Superfoods Market Summary

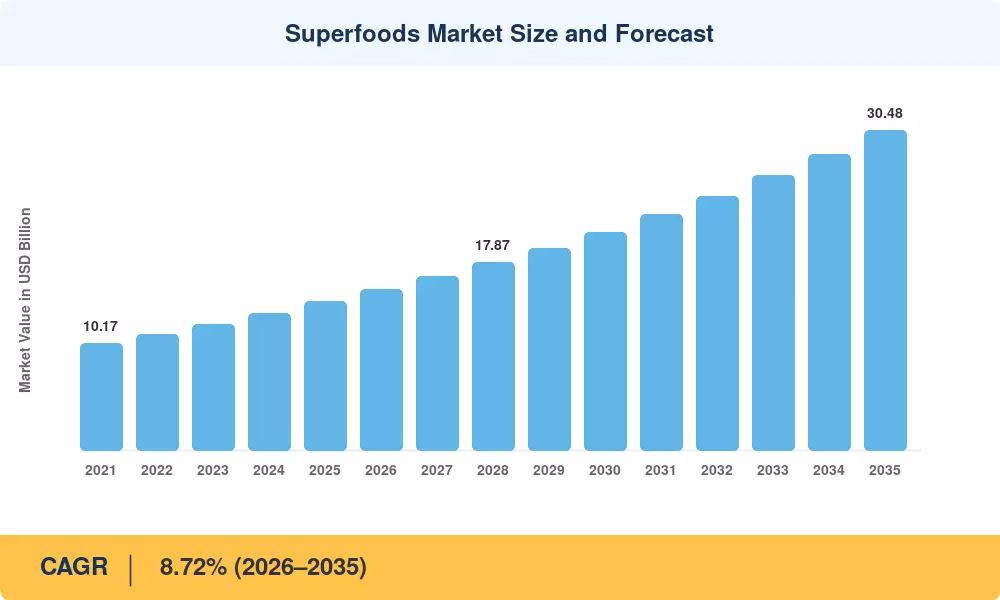

The global Superfoods Market was valued at USD 14.21 billion in 2025 and is projected to reach USD 15.36 billion in 2026, climbing to USD 30.48 billion by 2035 at a CAGR of 8.72% during the forecast period (2026–2035). This expansion is anchored in a decisive shift toward preventive healthcare spending—global wellness expenditure surpassed USD 5.6 trillion in 2024—and updated regulatory frameworks such as the FDA's revised "healthy" nutrient content claim, which now permits nutrient-dense foods like avocados, nuts, and salmon to carry front-of-pack health labels [2]. The Superfoods Market benefits directly from these policy catalysts as consumers increasingly seek antioxidant-rich foods and functional food ingredients that align with clinical nutrition guidance.

Whole food nutrition items being delivered to consumers are changing. Legacy bulk-commodity supply networks are being replaced by digitally integrated, cold-chain-optimized distribution methods that preserve bioactive components in superfood powders and supplements. In 2024, private-label investment in nutrient-dense health foods around the globe surpassed USD 2.1 billion, with shops like Costco and Aldi expanding their product offerings for organic acai, spirulina, and moringa [3]. With this change in the infrastructure, smaller brands can compete on quality, not just shelf space.

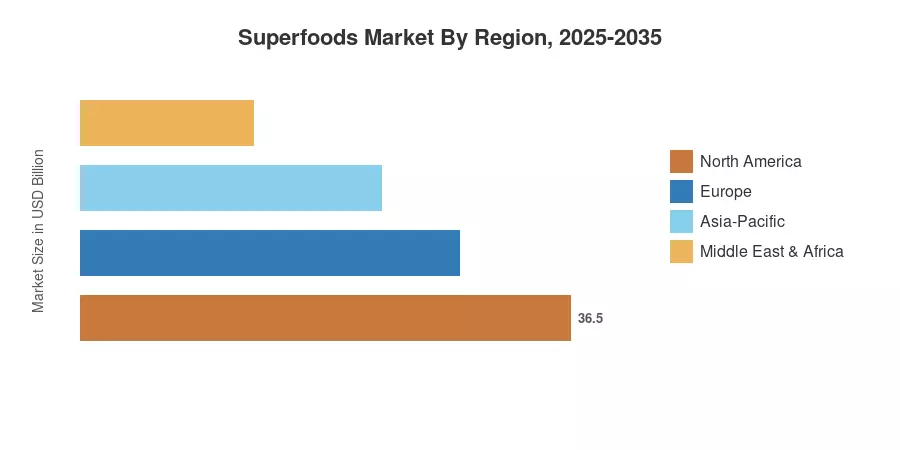

North America accounts for around 40.3% of the Superfoods Market, because to high retail penetration and clinical research funding Asia-Pacific is the fastest-growing market with a projected CAGR of 10.87% through 2035, due to rising disposable incomes in China and India, and emerging e-commerce channels for whole food nutrition products [4]. Europe retains the second greatest proportion of about 27.5%, with the Farm to Fork strategy of the EU strengthening the demand for organic and antioxidant foods [5]. “Over the next 10 years, personalized nutrition platforms and AI-powered formulation will increasingly define the Superfoods Market.

Key Report Takeaways

• By Product Type

- Fruit-based superfoods led the Superfoods Market with a 36.1% revenue share in 2025, reflecting strong demand for acai, blueberry, and goji berry products across retail and foodservice channels

- Algae-based superfoods are forecast to expand at an 11.08% CAGR through 2035, positioning spirulina and chlorella as high-growth functional food ingredients

• By Form

- Powders captured approximately USD 6.32 billion in 2025 revenue, driven by convenience-oriented consumers blending superfood powders and supplements into daily routines

- Liquid formats are the fastest-rising form at a 10.34% CAGR, propelled by ready-to-drink smoothie and cold-pressed juice innovation

• By Region

- North America retained the dominant position in the Superfoods Market with 40.3% of 2025 global revenue

- Asia-Pacific is on course for a 10.87% CAGR to 2035, with China and India as primary growth engines for nutrient-dense health foods

Market Size and Forecast (2021–2035)

MRFR's proprietary sizing framework triangulates top-down revenue estimates from trade databases, company filings, and customs data with bottom-up demand models validated through 120+ expert interviews conducted in Q4 2024 and Q1 2025.

.webp?v=1783416547)