Market with 38.2% revenue share in 2025, supported by dense U.S. biomanufacturing clusters.

- Asia-Pacific is forecast to grow at a 14.2% CAGR through 2035, the highest among all regions.

- Europe contributed 28.5% of 2025 revenue, anchored by Germany, France, and the U.K.

Single Use Bioprocessing Market Size and Forecast (2021–2035)

Market Research Future derives market sizing through a triangulated methodology that combines top-down industry revenue analysis, bottom-up product shipment tracking across 40+ countries, and validated interviews with 180+ procurement and operations executives at biopharmaceutical companies, CDMOs, and suppliers. Historical figures (2021–2024) are reconciled against publicly reported revenues of leading suppliers, while the forecast (2026–2035) applies scenario-weighted modeling tied to biologics pipeline progression and facility investment announcements.