Unified Threat Management Market Summary

The Unified Threat Management Market reached a valuation of USD 9.96 Billion in 2025 and is projected to grow from USD 11.19 Billion in 2026 to USD 32.03 Billion by 2035, advancing at a CAGR of 12.40% during the forecast period (2026–2035). Two forces are propelling this trajectory: the proliferation of ransomware-as-a-service syndicates that tripled attack volumes on mid-market firms between 2022 and 2024, and the regulatory tightening exemplified by the EU's NIS2 Directive, which mandates consolidated security reporting for essential-services operators [1]. Government cybersecurity spending across G7 nations surpassed USD 38 Billion in 2024, channeling significant procurement toward converged security platforms [2].

Enterprises are steadily retiring siloed point products — standalone firewalls, disconnected intrusion-detection modules, and bolt-on VPN appliances — in favor of software-defined, cloud-delivered platforms that unify inspection engines under a single management pane. 's 2024 planning guidance estimated that 68% of mid-market security budgets now prioritize platform consolidation over best-of-breed stacking [3]. This shift rewards vendors that can deliver continuous threat-intelligence updates without firmware replacement cycles.

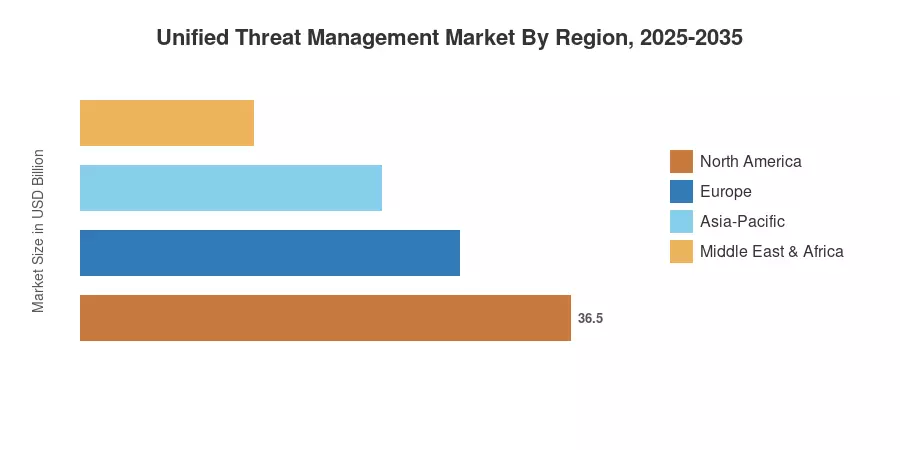

North America commands roughly 39.2% of the Unified Threat Management Market revenue base, anchored by federal zero-trust mandates and a dense MSSP ecosystem. Asia-Pacific is the fastest-growing geography, registering a 16.8% CAGR through 2035 as data-sovereignty laws in India, Indonesia, and Vietnam force localized security stacks [4]. Europe holds the second-largest share at approximately 26.5%, driven by NIS2 compliance timelines that extend through 2027. As hybrid-work architectures harden into permanent operating models, the Unified Threat Management Market is set to benefit from a decade-long consolidation wave.

Key Report Takeaways

• By Component

- Software captured 70.5% of the Unified Threat Management Market share in 2025, reflecting the migration toward subscription-licensed, auto-updating security engines.

- Services are projected to grow at a 13.6% CAGR through 2035 as managed-detection-and-response bundles gain traction among lean IT teams.

• By Deployment

- Cloud deployment held a 14.89% CAGR trajectory, outpacing on-premise adoption as throughput constraints diminish with purpose-built cloud gateways.

• By Organization Size

- Large enterprises retained 65.1% revenue share in 2025 within the Unified Threat Management Market, yet small and medium enterprises are advancing at a 13.42% CAGR through 2035.

• By Region

- North America accounted for 39.2% of global revenue in 2025, supported by CISA's Binding Operational Directives and widespread MSSP adoption.

- Asia-Pacific is forecast to expand at a 16.8% CAGR to 2035, powered by manufacturing digitalization and maritime cybersecurity regulations.

- Europe contributed approximately 26.5% of global revenue, with NIS2 compliance serving as the principal procurement catalyst.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from vendor revenue disclosures, channel-partner surveys, and customs trade data. Forecast projections apply a calibrated compound growth model benchmarked against proprietary demand indicators and third-party intelligence.