Smart Factory Market Summary

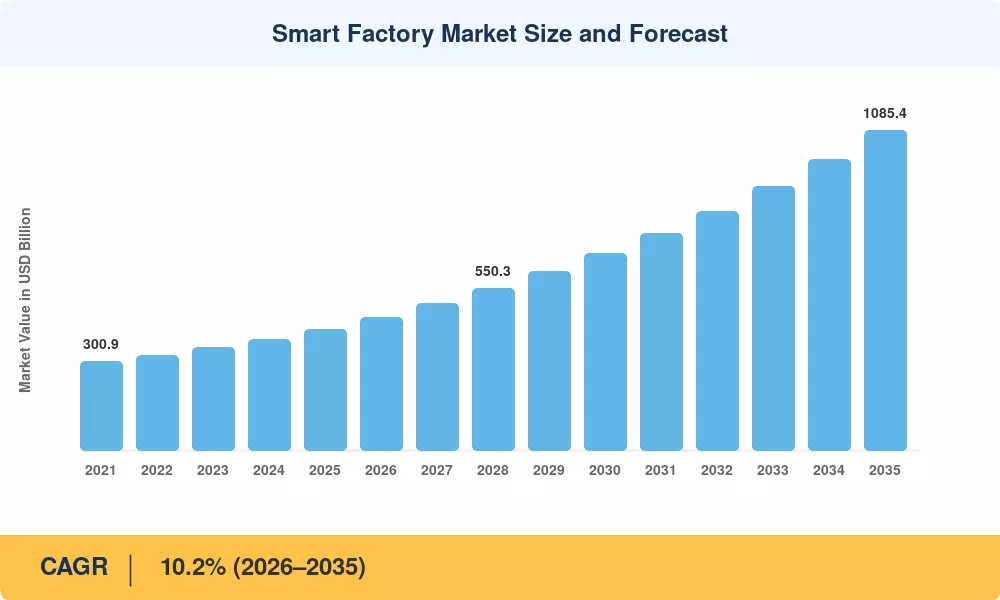

The Smart Factory Market was valued at USD 410.90 billion in 2025, is projected to reach USD 452.80 billion in 2026, and is expected to climb to USD 1,085.40 billion by 2035, registering a CAGR of 10.2% over the 2026–2035 forecast period. Two forces are compressing adoption timelines: government capital incentives across Asia-Pacific manufacturing corridors and carbon-border adjustment mechanisms in Europe that penalize energy-opaque production lines [1]. Together, these policy levers are converting what was once a discretionary technology upgrade into a compliance imperative for export-facing factories.

The technology landscape inside the Smart Factory Market is shifting from siloed programmable logic controllers and standalone SCADA systems toward unified data architectures where sensors, execution platforms, and analytics layers communicate in real time. A 2024 World Economic Forum survey estimated that leading manufacturers investing more than USD 15 billion collectively in factory digitization between 2022 and 2024 shortened unplanned downtime by 30–45% [2]. Edge inference chips now process quality-control decisions at the line level, reducing round-trip latency that cloud-only architectures impose.

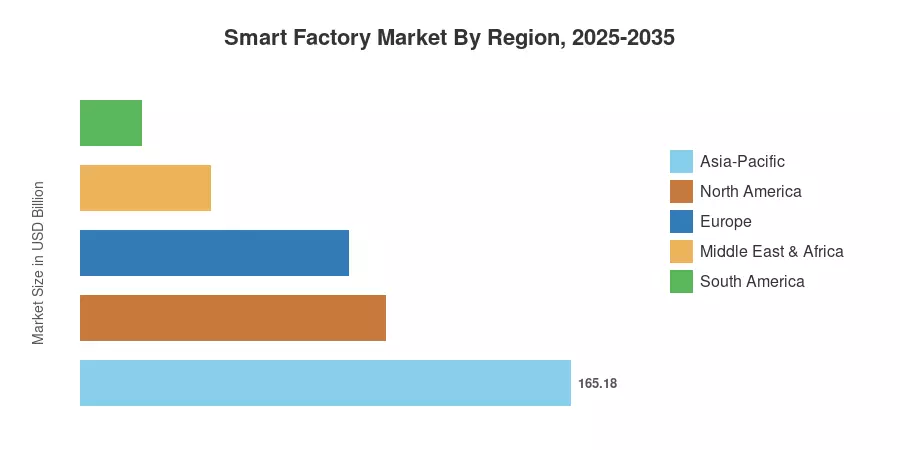

Asia-Pacific dominates the Smart Factory Market with roughly 40.2% of 2025 revenue, driven by China's "Intelligent Manufacturing 2025" program and India's Production-Linked Incentive schemes [3]. The Middle East & Africa region is the fastest-growing geography, advancing at a 10.7% CAGR through 2035 as Saudi Arabia's Vision 2030 industrial diversification funds flow into greenfield factory builds. North America holds the second-largest share at approximately 25.0%, anchored by the reshoring incentives in the U.S. CHIPS and Science Act. The decade ahead will reward manufacturers that treat factory intelligence as a platform rather than a project.

Key Report Takeaways

• By Product Type

- Industrial robotics accounted for 30.4% of Smart Factory Market revenue in 2025, reflecting strong demand for welding, painting, and material-handling automation across automotive and electronics assembly.

- Collaborative robots are expanding at a 9.5% CAGR through 2035, fueled by small-and-medium-enterprise adoption in mixed human–robot workflows.

• By Technology

- Manufacturing execution systems captured 22.2% of technology spending in the Smart Factory Market in 2025, anchoring shop-floor orchestration.

- Advanced analytics and AI platforms are growing at an 11.1% CAGR as real-time process optimization moves from pilot to production scale.

• By End-User Industry

- Automotive represented 29.2% of end-user demand in 2025, driven by electric-vehicle line retooling and just-in-sequence assembly requirements.

- Pharmaceuticals represent the fastest-growing vertical at a 10.6% CAGR, propelled by serialization mandates and continuous-manufacturing adoption.

• By Region

- Asia-Pacific led global demand with 40.2% share in the Smart Factory Market in 2025.

- The Middle East & Africa is projected to expand at a 10.7% CAGR through 2035.

Smart Factory Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates bottom-up revenue estimates from equipment OEMs, software license disclosures, and system integrator project databases. Historical figures (2021–2024) reflect actual shipment data and annual reports, while the forecast horizon (2026–2035) applies a calibrated compound growth rate informed by policy pipelines, capital-expenditure surveys, and technology adoption curves.