Smart Warehousing Market Summary

The Smart Warehousing Market stood at USD 2.48 billion in 2025, with the forecast period opening at USD 3.28 billion in 2026 and climbing to USD 32.43 billion by 2035 at a CAGR of 29.0%. Two forces anchored this trajectory: the U.S. Infrastructure Investment and Jobs Act earmarked over USD 65 billion for broadband and digital logistics corridors. At the same time, the EU's Digital Decade Policy Programme committed member states to 75% cloud adoption across critical supply-chain sectors by 2030 [2][3]. These catalysts funneled capital directly into AI-powered warehouse operations and intelligent inventory management platforms.

Legacy pick-and-pack workflows once dominated by paper-based processes are giving way to automated warehouse technology stacks that merge cloud-native warehouse management software with sensor-rich IoT warehouse management networks. Venture funding in warehouse robotics surpassed USD 5.3 billion globally between 2022 and 2024, reflecting investors' conviction that robotic smart storage systems and autonomous mobile robots will become standard infrastructure rather than niche upgrades [4]. The convergence of edge computing and digital twins is accelerating deployment timelines from years to months.

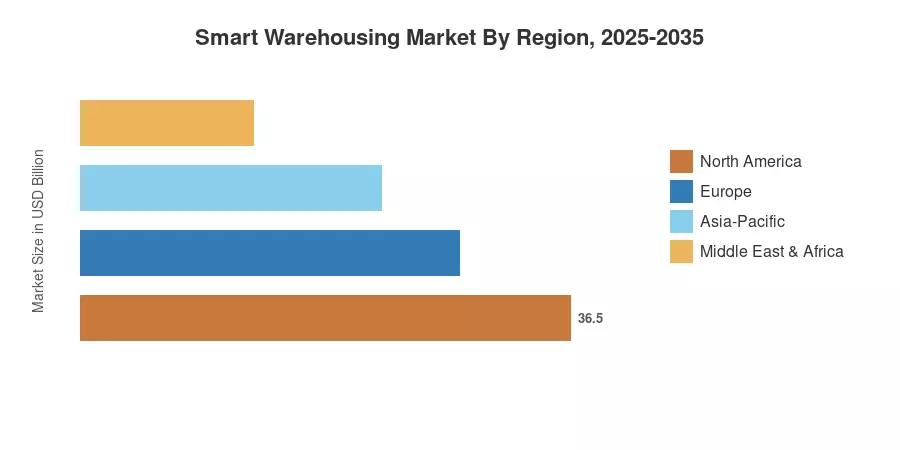

North America commanded 36.1% of the Smart Warehousing Market in 2025, propelled by early automation mandates from major retailers and third-party logistics providers. Asia-Pacific is the fastest-growing region, projected at a 17.9% CAGR through 2035, fueled by manufacturing modernization across China and India. Europe held the second-largest share at roughly 24.2%, with Germany's Industry 4.0 agenda serving as the continent's primary growth engine. The decade ahead will reward operators who integrate AI-powered warehouse operations across the full inbound-to-outbound cycle.

Key Report Takeaways

• By Component

- Software captured 43.5% of the Smart Warehousing Market revenue share in 2025, driven by the proliferation of cloud-native WMS and intelligent inventory management solutions.

- Services are projected to register a CAGR of 19.3% through 2035 as system integration, training, and managed-service contracts expand.

• By Technology

- Automated storage and retrieval systems (AS/RS) accounted for 30.5% of the Smart Warehousing Market size in 2025.

- Autonomous mobile robots and drones are forecast to grow at a 21.3% CAGR, reflecting demand for flexible, scalable robotic smart storage systems.

• By End-User

- Retail and e-commerce held a 35.2% share of the Smart Warehousing Market in 2025, underscoring fulfilment-speed pressures.

- Healthcare and pharmaceuticals will advance at a 22.2% CAGR, propelled by cold-chain traceability and compliance mandates.

• By Region

- North America led with 36.1% revenue share; Asia-Pacific posted the highest regional CAGR of 17.9% through 2035.

Smart Warehousing Market Size and Forecast (2021–2035)

MRFR's estimates synthesize primary interviews with warehouse operators, technology vendors, and logistics executives alongside secondary data from trade associations, regulatory filings, and third-party financial disclosures. All figures are expressed in current USD Billion.